Looking back on apparel retailer stocks’ Q2 earnings, we examine this quarter’s best and worst performers, including Lululemon (NASDAQ: LULU) and its peers.

Apparel sales are not driven so much by personal needs but by seasons, trends, and innovation, and over the last few decades, the category has shifted meaningfully online. Retailers that once only had brick-and-mortar stores are responding with omnichannel presences. The online shopping experience continues to improve and retail foot traffic in places like shopping malls continues to stall, so the evolution of clothing sellers marches on.

The 9 apparel retailer stocks we track reported a strong Q2. As a group, revenues beat analysts’ consensus estimates by 1.1% while next quarter’s revenue guidance was in line.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 9.3% since the latest earnings results.

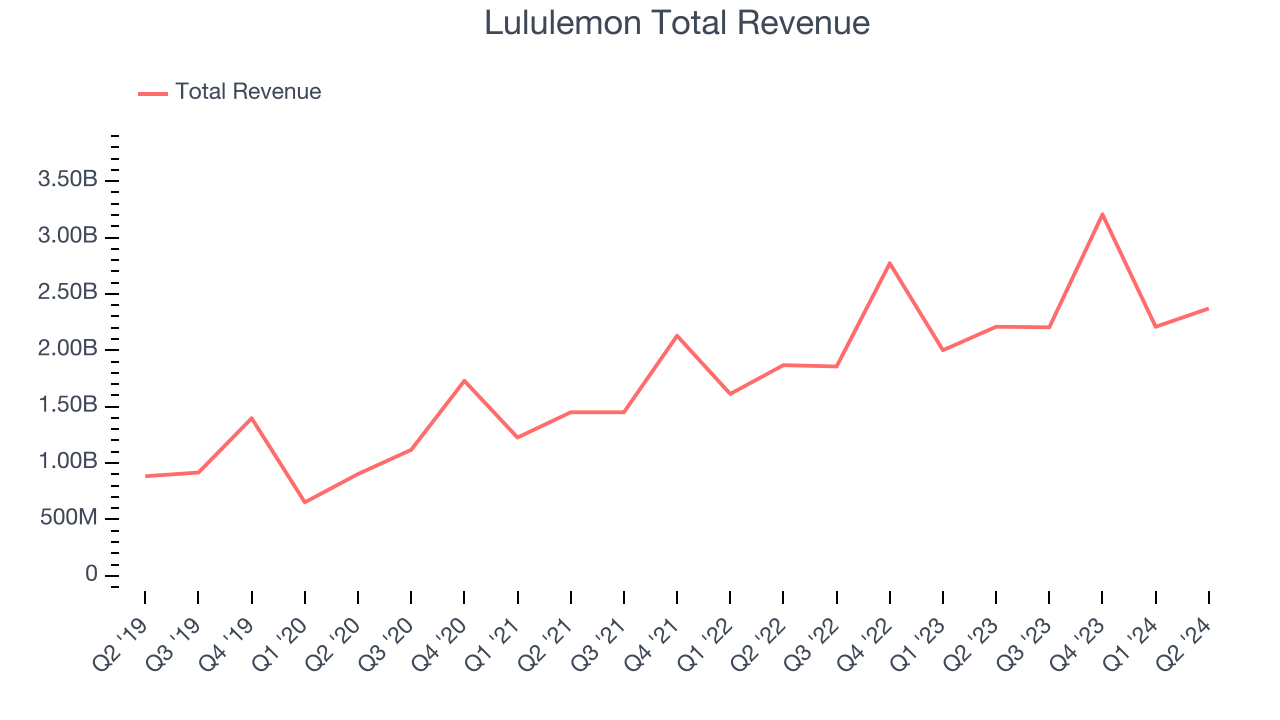

Lululemon (NASDAQ: LULU)

Originally serving yogis and hockey players, Lululemon (NASDAQ: LULU) is a designer, distributor, and retailer of athletic apparel for men and women.

Lululemon reported revenues of $2.37 billion, up 7.3% year on year. This print fell short of analysts’ expectations by 1.5%. Overall, it was a mixed quarter for the company with an impressive beat of analysts’ EBITDA estimates but full-year revenue guidance missing analysts’ expectations.

Calvin McDonald, Chief Executive Officer, stated: "In the second quarter, lululemon delivered revenue and earnings growth, with ongoing strength across our international business. In the U.S., our teams continue to optimize our product assortment and remain focused on driving forward our opportunities in the market. Looking ahead, we feel confident in the long runway in front of us as we execute on our Power of Three ×2 growth plan."

Lululemon delivered the weakest performance against analyst estimates and weakest full-year guidance update of the whole group. Interestingly, the stock is up 23.9% since reporting and currently trades at $320.89.

Is now the time to buy Lululemon? Access our full analysis of the earnings results here, it’s free.

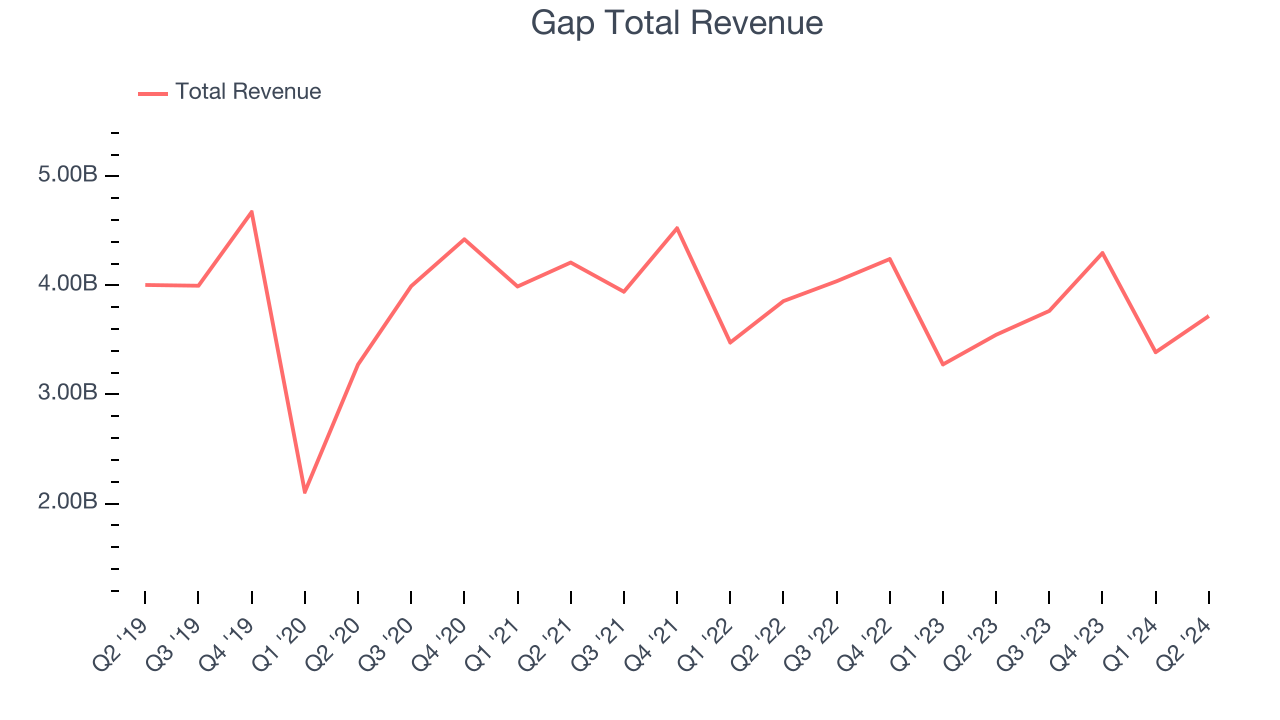

Best Q2: Gap (NYSE: GAP)

Operating under The Gap, Old Navy, Banana Republic, and Athleta brands, The Gap (NYSE: GAP) is an apparel and accessories retailer that sells its own brand of casual clothing to men, women, and children.

Gap reported revenues of $3.72 billion, up 4.8% year on year, outperforming analysts’ expectations by 2.6%. The business had a stunning quarter with an impressive beat of analysts’ earnings and EBITDA estimates.

Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 4.3% since reporting. It currently trades at $21.47.

Is now the time to buy Gap? Access our full analysis of the earnings results here, it’s free.

Weakest Q2: American Eagle (NYSE: AEO)

With a heavy focus on denim, American Eagle Outfitters (NYSE: AEO) is a specialty retailer offering an assortment of apparel and accessories to young adults.

American Eagle reported revenues of $1.29 billion, up 7.5% year on year, falling short of analysts’ expectations by 1.4%. It was a slower quarter as it posted a miss of analysts’ EBITDA and gross margin estimates.

As expected, the stock is down 8.4% since the results and currently trades at $19.86.

Read our full analysis of American Eagle’s results here.

Urban Outfitters (NASDAQ: URBN)

Founded as a purveyor of vintage items, Urban Outfitters (NASDAQ: URBN) now largely sells new apparel and accessories to teens and young adults seeking on-trend fashion.

Urban Outfitters reported revenues of $1.35 billion, up 6.3% year on year. This print topped analysts’ expectations by 1%. It was an exceptional quarter as it also put up an impressive beat of analysts’ EBITDA estimates.

The stock is down 13.4% since reporting and currently trades at $35.95.

Read our full, actionable report on Urban Outfitters here, it’s free.

Abercrombie and Fitch (NYSE: ANF)

Founded as an outdoor and sporting brand, Abercrombie & Fitch (NYSE: ANF) evolved to become a specialty retailer that sells its own brand of fashionable clothing to young adults.

Abercrombie and Fitch reported revenues of $1.13 billion, up 21.2% year on year. This print surpassed analysts’ expectations by 4.1%. It was a very strong quarter as it also put up an impressive beat of analysts’ EBITDA estimates and a decent beat of analysts’ earnings estimates.

Abercrombie and Fitch pulled off the biggest analyst estimates beat and fastest revenue growth among its peers. The stock is down 18.2% since reporting and currently trades at $136.48.

Read our full, actionable report on Abercrombie and Fitch here, it’s free.

Market Update

The Fed cut its policy rate by 50bps (half a percent) in September 2024, the first in roughly four years. This marks the end of its most pointed inflation-busting campaign since the 1980s. While CPI (inflation) readings have been supportive lately, employment measures have bordered on worrisome. The markets will be assessing whether this rate cut's timing (and more potential ones in 2024 and 2025) is ideal for supporting the economy or a bit too late for a macro that has already cooled too much.

Want to invest in winners with rock-solid fundamentals? Check out our 9 Best Market-Beating Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.