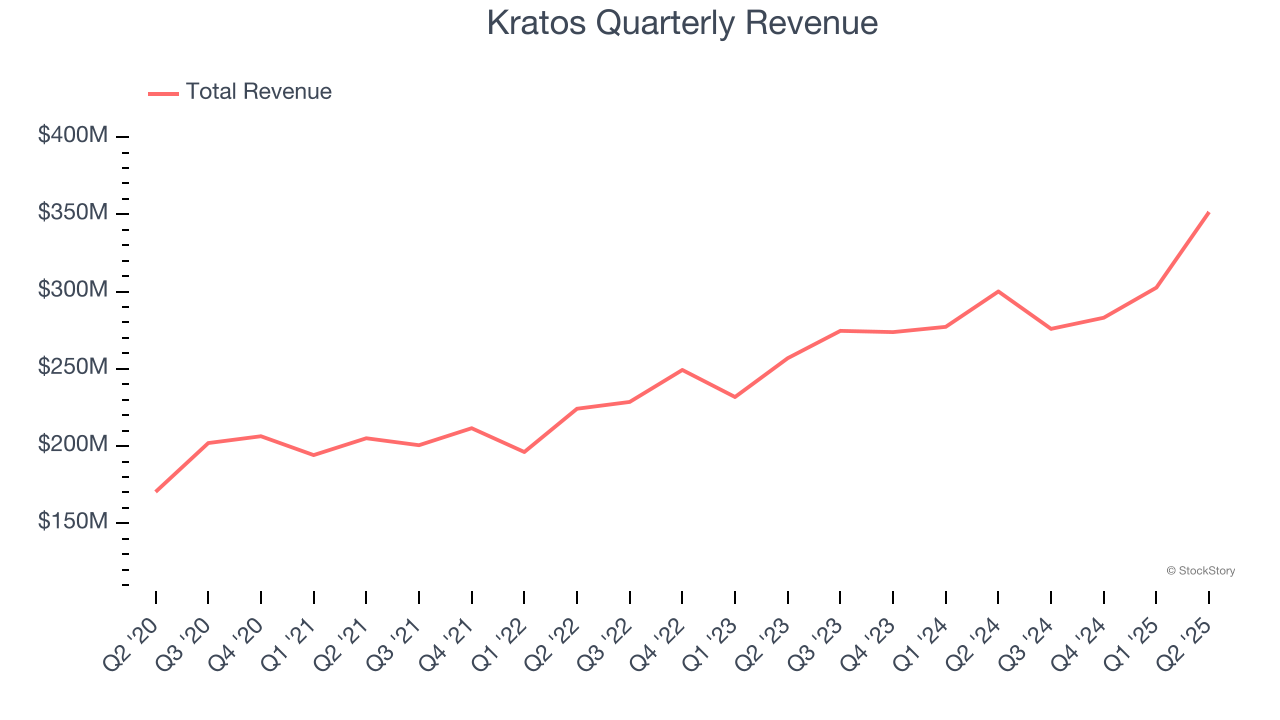

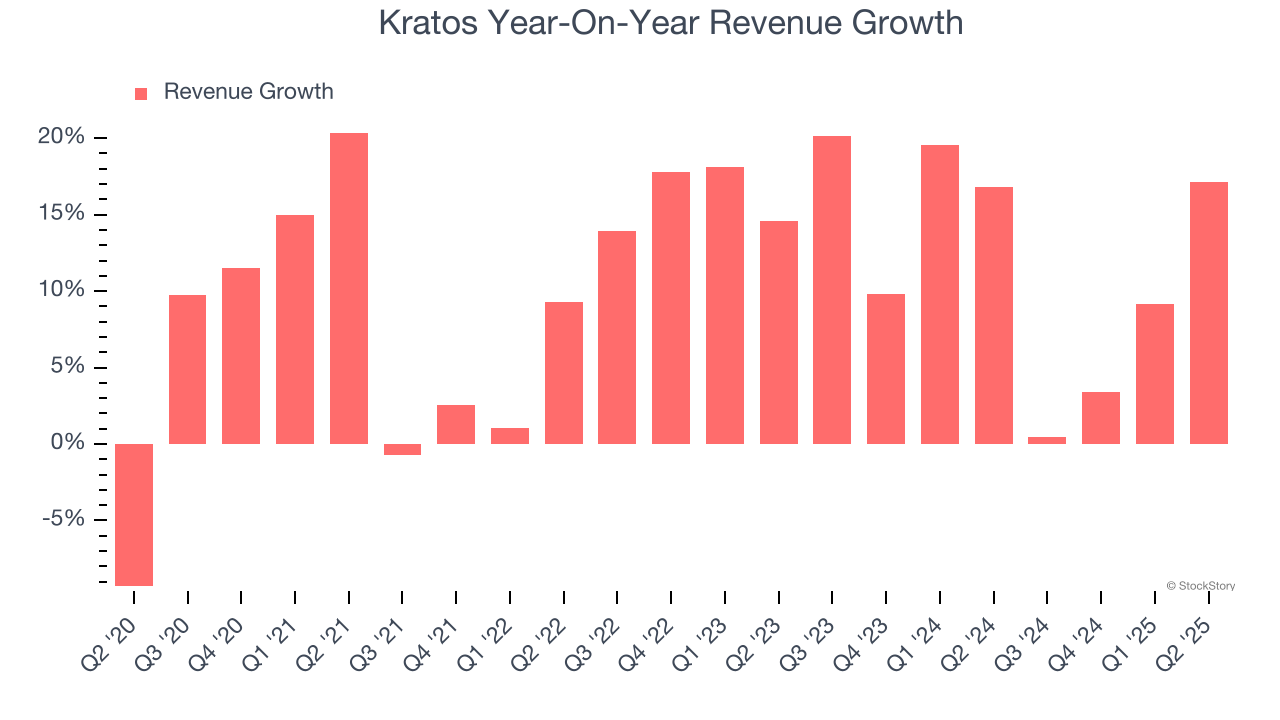

Aerospace and defense company Kratos (NASDAQ: KTOS) reported Q2 CY2025 results exceeding the market’s revenue expectations, with sales up 17.1% year on year to $351.5 million. Revenue guidance for the full year exceeded analysts’ estimates, but next quarter’s guidance of $320 million was less impressive, coming in 1.5% below expectations. Its non-GAAP profit of $0.11 per share was 17.7% above analysts’ consensus estimates.

Is now the time to buy Kratos? Find out by accessing our full research report, it’s free.

Kratos (KTOS) Q2 CY2025 Highlights:

- Revenue: $351.5 million vs analyst estimates of $305.5 million (17.1% year-on-year growth, 15% beat)

- Adjusted EPS: $0.11 vs analyst estimates of $0.09 (17.7% beat)

- Adjusted EBITDA: $28.3 million vs analyst estimates of $23.7 million (8.1% margin, 19.4% beat)

- The company lifted its revenue guidance for the full year to $1.3 billion at the midpoint from $1.27 billion, a 2.2% increase

- EBITDA guidance for the full year is $117 million at the midpoint, in line with analyst expectations

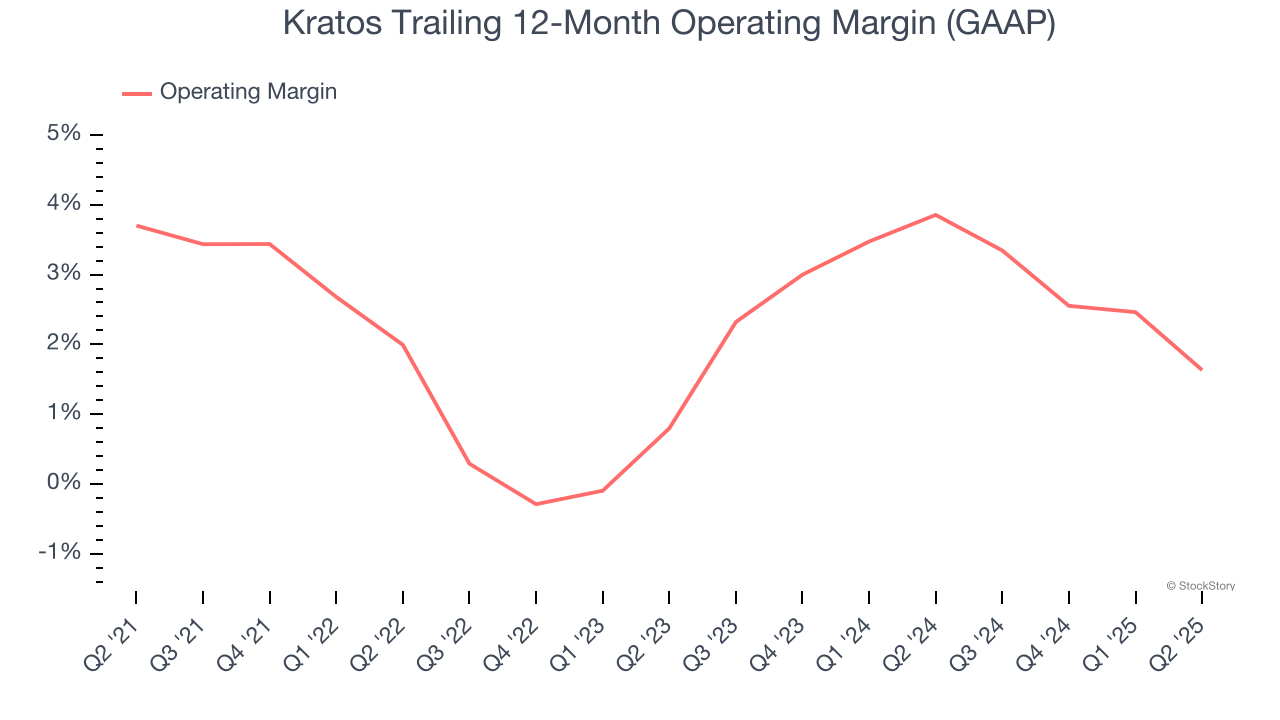

- Operating Margin: 1.1%, down from 4.2% in the same quarter last year

- Free Cash Flow was -$32.2 million compared to -$15.4 million in the same quarter last year

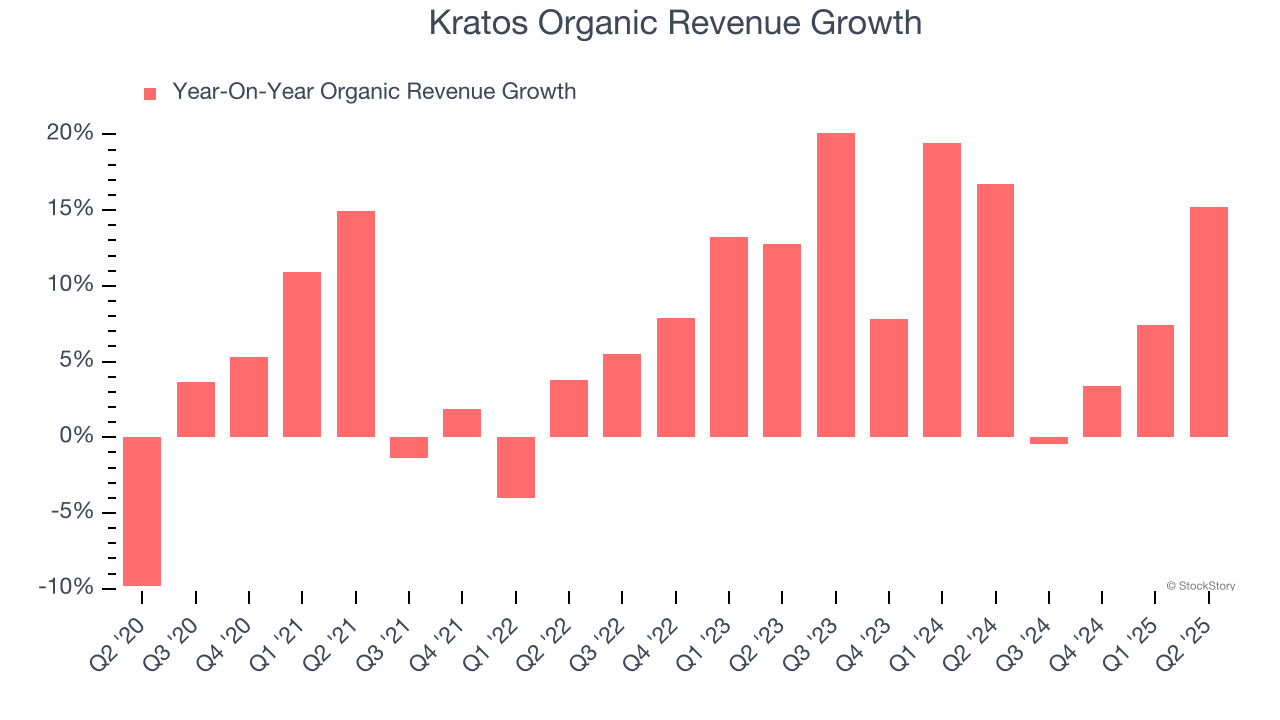

- Organic Revenue rose 15.2% year on year (16.7% in the same quarter last year)

- Market Capitalization: $9.92 billion

Eric DeMarco, Kratos’ President and CEO, said, “A generational recapitalization of strategic weapon systems is underway, with significant global funding being committed by the U.S. and its allies, including as represented by a planned U.S. 2026 National Security spend exceeding $1 trillion, NATO committing 5% of member GDP to defense, and Asian allies looking to do the same. The Global Defense and National Security Market is currently approximately $2.5 trillion, led by the United States “peace through strength” posture and is expected to grow for the foreseeable future.

Company Overview

Established with a commitment to supporting national security, Kratos (NASDAQ: KTOS) is a provider of advanced engineering, technology, and security solutions tailored for critical national security applications.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Luckily, Kratos’s sales grew at an impressive 11.4% compounded annual growth rate over the last five years. Its growth beat the average industrials company and shows its offerings resonate with customers.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Kratos’s annualized revenue growth of 12% over the last two years aligns with its five-year trend, suggesting its demand was predictably strong.

We can better understand the company’s sales dynamics by analyzing its organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, Kratos’s organic revenue averaged 11.2% year-on-year growth. Because this number aligns with its two-year revenue growth, we can see the company’s core operations (not acquisitions and divestitures) drove most of its results.

This quarter, Kratos reported year-on-year revenue growth of 17.1%, and its $351.5 million of revenue exceeded Wall Street’s estimates by 15%. Company management is currently guiding for a 16% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 12.4% over the next 12 months, similar to its two-year rate. This projection is noteworthy and indicates the market is forecasting success for its products and services.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Kratos was profitable over the last five years but held back by its large cost base. Its average operating margin of 2.4% was weak for an industrials business.

Analyzing the trend in its profitability, Kratos’s operating margin decreased by 2.1 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Kratos’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

In Q2, Kratos generated an operating margin profit margin of 1.1%, down 3.1 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

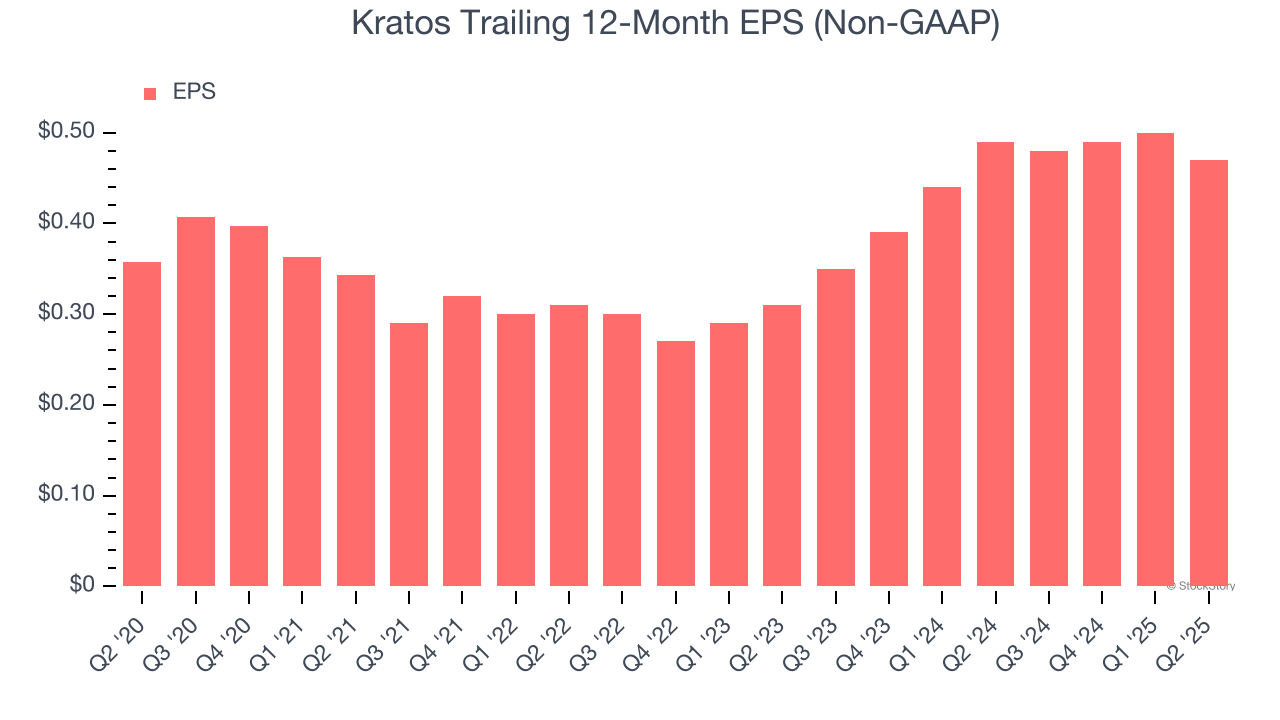

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

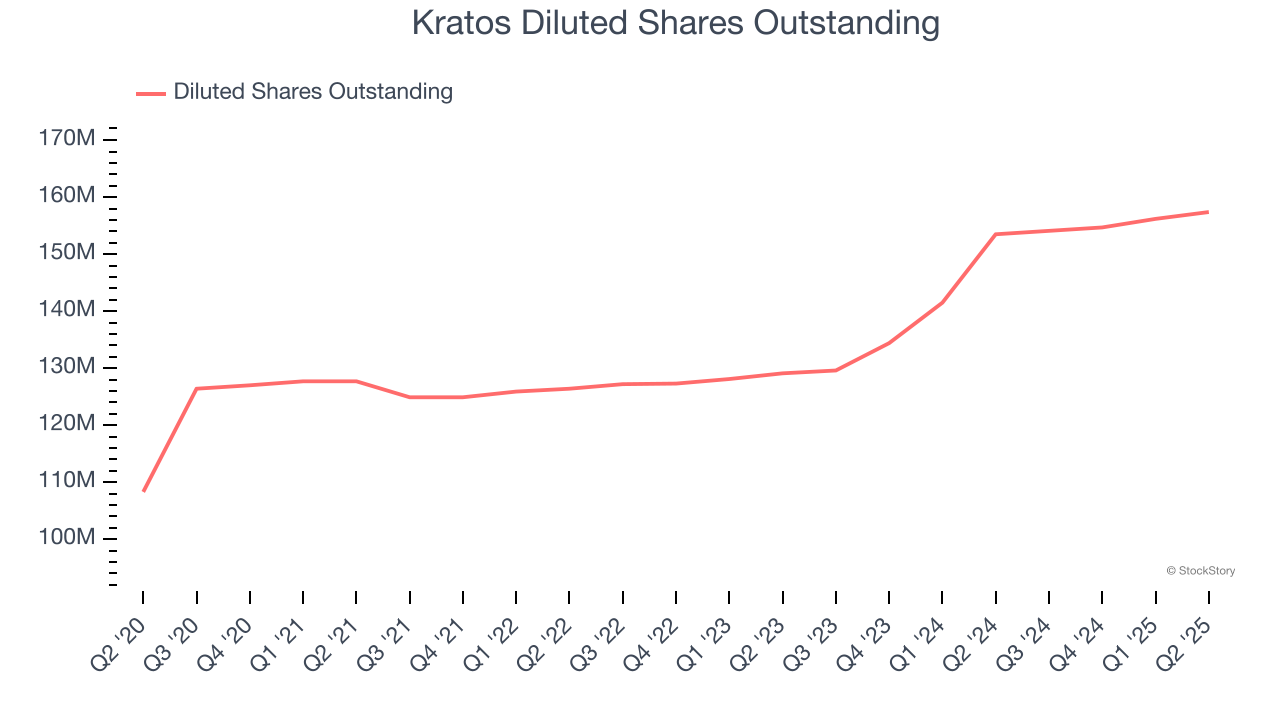

Kratos’s EPS grew at an unimpressive 5.7% compounded annual growth rate over the last five years, lower than its 11.4% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

Diving into the nuances of Kratos’s earnings can give us a better understanding of its performance. As we mentioned earlier, Kratos’s operating margin declined by 2.1 percentage points over the last five years. Its share count also grew by 45.3%, meaning the company not only became less efficient with its operating expenses but also diluted its shareholders.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Kratos, its two-year annual EPS growth of 23.1% was higher than its five-year trend. This acceleration made it one of the faster-growing industrials companies in recent history.

In Q2, Kratos reported adjusted EPS at $0.11, down from $0.14 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Kratos’s full-year EPS of $0.47 to grow 24.3%.

Key Takeaways from Kratos’s Q2 Results

We were impressed by how significantly Kratos blew past analysts’ expectations across the board this quarter. We were also excited it raised its full-year revenue guidance. Overall, we think this was a solid quarter with some key metrics above expectations. Investors were likely hoping for more, and shares traded down 4.2% to $56.67 immediately after reporting.

Is Kratos an attractive investment opportunity right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.