Lake Success, New York-based Broadridge Financial Solutions, Inc. (BR) is a financial technology company that provides investor communications and technology-driven solutions to banks, broker-dealers, asset managers, and corporate issuers. It is valued at a market cap of $20.7 billion.

Companies worth $10 billion or more are typically classified as “large-cap stocks,” and BR fits the label perfectly, with its market cap exceeding this threshold, underscoring its size, influence, and dominance within the information technology services industry. The company is aggressively expanding its footprint in digital assets and artificial intelligence, exemplified by its Distributed Ledger Repo (DLR) platform reaching record volumes and its recent strategic acquisition of Acolin to enhance cross-border fund distribution capabilities in Europe.

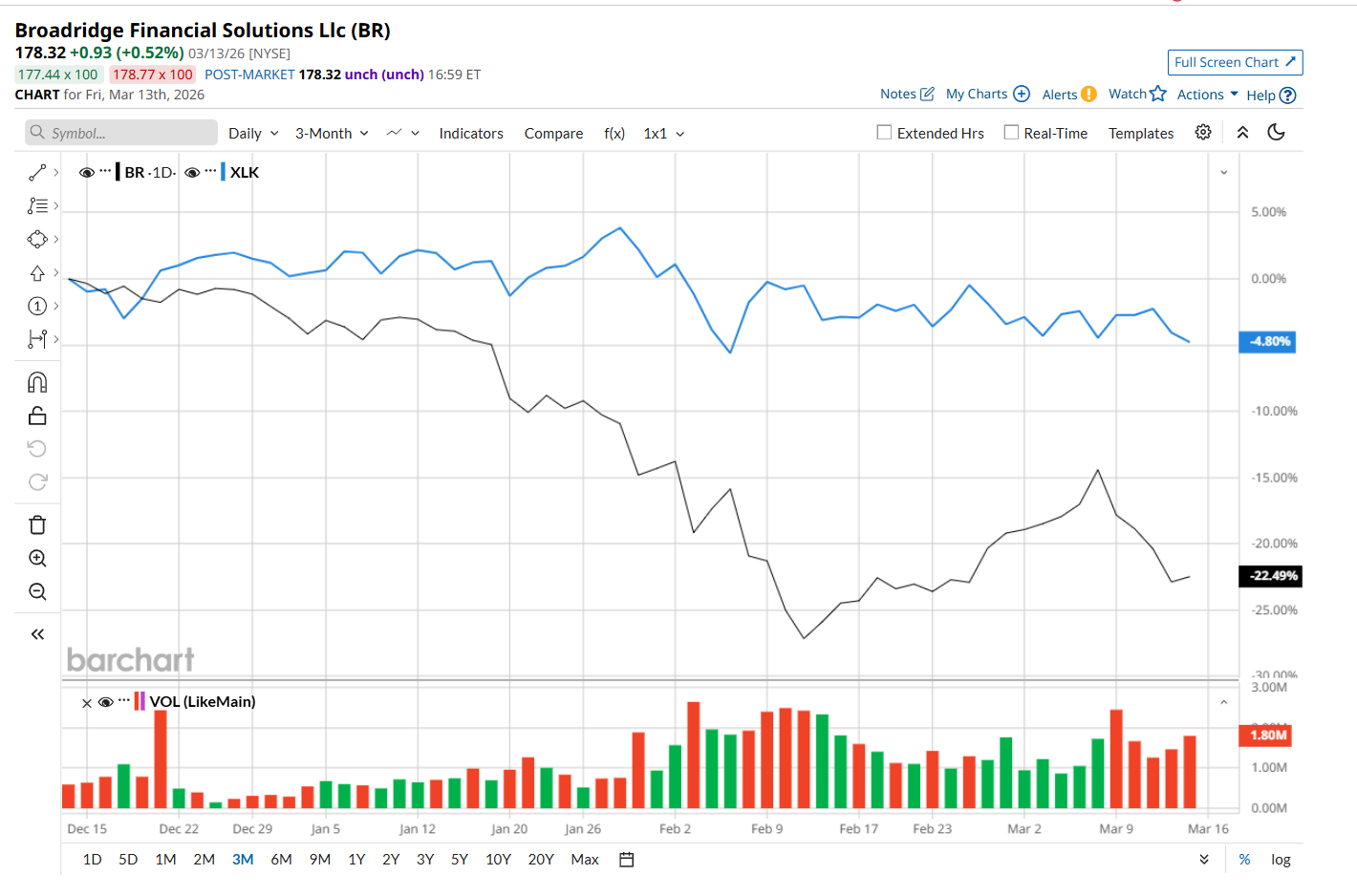

This fintech company has slipped 34.4% from its 52-week high of $271.91, reached on Aug. 7, 2025. Shares of BR have declined 22.5% over the past three months, underperforming the State Street Technology Select Sector SPDR ETF’s (XLK) 4.8% decline during the same period.

Moreover, on a YTD basis, shares of BR are down 20.1%, compared to XLK’s 5% fall. In the longer term, BR has fallen 21% over the past 52 weeks, notably lagging behind XLK’s 31.8% uptick over the same time frame.

To confirm its bearish trend, BR has been trading below its 200-day moving average since late September and has remained below its 50-day moving average since mid-September, with slight fluctuations.

On Feb. 3, BR released better-than-expected Q2 earnings results, yet its shares plunged 6.3%. The company’s total revenue increased 7.9% year over year to $1.7 billion, surpassing consensus estimates by 7.5%, while its adjusted EPS advanced 1.9%, handily topping analyst expectations of $1.34. Strong organic growth of 7%, including strength in investor participation and elevated levels of event-driven activity, supported its performance.

BR has outperformed its rival, Fidelity National Information Services, Inc. (FIS), which fell 28.8% over the past 52 weeks and 25.2% on a YTD basis.

Despite BR’s recent underperformance, analysts remain moderately optimistic about its prospects. The stock has a consensus rating of "Moderate Buy” from the nine analysts covering it, and the mean price target of $239.57 suggests a 34.3% premium to its current price levels.

On the date of publication, Neharika Jain did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Walmart v.s Costco: Which Is the Better Dividend Stock in 2026?

- Is Carvana Stock a Buy on New Stock Split Announcement?

- Palantir Is Now a Sports Betting Stock. Does That Make PLTR a Buy Here?

- Tesla’s China-Made EV Sales Just Nearly Doubled. Should You Buy TSLA Stock Now in Hopes of an Auto Business Rebound?