CION Investment Corp (CION), a BDC that pays out 90% of its interest income from loans it owns, pays a 10-cent monthly distribution. At $6.55 per share, CION stock now has an 18.3% annualized yield. It looks very attractive to value investors as its income covers the distributions.

CION closed down 4% on Friday, March 13, at $6.55, following the company's earnings release on March 12. That provides value investors with a great investing opportunity. This article will show why.

Huge Yield - And It's Covered!

First, let's look at the distribution. Management announced on March 9 that it will keep paying 10 cents a month for the next 3 months, or 30 cents for Q2.

So, if this keeps up, the cumulative distribution for the next 12 months will be $1.20, and the forward distribution yield is over 18%:

$1.20 / $6.55 = 0.1832 = 18.32%

So, why did the stock fall? Maybe investors were disappointed. After all, it had previously paid out 36 cents per quarter (in one payment) last year. Or maybe they think CION could cut the distribution payment again.

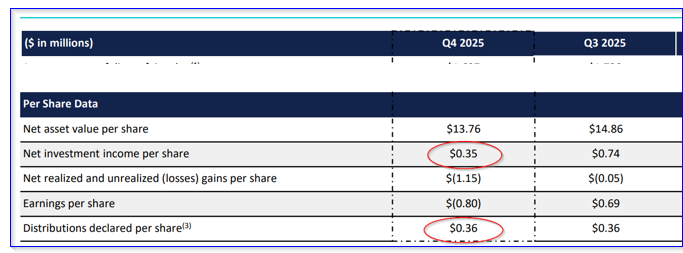

Investors need not worry if CION can afford this payment. The investment deck shows that CION's earnings per share (EPS) were negative 80 cents per share.

That included a net unrealized and realized loss of $1.15 (mostly from unrealized loan asset writedowns). Its actual investment income, which is the basis to pay out distributions, was 35 cents - more than enough to cover the 30-cent distribution going forward.

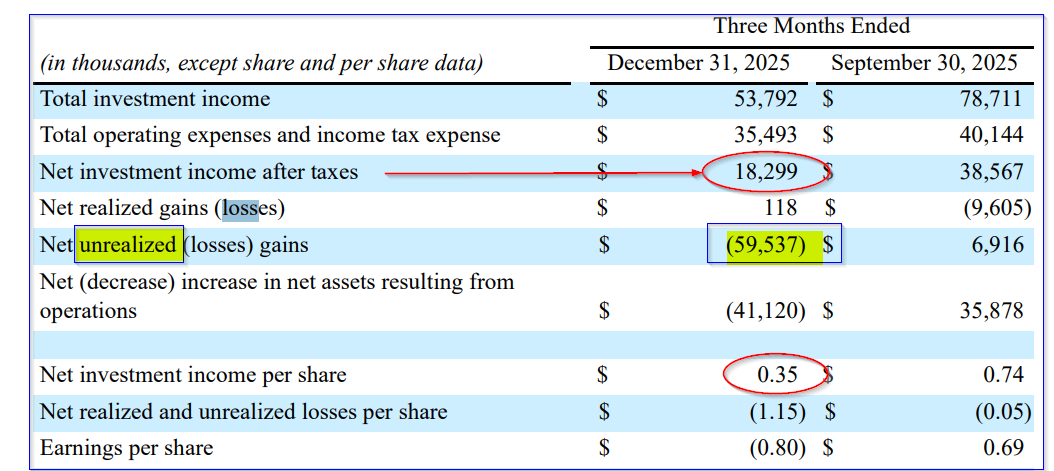

Here is another way to look at this. Cion's Q4 investment income was $53.8 million. After expenses and taxes, it generated $18.3 million in income, or 35 cents per share on a cash flow basis, as the unrealized loss was $59.5 million:

But, today its shares outstanding have fallen to 50.496 million. That means that investment income, if it continues at this level, is now 36.2 cents:

$18.3m / 50.496m shs o/s = 0.362 = 36.2 cents

As a result, the 30-cent distribution is well-covered - even more than is evident from the Q4 results.

$0.10 x 50.496 shs o/s = $5.596m/mo x 3 = $15.1488 million

In other words, there will be $3.15 million in extra cash flow (i.e., $18.3m - $15.15m = $3.15), or 6.24 cents (i.e., 3.15m/50.5m shs).

The company will have an extra 6 cents going forward if investment income stays at the same level.

Huge Discount to NAV

Moreover, note that CION's net asset value (NAV), although down from Q3, is still $13.76 per share. That means at $6.55, CION stock is trading for less than half its book value:

$6.55/$13.76 = 0.476 = 47.6% of NAV

This is what value investors typically look for - a margin of safety. For example, let's say that in Q1 or Q2, the company has to write off more loans - up to 25% of its assets.

$13.76 NAV - .25($13.76) = $13.76 - $3.44 = $10.32 NAV

So, even if CION writes off more than 3x the $1.10 NAV Q4 reduction (i.e., $14.86-$13.76) from Q3, the NAV will still be well over the stock price today:

$6.55/$10.32 = 0.635 = 63.5%

In other words, any potential bad news is more than adequately reflected in today's price, making it a bargain.

Summary and Conclusion

Cion distributions are from a business development company, so they are not qualified dividends. But, no matter, at 18.3%, the annualized forward yield is very attractive.

For example, the average yield in 2025 was 14.89% according to Morningstar. If CION were to trade at that yield today, the stock should be +23% higher:

$1.20 / 0.1489 = $8.06

$8.06 / $6.55 = 1.23 (i.e., 23% upside)

This article has shown that based on (1) its cash flow coverage, (2) discount to NAV, and (3) average yield, CION stock looks to be way too cheap.

The bottom line is that CION stock is statistically undervalued and attractive to value investors.

On the date of publication, Mark R. Hake, CFA did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart