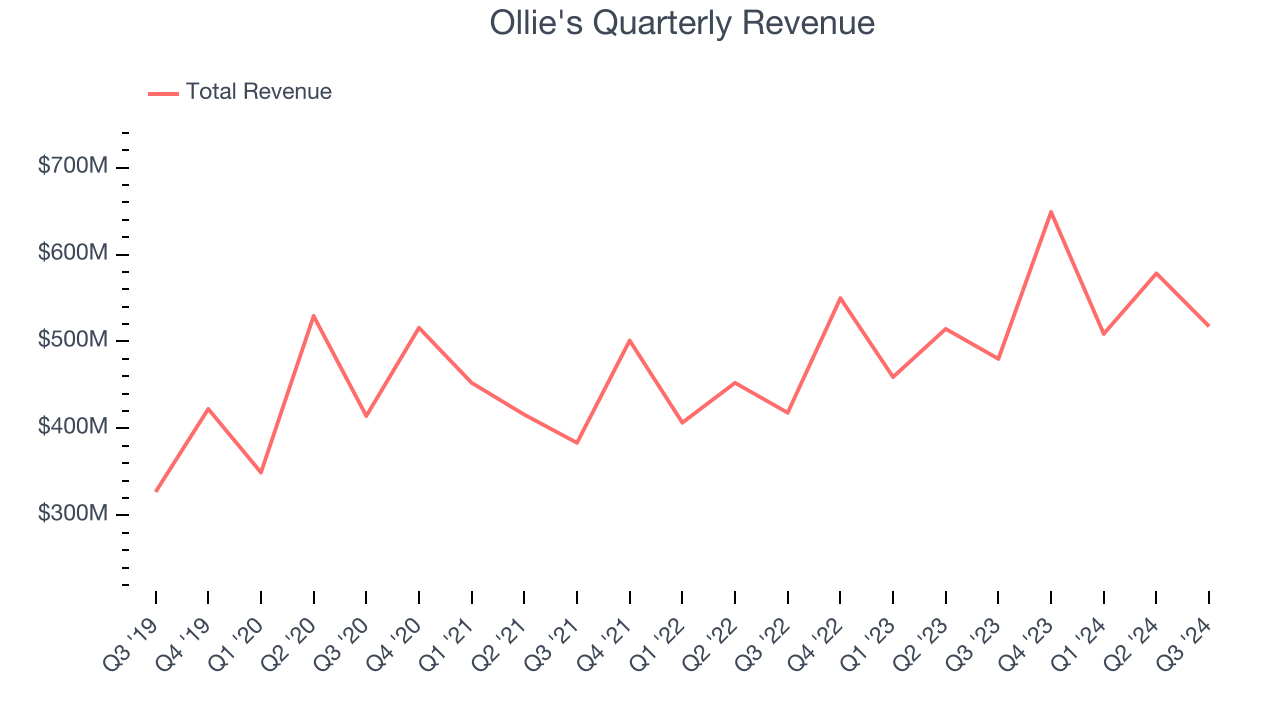

Discount retail company Ollie’s Bargain Outlet (NASDAQ: OLLI) met Wall Street’s revenue expectations in Q3 CY2024, with sales up 7.8% year on year to $517.4 million. The company’s outlook for the full year was close to analysts’ estimates with revenue guided to $2.28 billion at the midpoint. Its non-GAAP profit of $0.58 per share was in line with analysts’ consensus estimates.

Is now the time to buy Ollie's? Find out by accessing our full research report, it’s free.

Ollie's (OLLI) Q3 CY2024 Highlights:

- Revenue: $517.4 million vs analyst estimates of $519.5 million (7.8% year-on-year growth, in line)

- Adjusted EPS: $0.58 vs analyst estimates of $0.57 (in line)

- Adjusted EBITDA: $59.84 million vs analyst estimates of $56.44 million (11.6% margin, 6% beat)

- The company reconfirmed its revenue guidance for the full year of $2.28 billion at the midpoint

- Management reiterated its full-year Adjusted EPS guidance of $3.26 at the midpoint

- Operating Margin: 8.6%, in line with the same quarter last year

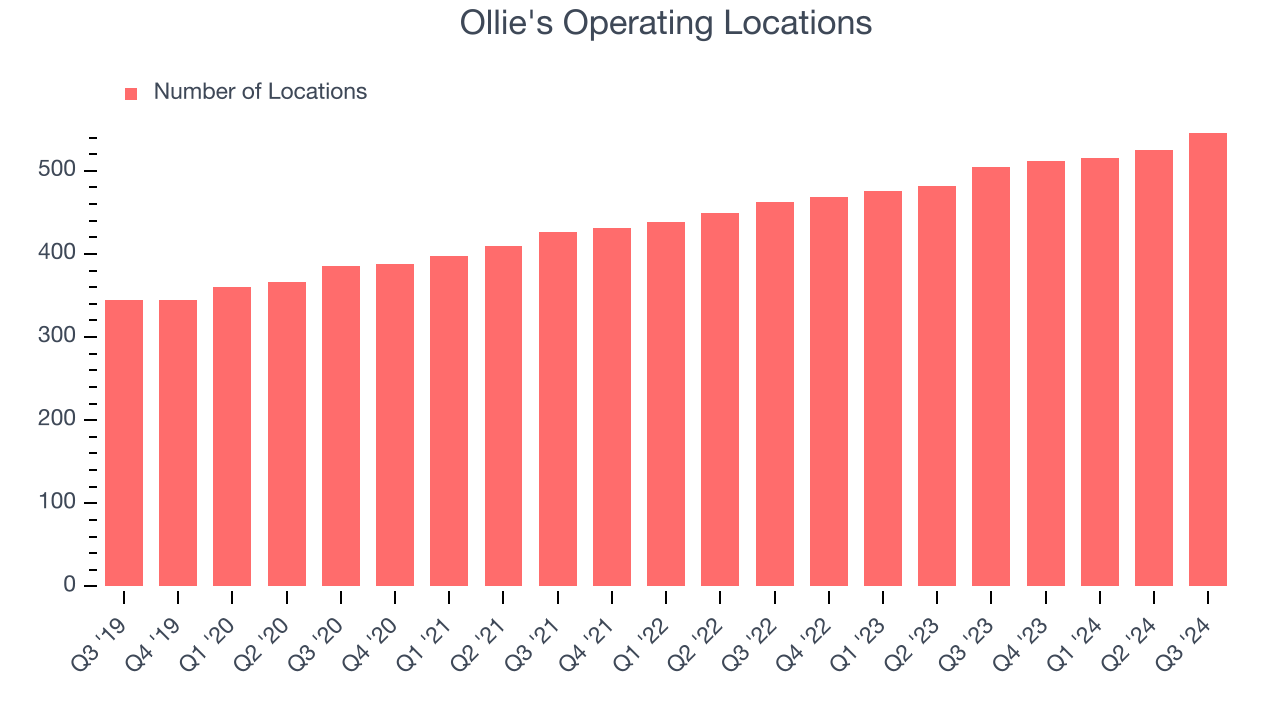

- Locations: 546 at quarter end, up from 505 in the same quarter last year

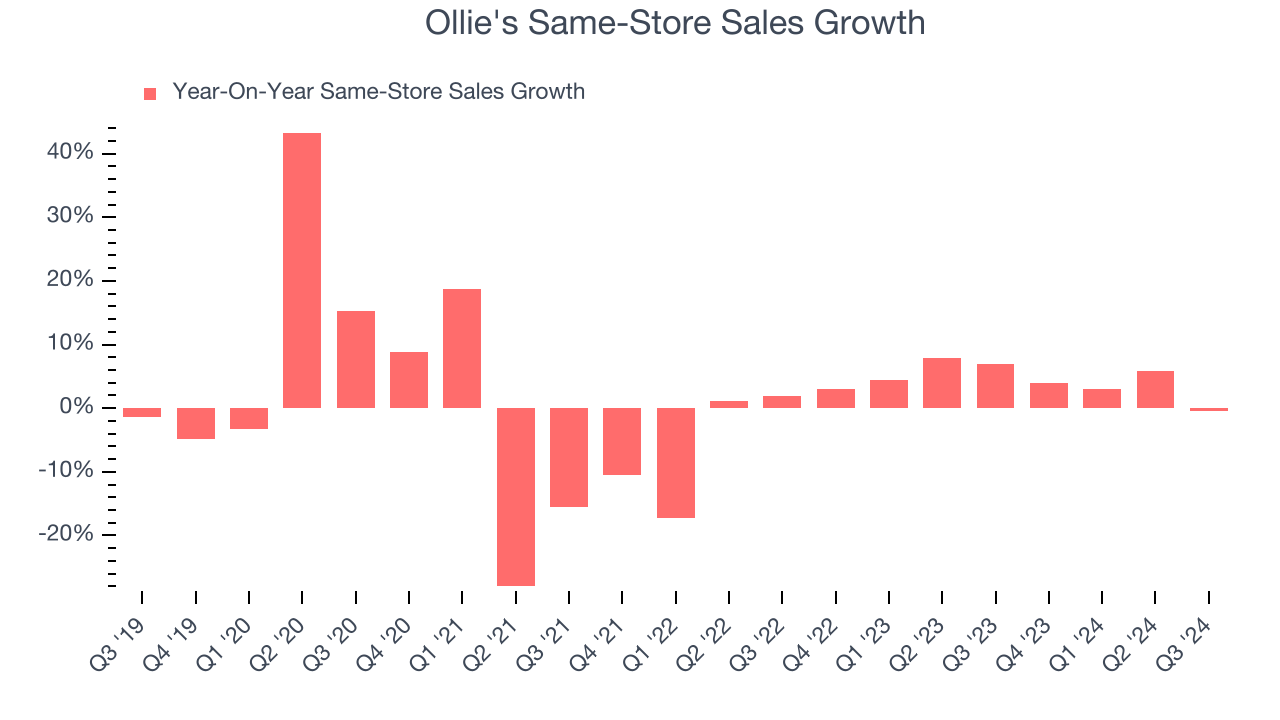

- Same-Store Sales were flat year on year (7% in the same quarter last year)

- Market Capitalization: $6.02 billion

“We had another great quarter and are pleased with our results. We delivered strong earnings on higher sales, gross margin, and disciplined expense control. We also took advantage of a number of real estate opportunities that strengthened our new store pipeline and enhanced our competitive positioning for the future,” said John Swygert, Chief Executive Officer.

Company Overview

Often located in suburban or semi-rural shopping centers, Ollie’s Bargain Outlet (NASDAQ: OLLI) is a discount retailer that acquires excess inventory then sells at meaningful discounts.

Discount Retailer

Discount retailers understand that many shoppers love a good deal, and they focus on providing excellent value to shoppers by selling general merchandise at major discounts. They can do this because of unique purchasing, procurement, and pricing strategies that involve scouring the market for trendy goods or buying excess inventory from manufacturers and other retailers. They then turn around and sell these snacks, paper towels, toys, clothes, and myriad other products at highly enticing prices. Despite the unique draw and lure of discounts, these discount retailers must also contend with the secular headwinds of online shopping and challenged retail foot traffic in places like suburban strip malls.

Sales Growth

A company’s long-term sales performance signals its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

Ollie's is a small retailer, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage. On the other hand, it can grow faster because it’s working from a smaller revenue base and has more white space to build new stores.

As you can see below, Ollie’s 10.3% annualized revenue growth over the last five years (we compare to 2019 to normalize for COVID-19 impacts) was decent as it opened new stores and increased sales at existing, established locations.

This quarter, Ollie's grew its revenue by 7.8% year on year, and its $517.4 million of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 9.6% over the next 12 months, similar to its five-year rate. This projection is noteworthy and indicates the market is factoring in success for its products.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Store Performance

Number of Stores

The number of stores a retailer operates is a critical driver of how quickly company-level sales can grow.

Ollie's sported 546 locations in the latest quarter. Over the last two years, it has opened new stores at a rapid clip by averaging 8.5% annual growth, among the fastest in the consumer retail sector. This gives it a chance to scale into a mid-sized business over time.

When a retailer opens new stores, it usually means it’s investing for growth because demand is greater than supply, especially in areas where consumers may not have a store within reasonable driving distance.

Same-Store Sales

A company's store base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales is an industry measure of whether revenue is growing at those existing stores and is driven by customer visits (often called traffic) and the average spending per customer (ticket).

Ollie’s demand has been spectacular for a retailer over the last two years. On average, the company has increased its same-store sales by an impressive 4.3% per year. This performance suggests its rollout of new stores is beneficial for shareholders. We like this backdrop because it gives Ollie's multiple ways to win: revenue growth can come from new stores, e-commerce, or increased foot traffic and higher sales per customer at existing locations.

In the latest quarter, Ollie’s year on year same-store sales were flat. This was a meaningful deceleration from its historical levels. We’ll be watching closely to see if Ollie's can reaccelerate growth.

Key Takeaways from Ollie’s Q3 Results

We enjoyed seeing Ollie's exceed analysts’ operating profit expectations this quarter. We were also happy its gross margin narrowly outperformed Wall Street’s estimates. Revenue was in line and the company reconfirmed its full year revenue guidance, Overall, this quarter had some key positives. The stock traded up 2.9% to $101 immediately following the results.

Should you buy the stock or not? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.