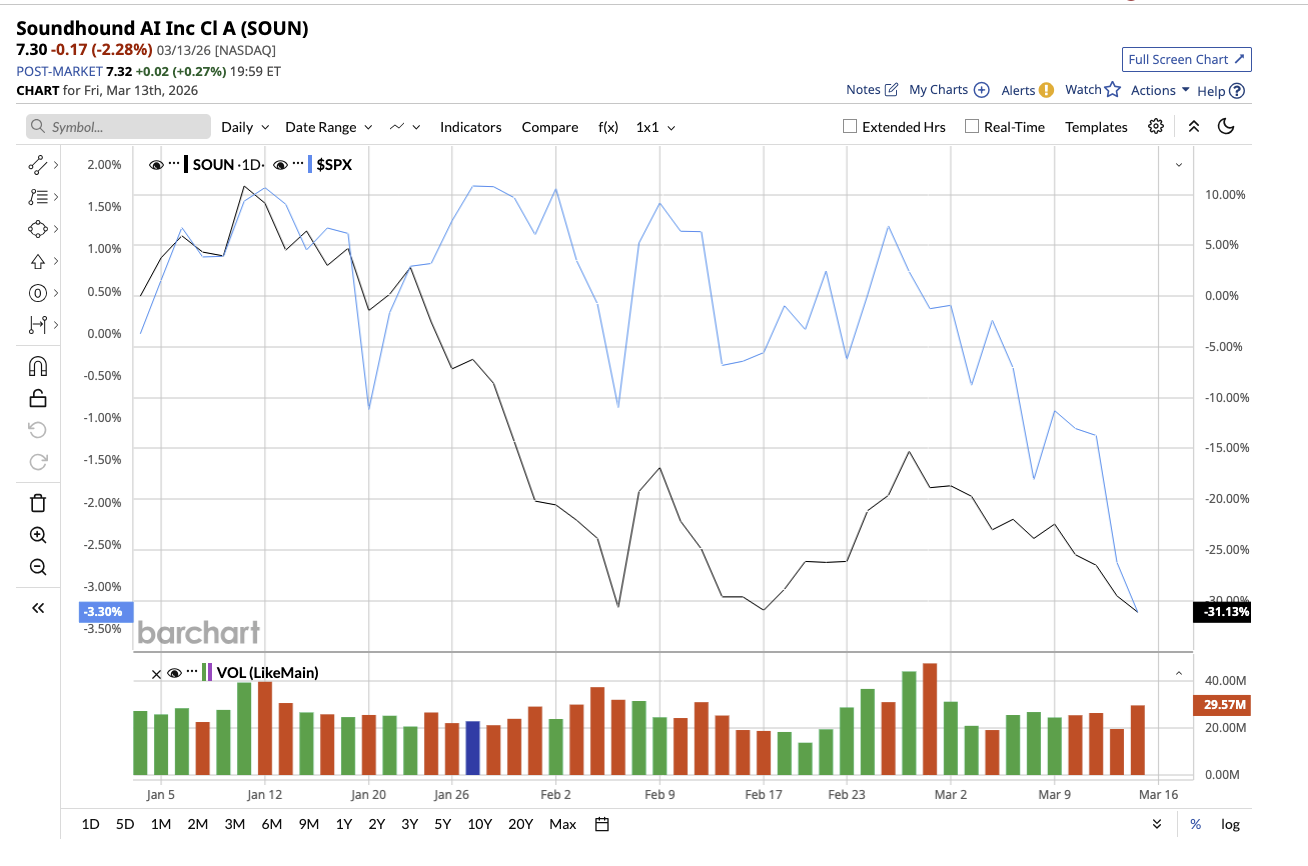

Artificial intelligence (AI) stocks have been among the biggest winners of the past few years. But many of the high-flying AI stocks have since come back down to earth as investor enthusiasm cooled in 2026. One such company is SoundHound AI (SOUN), whose stock has dropped roughly 66% from its 52-week high of $22.17 and now trades around $7, despite strong business momentum.

Does this selloff present a buying opportunity in a fast-growing pure-play AI company, or is it a sign to stay away?

Let’s find out.

Massive Customer Momentum Across Multiple Industries

Valued at $3.09 billion, SoundHound AI is a voice-based pure-play AI company focused on conversational AI and voice assistants for businesses. Its technology enables firms to integrate voice interaction directly into their goods, automobiles, customer support systems, and ordering platforms. Its primary offerings are the Houndify platform, SoundHound Chat AI, Smart Answering, and voice commerce tools.

SoundHound gained significantly as speech AI usage spread across many industries. Furthermore, Nvidia’s (NVDA) investment in the company brought it to the limelight. However, when Nvidia sold its stake in the company in 2024, it spooked investors, causing the stock to plummet.

While SOUN stock might have plummeted, its recent fourth quarter shows rapid growth across multiple industries, even as it continues navigating the challenges typical of emerging AI firms. In Q4, total revenue climbed 59% year-over-year (YoY) to $55.1 million. For the full year, the company reported 99% growth to $169 million. Over the past few years, SoundHound has managed to scale its revenue more than fivefold since becoming a public company in 2022.

One of the most notable achievements in Q4 was the company’s number of customer wins across different sectors. In Q4 alone, it signed more than 100 customer deals that span industries including automotive, telecommunications, healthcare, financial services, retail, government, and education. The automotive industry remains one of SoundHound’s most important growth drivers. The company signed multiple new automotive partners in Q4, including manufacturers from Japan, Korea, China, Vietnam, and Italy, as well as a commercial truck manufacturer.

Profitability Still Remains a Concern

Although SoundHound’s revenue growth is impressive, the company is still not consistently profitable. Besides the market's rotation out of AI stocks, this is one of the main reasons why SOUN stock is down 31% year-to-date (YTD). SoundHound reported an adjusted net loss of $7.3 million. Adjusted EBITDA losses narrowed to $7.4 million, marking a 56% improvement YoY. Adjusted gross margin stood at 61% in the quarter.

While losses have improved over last year, this remains a concern among investors looking for steady profits. The company has been focusing on improving efficiency by optimizing cloud spending, modernizing infrastructure, and shifting from third-party solutions to internally developed technologies. Management believes the business could eventually operate at gross margins above 70% and EBIT margins exceeding 30% once it reaches scale. On the balance sheet, SoundHound remains sound for now. It ended the quarter with $248 million in cash and no debt, giving the company financial flexibility to continue investing in growth initiatives while working toward profitability.

SoundHound's Strong Outlook for 2026

Looking ahead, SoundHound expects another year of strong growth, with 2026 revenue between $225 million and $260 million, reflecting continued expansion across its enterprise AI, automotive, restaurant, and voice commerce businesses. The company believes the increasing adoption of generative AI, agentic AI, and voice-based automation is creating a massive market opportunity.

While SoundHound has a first-mover advantage in the conversational AI and voice assistant space, this space is also becoming competitive. Major tech titans like Alphabet (GOOG) (GOOGL), Microsoft (MSFT), Amazon (AMZN), and Apple (AAPL) have massive resources to give SoundHound stiff competition.

The company is still in its growth phase and continues to invest heavily in research, development, and market expansion. While losses are narrowing and profitability is on the cards soon, sustaining these profits still could be a challenge, and investors should expect some volatility.

SOUN Stock: Buy the Dip or Stay Away?

Investors who believe SoundHound can convert its fast-growing AI platform into sustainable profits and are willing to handle the short-term volatility may want to hold on to the stock or accumulate shares at this dip. However, more conservative investors may prefer to wait for clearer evidence of sustained profitability before jumping into a stock that has already experienced significant volatility this year.

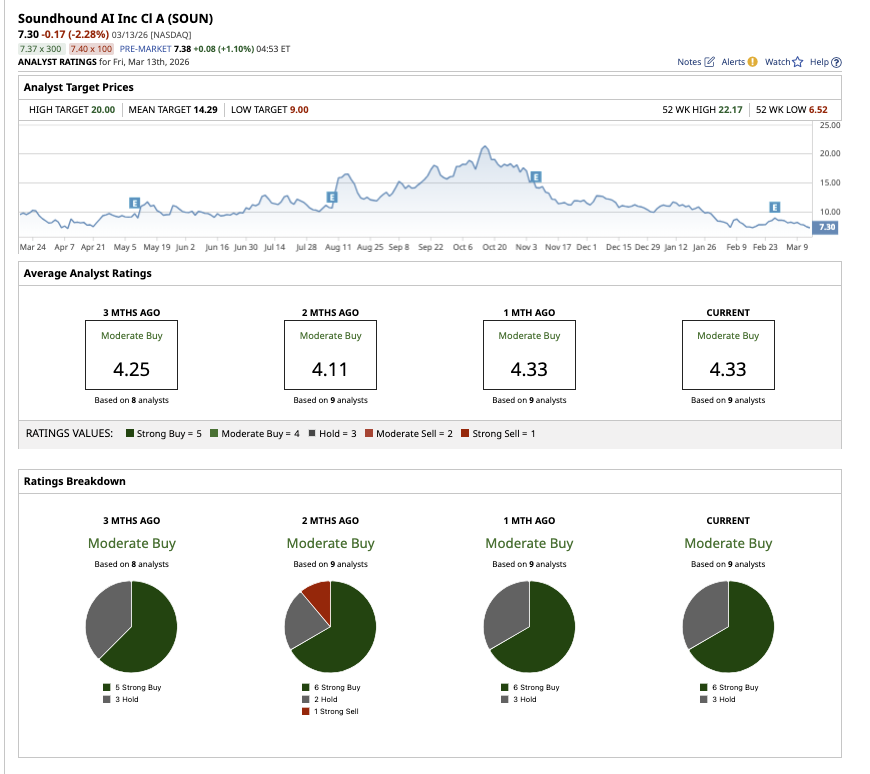

Overall, Wall Street rates SOUN stock a “Moderate Buy.” Out of the nine analysts covering SOUN, six rate it a “Strong Buy,” and three have given it a “Hold” rating. Its average target price of $14.29 suggests an upside potential of 96% from current levels. However, analysts have assigned a high price estimate of $20, which implies the stock could rally to 174% over the next 12 months.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart