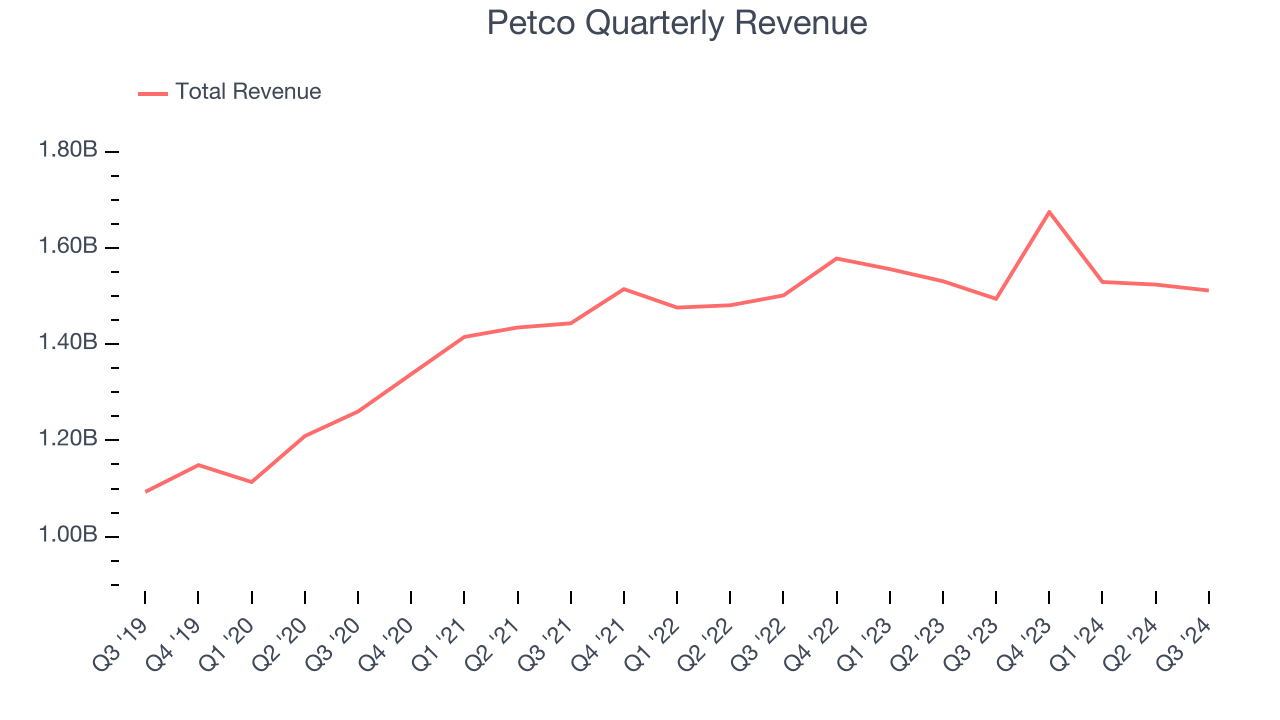

Pet-focused retailer Petco (NASDAQ: WOOF) reported Q3 CY2024 results topping the market’s revenue expectations, with sales up 1.2% year on year to $1.51 billion. On the other hand, next quarter’s revenue guidance of $1.55 billion was less impressive, coming in 1.5% below analysts’ estimates. Its non-GAAP loss of $0.02 per share was $0.01 above analysts’ consensus estimates.

Is now the time to buy Petco? Find out by accessing our full research report, it’s free.

Petco (WOOF) Q3 CY2024 Highlights:

- Revenue: $1.51 billion vs analyst estimates of $1.50 billion (1.2% year-on-year growth, 0.7% beat)

- Adjusted EPS: -$0.02 vs analyst estimates of -$0.03 ($0.01 beat)

- Adjusted EBITDA: $81.24 million vs analyst estimates of $78.73 million (5.4% margin, 3.2% beat)

- Revenue Guidance for Q4 CY2024 is $1.55 billion at the midpoint, below analyst estimates of $1.57 billion

- Adjusted EPS guidance for Q4 CY2024 is $0.01 at the midpoint, below analyst estimates of $0.04

- EBITDA guidance for Q4 CY2024 is $92.5 million at the midpoint, below analyst estimates of $101.6 million

- Operating Margin: 0.3%, up from -82.5% in the same quarter last year

- Free Cash Flow was -$10.29 million compared to -$28.08 million in the same quarter last year

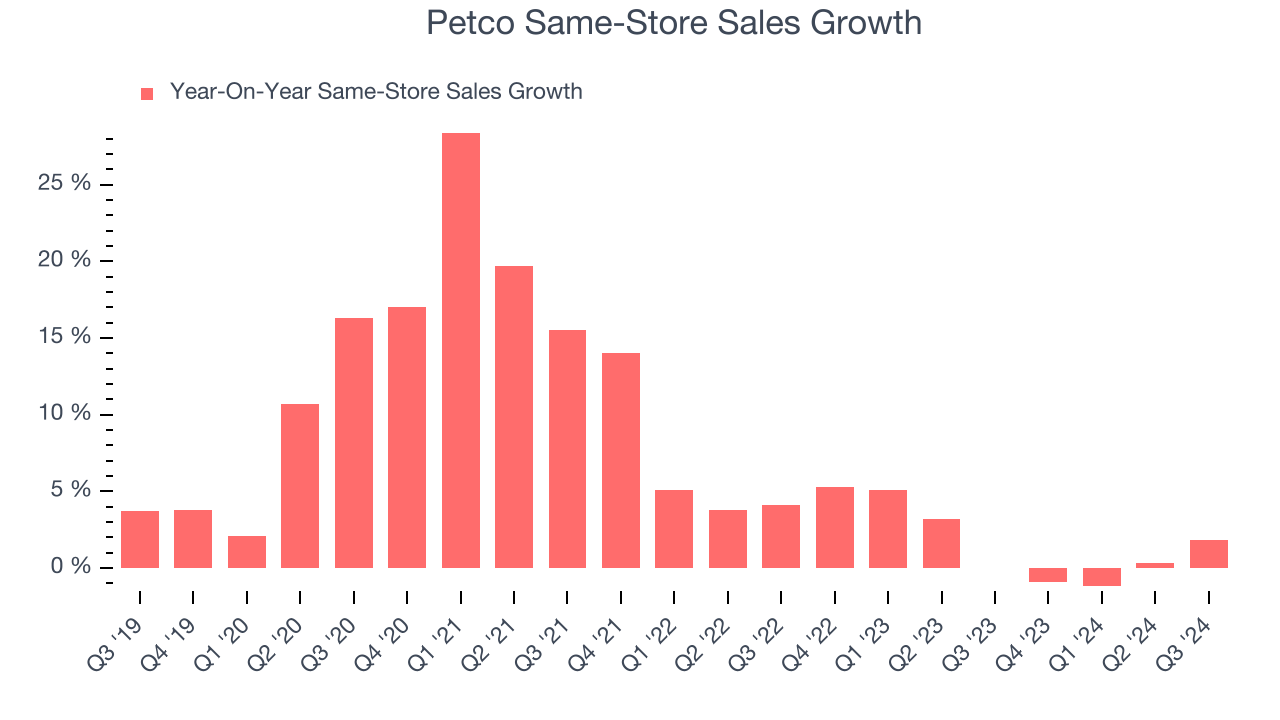

- Same-Store Sales rose 1.8% year on year (0% in the same quarter last year)

- Market Capitalization: $1.39 billion

"Our third quarter results demonstrate the meaningful progress we're making to strengthen our retail fundamentals to drive sustainable, profitable growth," said Joel Anderson, Petco's Chief Executive Officer.

Company Overview

Historically known for its window displays of pets for sale or adoption, Petco (NASDAQ: WOOF) is a specialty retailer of pet food and supplies as well as a provider of services such as wellness checks and grooming.

Specialty Retail

Some retailers try to sell everything under the sun, while others—appropriately called Specialty Retailers—focus on selling a narrow category and aiming to be exceptional at it. Whether it’s eyeglasses, sporting goods, or beauty and cosmetics, these stores win with depth of product in their category as well as in-store expertise and guidance for shoppers who need it. E-commerce competition exists and waning retail foot traffic impacts these retailers, but the magnitude of the headwinds depends on what they sell and what extra value they provide in their stores.

Sales Growth

A company’s long-term sales performance signals its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

Petco is a mid-sized retailer, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale.

As you can see below, Petco’s sales grew at a tepid 6.8% compounded annual growth rate over the last five years (we compare to 2019 to normalize for COVID-19 impacts) as its store footprint remained unchanged and it barely increased sales at existing, established locations.

This quarter, Petco reported modest year-on-year revenue growth of 1.2% but beat Wall Street’s estimates by 0.7%. Company management is currently guiding for a 7.4% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to remain flat over the next 12 months, a deceleration versus the last five years. This projection doesn't excite us and indicates its products will see some demand headwinds.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

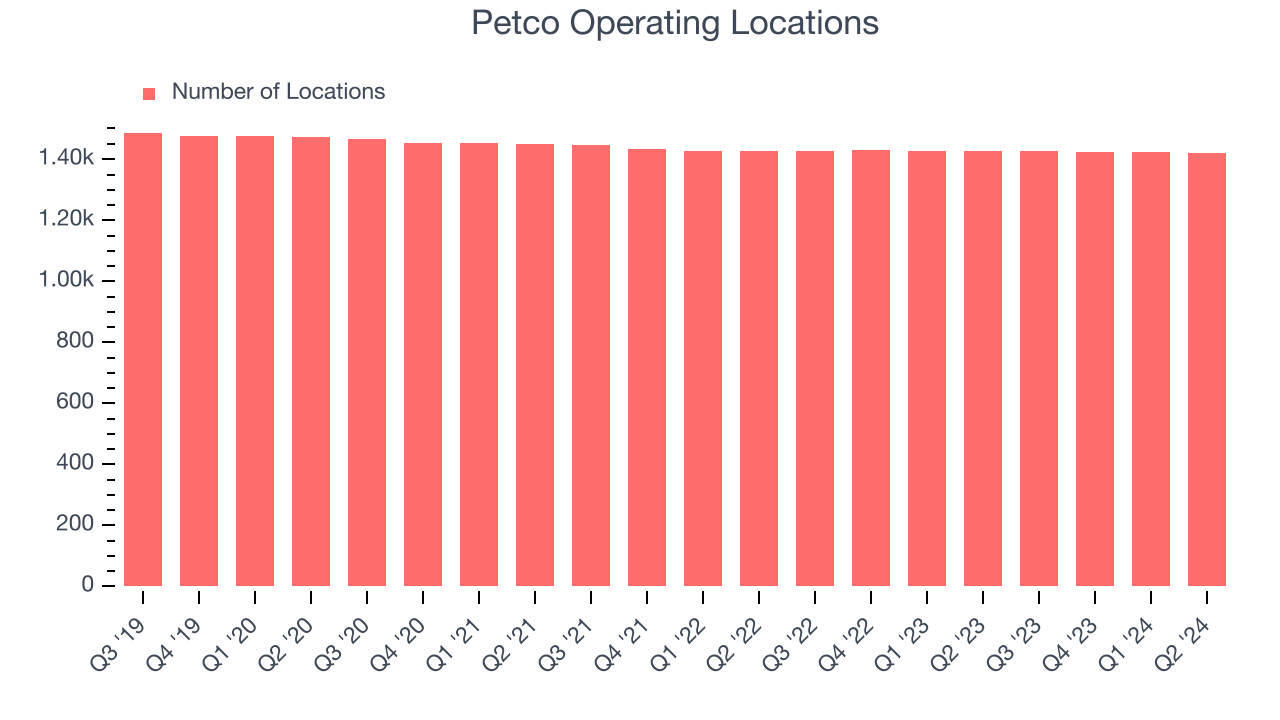

Store Performance

Number of Stores

A retailer’s store count influences how much it can sell and how quickly revenue can grow.

Over the last two years, Petco has kept its store count flat while other consumer retail businesses have opted for growth.

When a retailer keeps its store footprint steady, it usually means demand is stable and it’s focusing on operational efficiency to increase profitability.

Note that Petco reports its store count intermittently, so some data points are missing in the chart below.

Same-Store Sales

The change in a company's store base only tells one side of the story. The other is the performance of its existing locations and e-commerce sales, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales gives us insight into this topic because it measures organic growth for a retailer's e-commerce platform and brick-and-mortar shops that have existed for at least a year.

Petco’s demand within its existing locations has been relatively stable over the last two years but was below most retailers. On average, the company’s same-store sales have grown by 1.7% per year. Given its flat store base over the same period, this performance stems from a mixture of increased foot traffic at existing locations and higher e-commerce sales as demand shifts from in-store to online.

In the latest quarter, Petco’s same-store sales rose 1.8% year on year. This performance was more or less in line with its historical levels.

Key Takeaways from Petco’s Q3 Results

This was a two-sided quarter as its revenue, EPS, and EBITDA beat analysts' estimates while its full-year outlook for all metrics missed. Zooming out, we think this was a decent quarter featuring some areas of strength but also some blemishes. The market seemed to weigh the current results more than the guidance, and stock traded up 14.7% to $5.62 immediately following the results.

Is Petco an attractive investment opportunity at the current price? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.