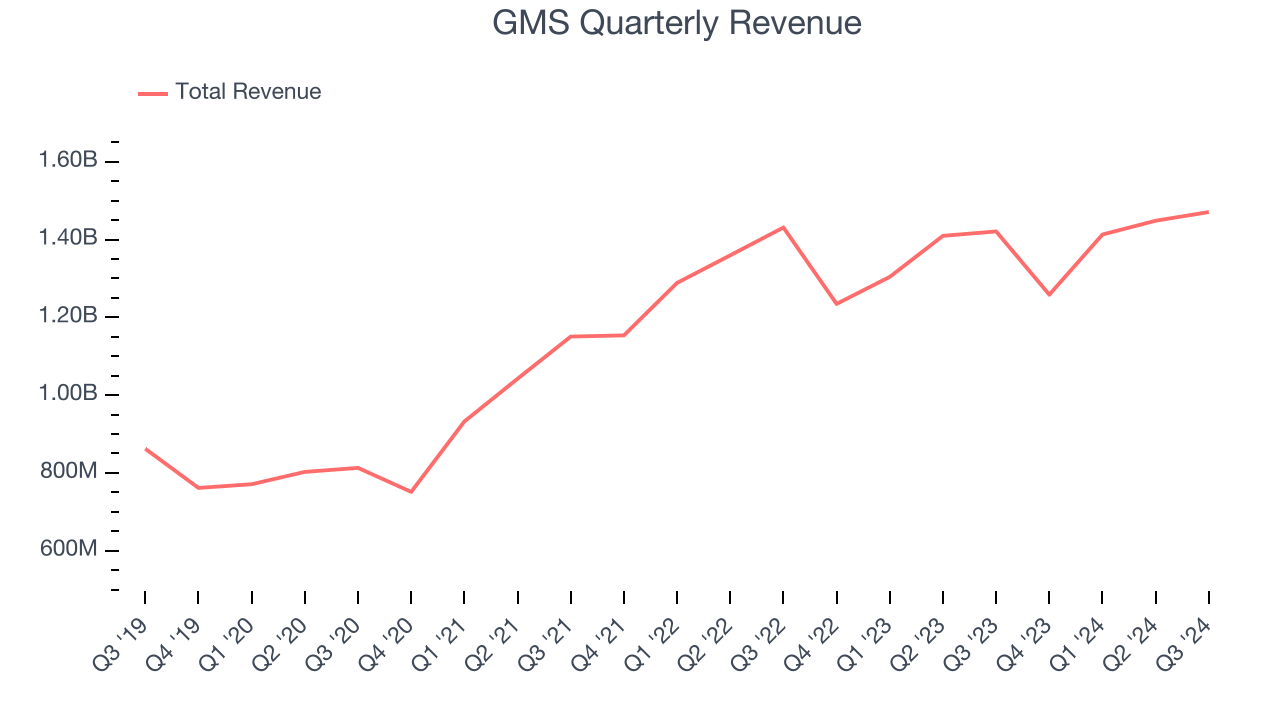

Building materials distributor GMS (NYSE: GMS) reported Q3 CY2024 results beating Wall Street’s revenue expectations, with sales up 3.5% year on year to $1.47 billion. Its non-GAAP profit of $2.02 per share was 7.8% below analysts’ consensus estimates.

Is now the time to buy GMS? Find out by accessing our full research report, it’s free.

GMS (GMS) Q3 CY2024 Highlights:

- Revenue: $1.47 billion vs analyst estimates of $1.46 billion (3.5% year-on-year growth, 0.5% beat)

- Adjusted EPS: $2.02 vs analyst expectations of $2.19 (7.8% miss)

- Adjusted EBITDA: $152.2 million vs analyst estimates of $162.1 million (10.3% margin, 6.1% miss)

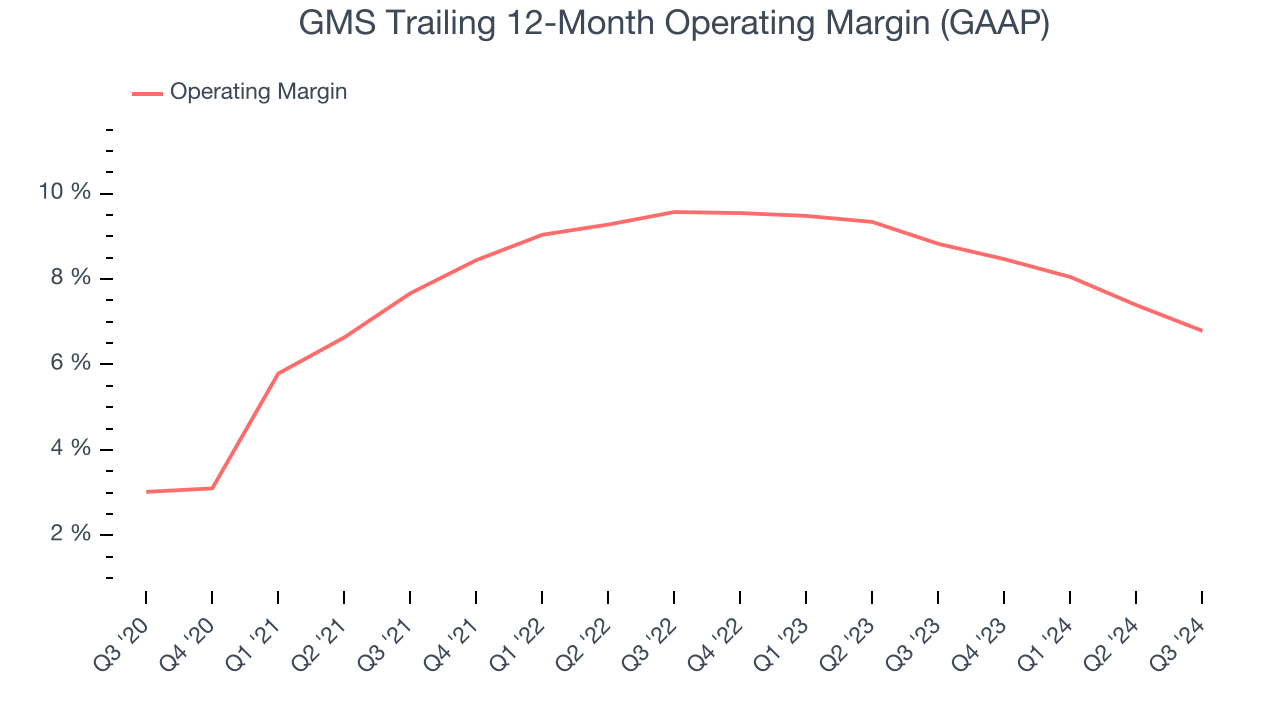

- Operating Margin: 6.4%, down from 8.8% in the same quarter last year

- Free Cash Flow Margin: 6.9%, similar to the same quarter last year

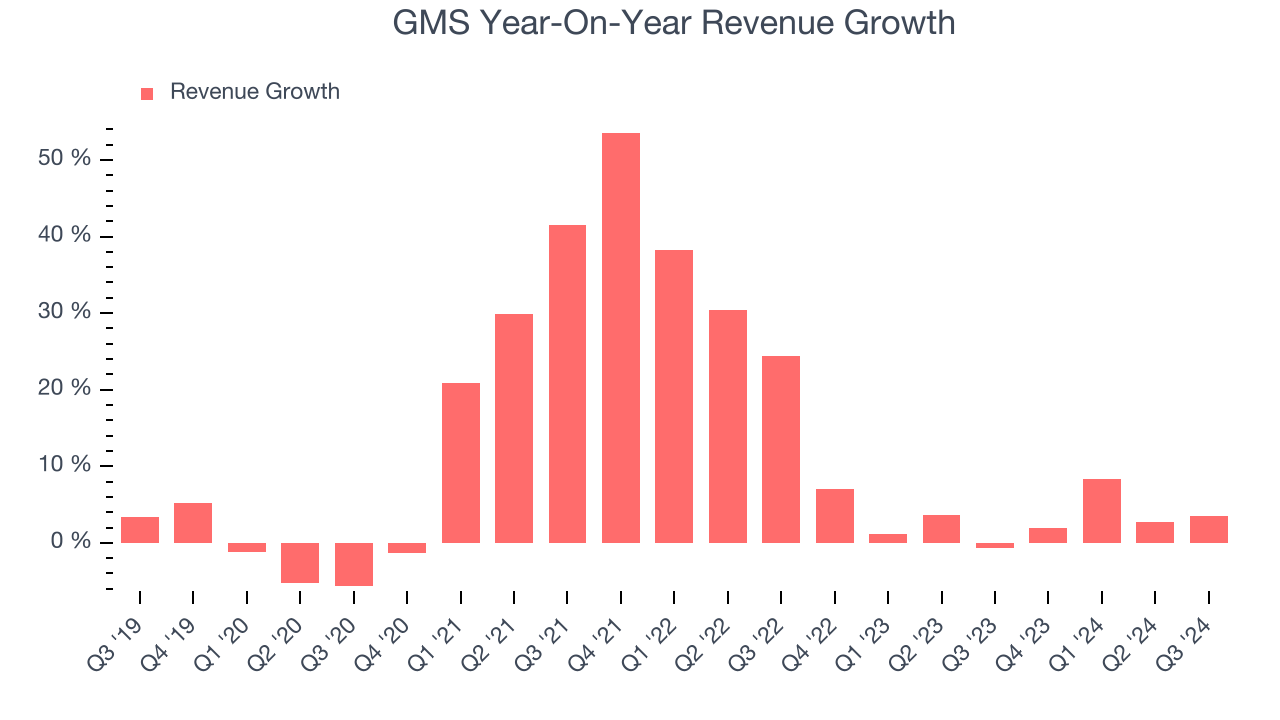

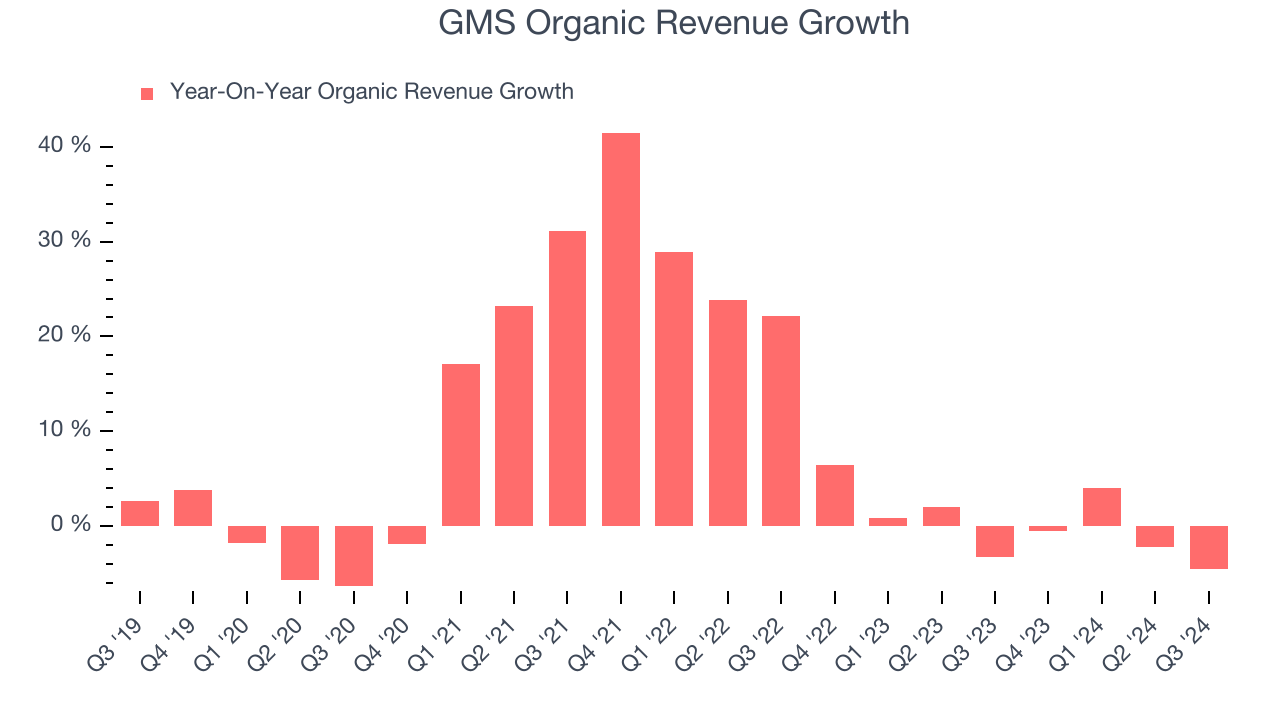

- Organic Revenue fell 4.6% year on year (-3.2% in the same quarter last year)

- Market Capitalization: $4.02 billion

“During our second quarter of fiscal 2025, the GMS team delivered net sales of $1.5 billion, net income of $53.5 million and Adjusted EBITDA of $152.2 million, reflecting the team’s continued ability to effectively navigate a challenging and dynamic operating environment,” said John C. Turner, Jr., President and CEO of GMS.

Company Overview

Founded in 1971, GMS (NYSE: GMS) distributes specialty building materials including wallboard, ceilings, and insulation products, to the construction industry.

Building Material Distributors

Supply chain and inventory management are themes that grew in focus after COVID wreaked havoc on the global movement of raw materials and components. Building materials distributors that boast reliable selection and quickly deliver products to customers can benefit from this theme. While e-commerce hasn’t disrupted industrial distribution as much as consumer retail, it is forcing investment in digital capabilities to communicate with and serve customers everywhere. Additionally, building materials distributors are at the whim of economic cycles that impact the capital spending and construction projects that can juice demand.

Sales Growth

A company’s long-term performance is an indicator of its overall quality. While any business can experience short-term success, top-performing ones enjoy sustained growth for years. Over the last five years, GMS grew its sales at an impressive 11.7% compounded annual growth rate. Its growth beat the average industrials company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. GMS’s recent history shows its demand slowed significantly as its annualized revenue growth of 3.4% over the last two years is well below its five-year trend.

GMS also reports organic revenue, which strips out one-time events like acquisitions and currency fluctuations because they don’t accurately reflect its fundamentals. Over the last two years, GMS’s organic revenue was flat. Because this number is lower than its normal revenue growth, we can see that some mixture of acquisitions and foreign exchange rates boosted its headline results.

This quarter, GMS reported modest year-on-year revenue growth of 3.5% but beat Wall Street’s estimates by 0.5%.

Looking ahead, sell-side analysts expect revenue to grow 3% over the next 12 months, similar to its two-year rate. This projection is underwhelming and suggests its newer products and services will not catalyze better top-line performance yet.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

GMS was profitable over the last five years but held back by its large cost base. Its average operating margin of 7.5% was weak for an industrials business.

On the plus side, GMS’s operating margin rose by 3.8 percentage points over the last five years, as its sales growth gave it operating leverage.

In Q3, GMS generated an operating profit margin of 6.4%, down 2.3 percentage points year on year. Since GMS’s operating margin decreased more than its gross margin, we can assume it was recently less efficient because expenses such as marketing, R&D, and administrative overhead increased.

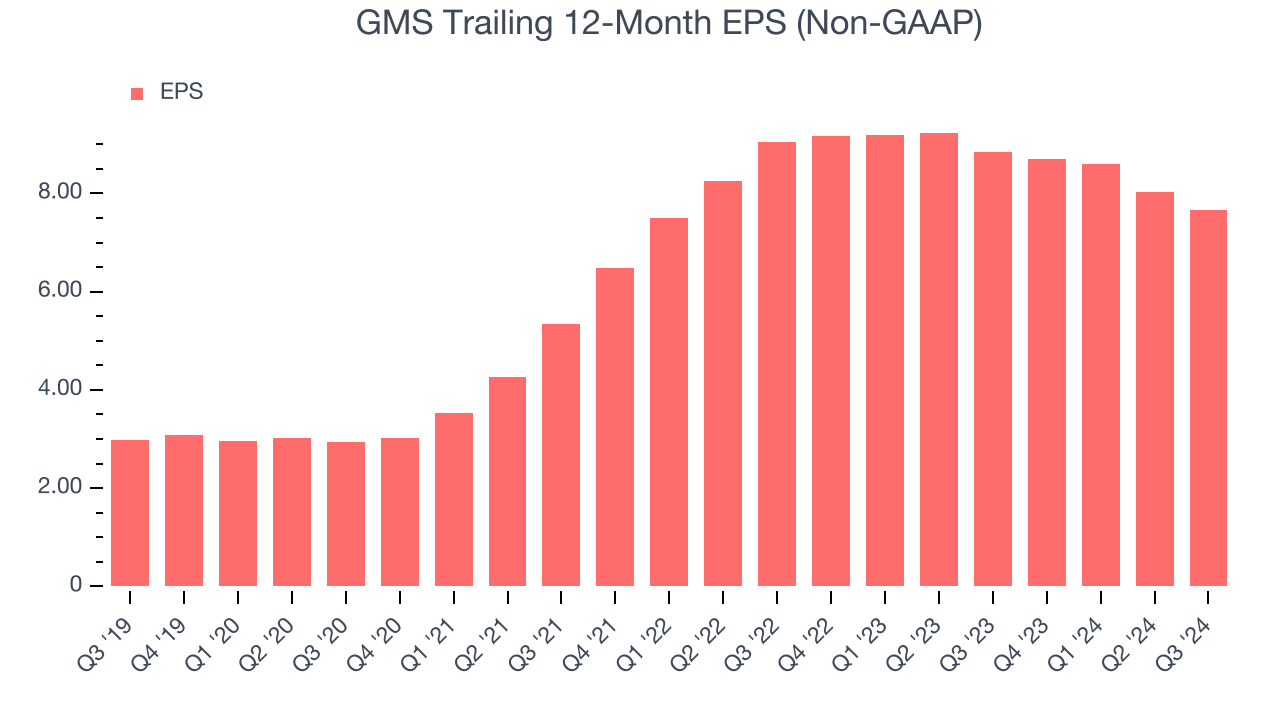

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

GMS’s EPS grew at an astounding 20.8% compounded annual growth rate over the last five years, higher than its 11.7% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

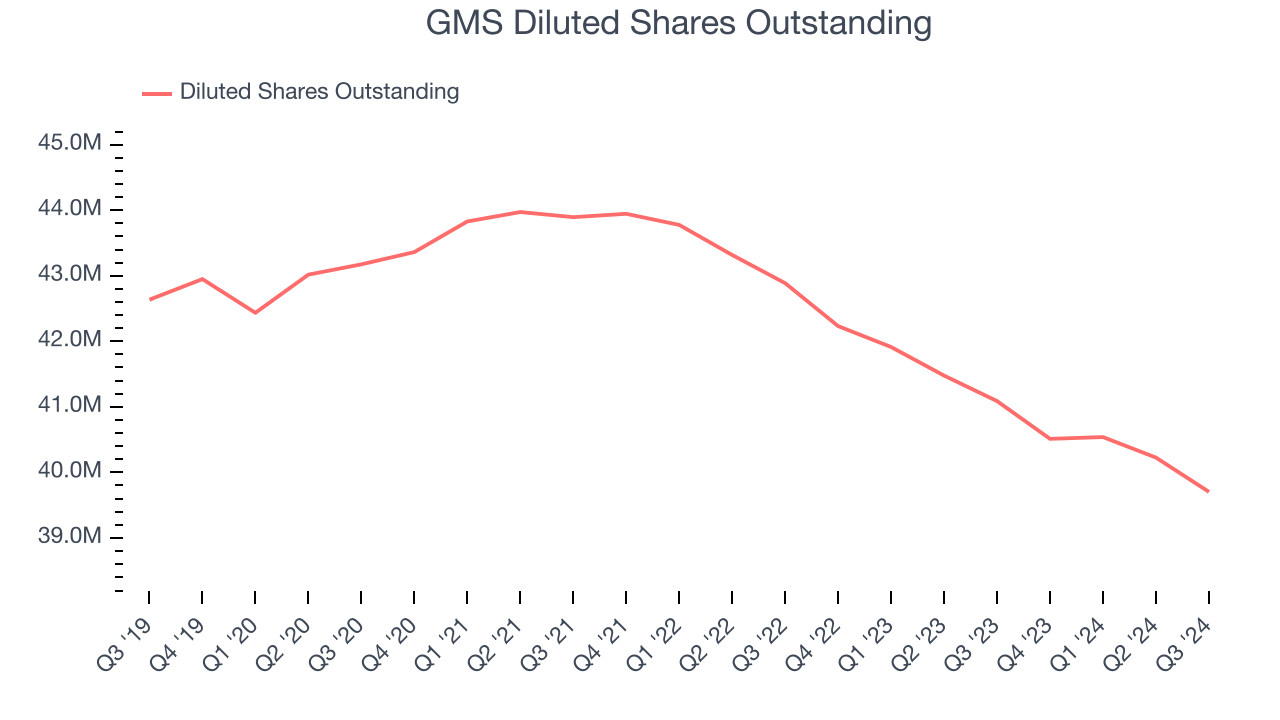

Diving into the nuances of GMS’s earnings can give us a better understanding of its performance. As we mentioned earlier, GMS’s operating margin declined this quarter but expanded by 3.8 percentage points over the last five years. Its share count also shrank by 6.9%, and these factors together are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For GMS, its two-year annual EPS declines of 8% mark a reversal from its (seemingly) healthy five-year trend. We hope GMS can return to earnings growth in the future.In Q3, GMS reported EPS at $2.02, down from $2.40 in the same quarter last year. This print missed analysts’ estimates, but we care more about long-term EPS growth than short-term movements. Over the next 12 months, Wall Street expects GMS’s full-year EPS of $7.66 to grow 4.9%.

Key Takeaways from GMS’s Q3 Results

We were impressed by how significantly GMS blew past analysts’ organic revenue expectations this quarter. On the other hand, its EBITDA and EPS fell short of Wall Street’s estimates. Overall, this was a mixed quarter. The stock remained flat at $101.26 immediately following the results.

Should you buy the stock or not? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.