Frontdoor has been treading water for the past six months, recording a small loss of 4.8% while holding steady at $56.64. The stock also fell short of the S&P 500’s 6% gain during that period.

Is now the time to buy Frontdoor, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Do We Think Frontdoor Will Underperform?

We're cautious about Frontdoor. Here are three reasons you should be careful with FTDR and a stock we'd rather own.

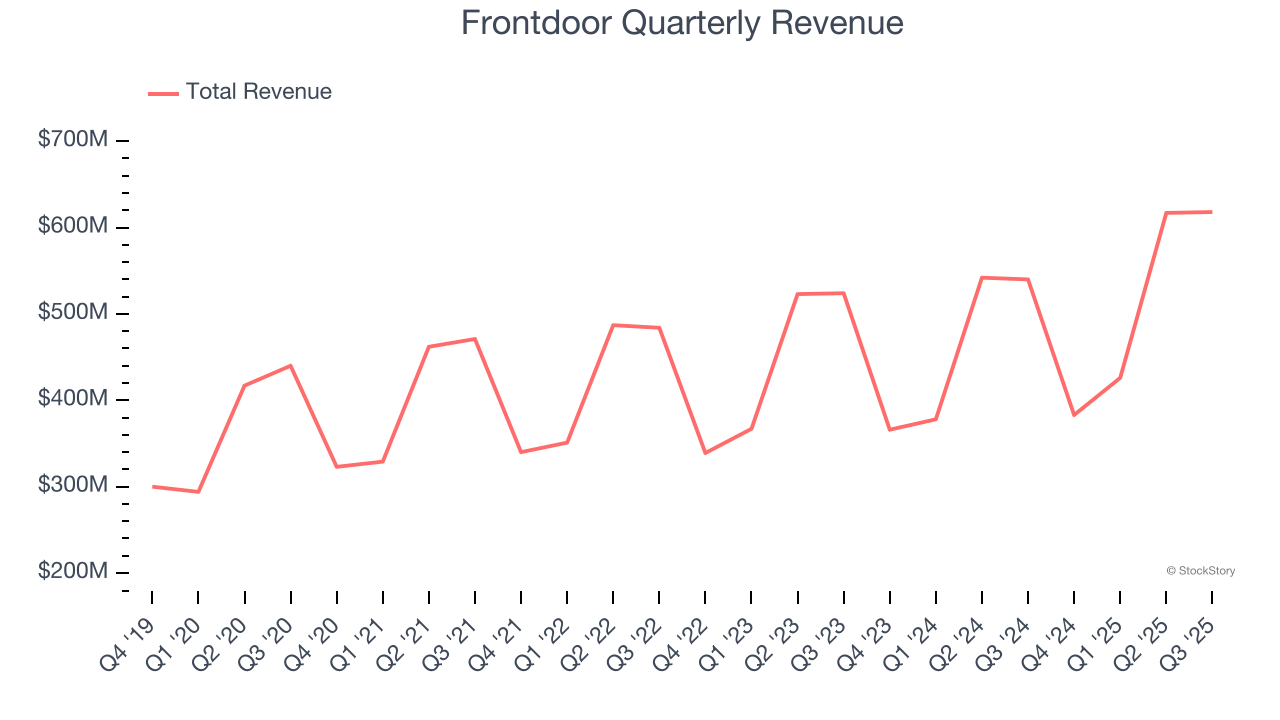

1. Long-Term Revenue Growth Disappoints

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Regrettably, Frontdoor’s sales grew at a weak 7.1% compounded annual growth rate over the last five years. This fell short of our benchmark for the consumer discretionary sector.

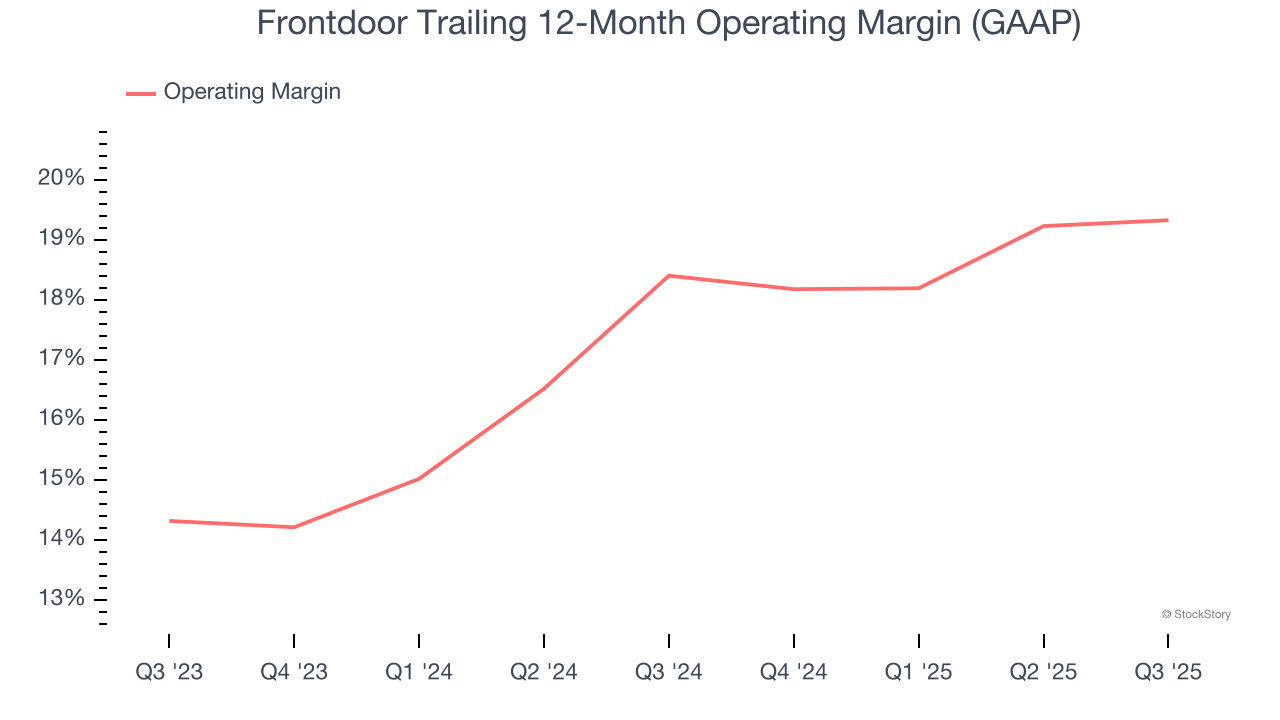

2. Weak Operating Margin Could Cause Trouble

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Frontdoor’s operating margin might fluctuated slightly over the last 12 months but has remained more or less the same, averaging 18.9% over the last two years. This profitability was inadequate for a consumer discretionary business and caused by its suboptimal cost structure.

3. Free Cash Flow Projections Disappoint

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Over the next year, analysts’ consensus estimates show they’re expecting Frontdoor’s free cash flow margin of 16.9% for the last 12 months to remain the same.

Final Judgment

Frontdoor falls short of our quality standards. With its shares lagging the market recently, the stock trades at 13.1× forward P/E (or $56.64 per share). This valuation is reasonable, but the company’s shaky fundamentals present too much downside risk. There are better stocks to buy right now. We’d recommend looking at a safe-and-steady industrials business benefiting from an upgrade cycle.

Stocks We Like More Than Frontdoor

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.