Nvidia (NVDA) released its fiscal Q4 2026 earnings on Wednesday, Feb. 25, after the close of markets. It was the “usual” report that we have been so accustomed to for the last three years. The company’s revenues and profits soared past estimates, and it provided an upbeat guidance that was well ahead of Street estimates.

However, as has usually been the case with NVDA, even a blowout earnings report failed to take the stock higher. While the shares were trading flattish in after-hours on Wednesday, they closed down over 5% on Thursday and another 4% on Friday but are recovering a little in this morning's trading session. Let's examine this disconnect between Nvidia’s otherwise strong earnings report and the price action and analyze whether you should buy the dip in NVDA.

Nvidia Expects Growth to Accelerate in the Current Quarter

Nvidia’s revenues rose 73% year-over-year (YoY) in fiscal Q4 and 65% in the full year. For the current quarter, it guided for revenues of $78 billion at the midpoint, which was ahead of even the most bullish projections and implies growth accelerating to 77%. Importantly, the guidance does not assume any sales to China. While Nvidia’s margins in the last fiscal year contracted to 71.3% as it ramped up Blackwell production, the company expects the metric to be at 74.9% at the midpoint in the current quarter.

NVDA Stock Forecast

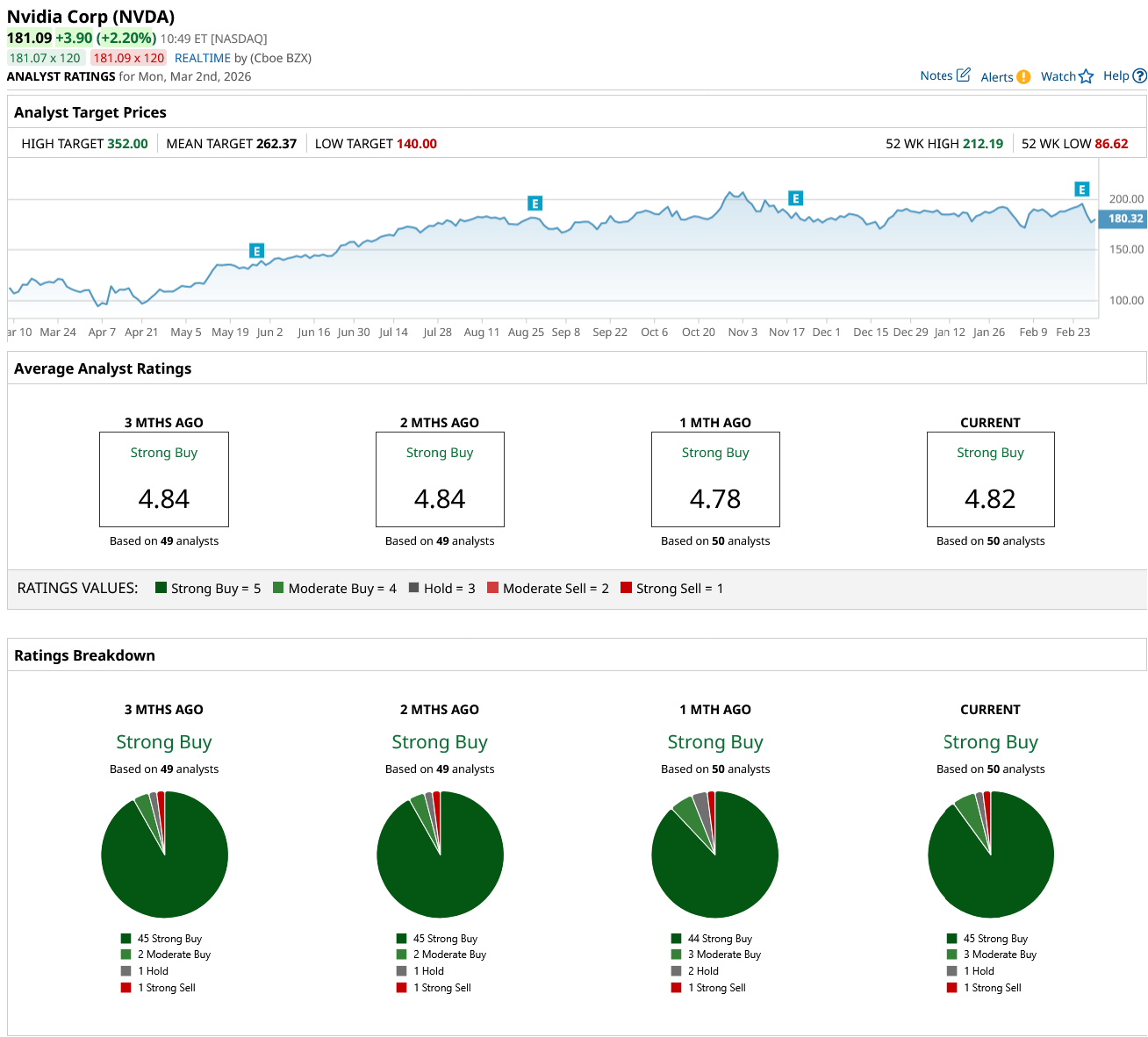

While markets sent NVDA stock southwards following the fiscal Q4 report, sell-side analysts were not perturbed and did pretty much the same thing they have been doing for the last many quarters—raise Nvidia’s target price. However, the intensity of price hikes has been a lot milder of late.

Bernstein, Baird, and Bank of America raised their target prices from $275 to $300, while Citi raised its target from $270 to $300. Rosenblatt also raised its target price from $245 to $300, which was the highest increase in percentage terms from major brokerages.

Why NVDA Stock Fell After a Blowout Earnings Report

While the reaction to Nvidia’s earnings wasn’t what one would expect after such a blowout quarter, there are reasons why markets reacted that way. Firstly, the bar is always set high for Nvidia, and markets expect more than a mere earnings beat from the world’s biggest company.

Also, while the fiscal Q1 guide was impressive and surpassed estimates, it wasn’t totally unexpected considering the spending spree of hyperscalers who have opened their purse strings for artificial intelligence (AI) capex as if there’s no tomorrow.

Then there is the sustainability question, which has been lingering along for quite some time now, as the AI spending spree, particularly of hyperscalers, might not continue in perpetuity, and investors are no longer cheering their growing capex, as was well evident in the recent earnings calls. Revenue concentration has been a concern for Nvidia, especially as some of its biggest buyers are developing AI chips and are also looking at alternative suppliers to lower their reliance on the company.

China remains a wild card for Nvidia, and there is considerable uncertainty over its prospects in that country, which was once its second-biggest market after the U.S.

Nvidia tried to address some of these issues and highlighted how its demand profile is getting diversified as non-hyperscalers ramp up purchases. It also noted the growth in sovereign AI and said that the business tripled to over $30 billion in the last fiscal year.

It also discussed physical AI and said it generated $6 billion in revenue in the last fiscal year. The company also touted the revenue opportunity from autonomous cars as companies ranging from Tesla (TSLA) to Alphabet (GOOG) (GOOGL)-backed Waymo and Uber (UBER) continue to scale up robotaxi operations.

Here’s Why It Makes Sense to Buy the Dip in NVDA Stock

For quite some time now, I have been noting that investors should temper their expectations for NVDA stock and not expect it to keep doubling every year. However, I find Nvidia’s short-term risk-reward quite attractive after the post-earnings selloff, and while there are genuine concerns over the sustainability of Nvidia's revenues, at a forward price-to-earnings (P/E) multiple of 27.2x, I find a reasonable margin of safety in the stock.

Also, while the other Magnificent 7 peers are struggling to grow their bottom line largely due to the soaring depreciation expenses on the billions they are spending on building the AI infrastructure—much of which lands into Nvidia’s coffers—Nvidia’s earnings are expected to rise nearly 60% this fiscal year, which gives us a P/E-to-growth (PEG) multiple of 0.58x. As things stand currently, I don’t expect Nvidia to hit $300 levels anytime soon. However, the post-earnings selloff does look like a buying opportunity to me.

On the date of publication, Mohit Oberoi had a position in: NVDA , GOOG , TSLA . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart