GE Vernova’s 28.4% return over the past six months has outpaced the S&P 500 by 22.5%, and its stock price has climbed to $802.45 per share. This was partly due to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is now the time to buy GE Vernova, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Is GE Vernova Not Exciting?

Despite the momentum, we're cautious about GE Vernova. Here are three reasons why GEV doesn't excite us and a stock we'd rather own.

1. Long-Term Revenue Growth Disappoints

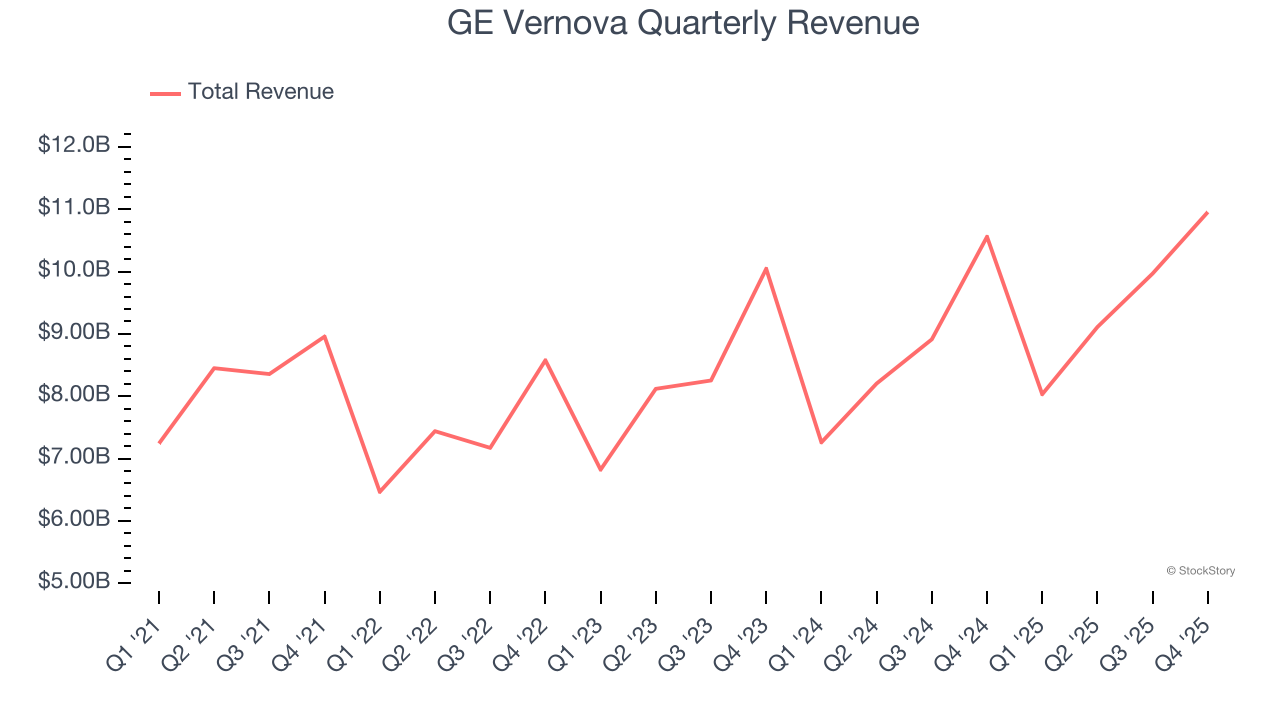

A company’s long-term performance is an indicator of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Over the last four years, GE Vernova grew its sales at a sluggish 3.6% compounded annual growth rate. This fell short of our benchmark for the industrials sector.

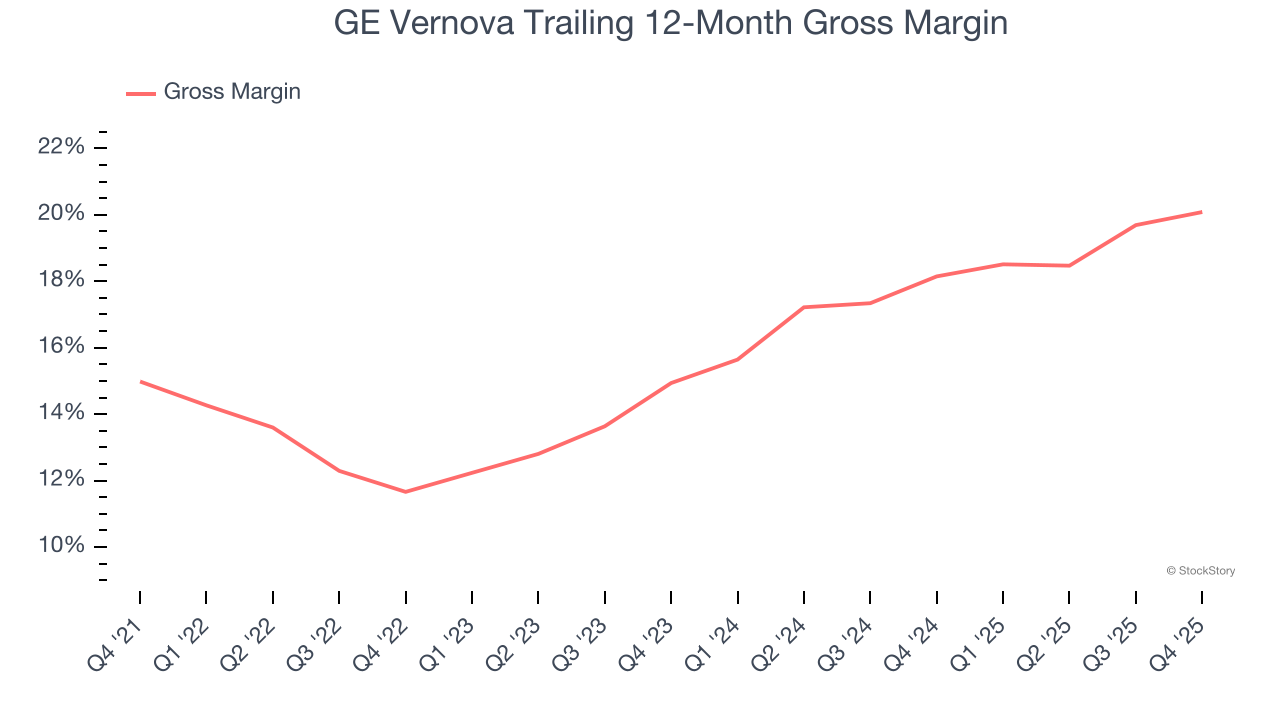

2. Low Gross Margin Reveals Weak Structural Profitability

Cost of sales for an industrials business is usually comprised of the direct labor, raw materials, and supplies needed to offer a product or service. These costs can be impacted by inflation and supply chain dynamics.

GE Vernova has bad unit economics for an industrials business, signaling it operates in a competitive market. As you can see below, it averaged a 16.2% gross margin over the last five years. That means GE Vernova paid its suppliers a lot of money ($83.81 for every $100 in revenue) to run its business.

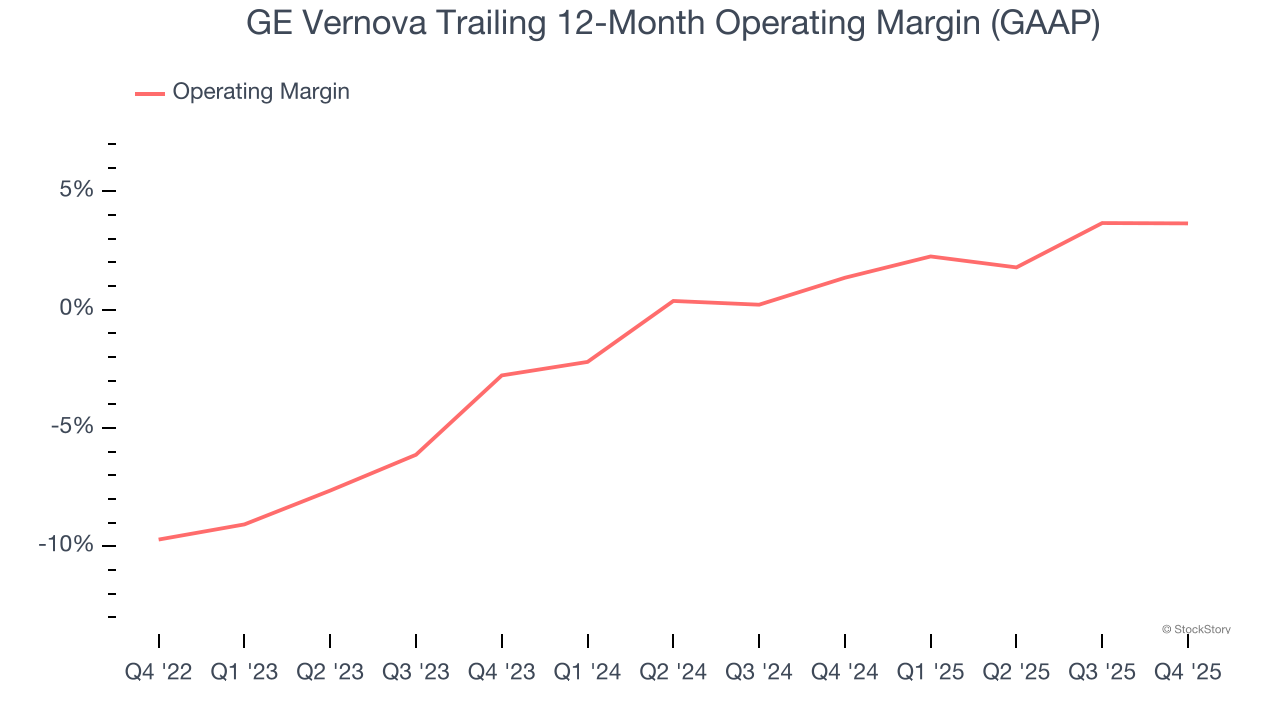

3. Operating Losses Sound the Alarms

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Although GE Vernova was profitable this quarter from an operational perspective, it’s generally struggled over a longer time period. Its expensive cost structure has contributed to an average operating margin of negative 1.4% over the last four years. Unprofitable industrials companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

Final Judgment

GE Vernova isn’t a terrible business, but it doesn’t pass our bar. With its shares outperforming the market lately, the stock trades at 58.2× forward P/E (or $802.45 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think there are better stocks to buy right now. We’d recommend looking at a fast-growing restaurant franchise with an A+ ranch dressing sauce.

Stocks We Like More Than GE Vernova

If your portfolio success hinges on just 4 stocks, your wealth is built on fragile ground. You have a small window to secure high-quality assets before the market widens and these prices disappear.

Don’t wait for the next volatility shock. Check out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.