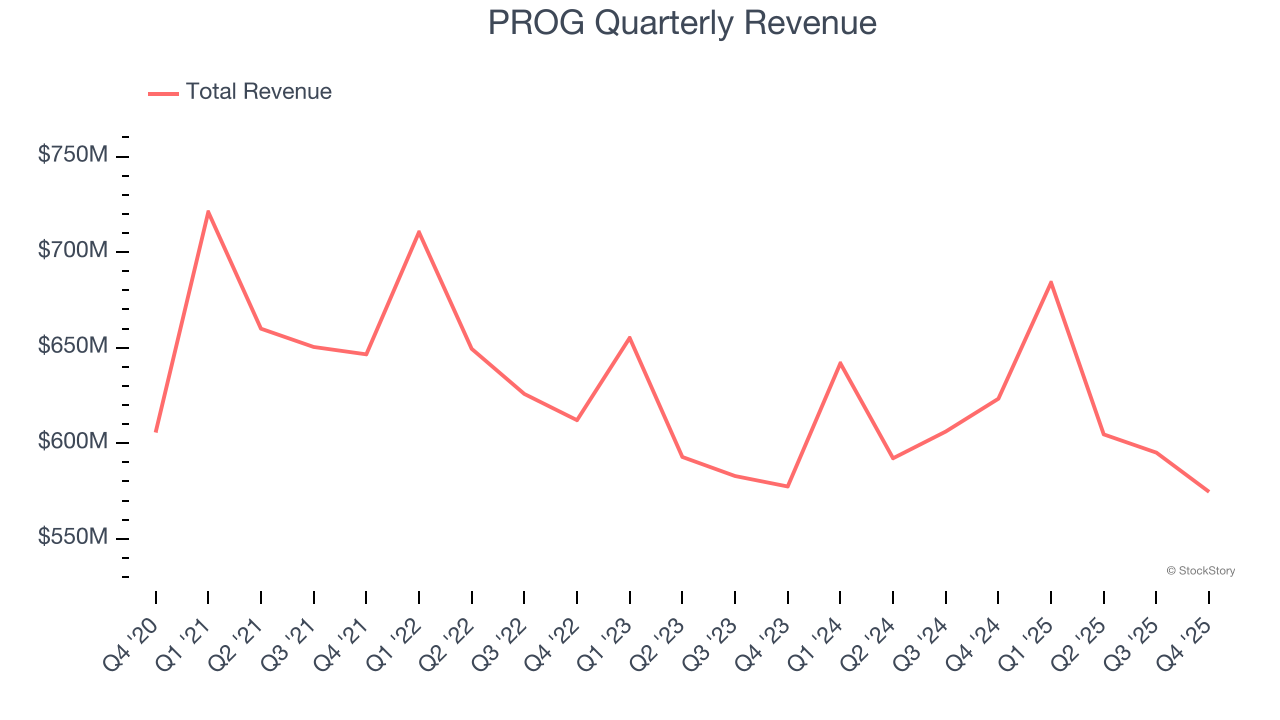

Financial technology company PROG Holdings (NYSE: PRG) fell short of the market’s revenue expectations in Q4 CY2025, with sales falling 7.8% year on year to $574.6 million. On the other hand, the company’s full-year revenue guidance of $3.08 billion at the midpoint came in 8% above analysts’ estimates. Its non-GAAP profit of $0.90 per share was 48.8% above analysts’ consensus estimates.

Is now the time to buy PROG? Find out by accessing our full research report, it’s free.

PROG (PRG) Q4 CY2025 Highlights:

- Revenue: $574.6 million vs analyst estimates of $584.3 million (7.8% year-on-year decline, 1.7% miss)

- Pre-tax Profit: $31.41 million (5.5% margin)

- Adjusted EPS: $0.90 vs analyst estimates of $0.61 (48.8% beat)

- Adjusted EPS guidance for the upcoming financial year 2026 is $4.23 at the midpoint, beating analyst estimates by 17.5%

- Market Capitalization: $1.34 billion

“Q4 and full-year 2025 were periods of disciplined execution that demonstrated the strength and resilience of PROG’s multi-product platform,” said PROG Holdings President and CEO Steve Michaels.

Company Overview

Evolving from its origins as Aaron's, Inc. before rebranding in 2020, PROG Holdings (NYSE: PRG) provides alternative payment solutions including lease-to-own options and second-look credit products for consumers who may not qualify for traditional financing.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Unfortunately, PROG struggled to consistently increase demand as its $2.46 billion of revenue for the trailing 12 months was close to its revenue five years ago. This wasn’t a great result and suggests it’s a low quality business.

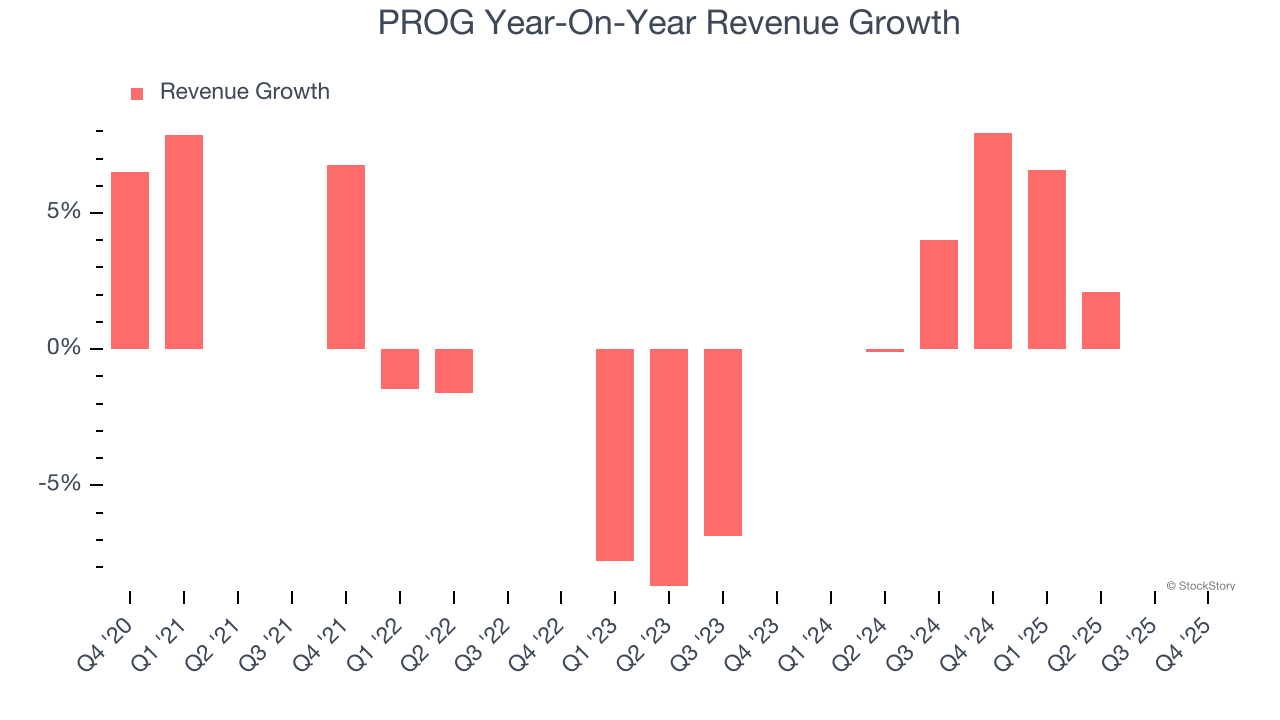

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. PROG’s annualized revenue growth of 1% over the last two years is above its five-year trend, which is encouraging.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, PROG missed Wall Street’s estimates and reported a rather uninspiring 7.8% year-on-year revenue decline, generating $574.6 million of revenue.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Key Takeaways from PROG’s Q4 Results

It was good to see PROG beat analysts’ EPS expectations this quarter. We were also glad its full-year EPS guidance trumped Wall Street’s estimates. On the other hand, its revenue missed. Zooming out, we think this was a solid print. The stock traded up 3.9% to $35.20 immediately following the results.

PROG had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).