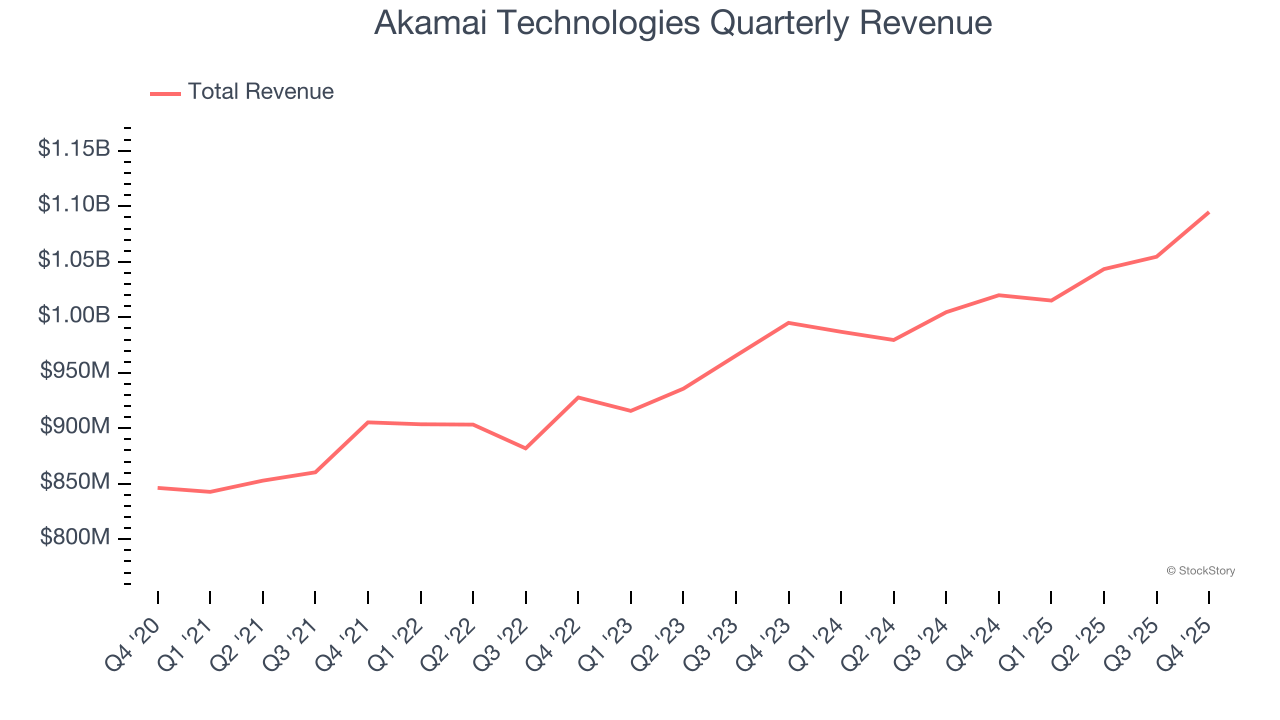

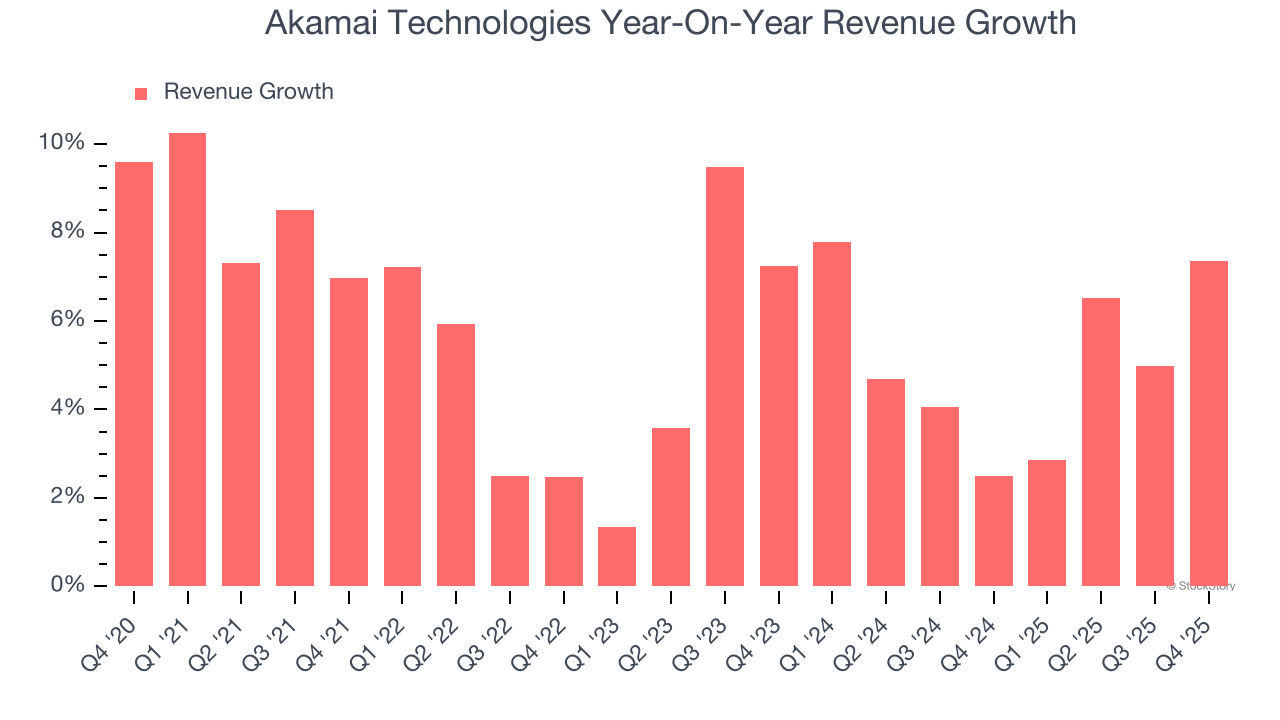

Cloud technology company Akamai Technologies (NASDAQ: AKAM) reported Q4 CY2025 results topping the market’s revenue expectations, with sales up 7.4% year on year to $1.09 billion. The company expects next quarter’s revenue to be around $1.07 billion, close to analysts’ estimates. Its non-GAAP profit of $1.84 per share was 5.1% above analysts’ consensus estimates.

Is now the time to buy Akamai Technologies? Find out by accessing our full research report, it’s free.

Akamai Technologies (AKAM) Q4 CY2025 Highlights:

- Revenue: $1.09 billion vs analyst estimates of $1.08 billion (7.4% year-on-year growth, 1.6% beat)

- Adjusted EPS: $1.84 vs analyst estimates of $1.75 (5.1% beat)

- Adjusted Operating Income: $316 million vs analyst estimates of $311.4 million (28.9% margin, 1.5% beat)

- Revenue Guidance for Q1 CY2026 is $1.07 billion at the midpoint, roughly in line with what analysts were expecting

- Adjusted EPS guidance for the upcoming financial year 2026 is $6.70 at the midpoint, missing analyst estimates by 8.7%

- Operating Margin: 8.7%, down from 14.5% in the same quarter last year

- Free Cash Flow Margin: 14.8%, down from 23.4% in the previous quarter

- Market Capitalization: $15.73 billion

“Akamai delivered strong year-end performance, with better-than-expected results on the top and bottom lines. We were particularly pleased to achieve 36% year-over-year revenue growth in Q4 across our Guardicore Segmentation and API Security products, and 45% year-over-year revenue growth for Cloud Infrastructure Services (CIS),” said Dr. Tom Leighton, Akamai’s Chief Executive Officer.

Company Overview

With a massive distributed network spanning 4,100+ points of presence in nearly 130 countries, Akamai Technologies (NASDAQ: AKAM) provides a global distributed cloud platform that helps businesses deliver, secure, and optimize their digital experiences online.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Akamai Technologies grew its sales at a weak 5.6% compounded annual growth rate. This fell short of our benchmark for the software sector and is a poor baseline for our analysis.

Long-term growth is the most important, but within software, a half-decade historical view may miss new innovations or demand cycles. Akamai Technologies’s annualized revenue growth of 5.1% over the last two years aligns with its five-year trend, suggesting its demand was consistently weak.

This quarter, Akamai Technologies reported year-on-year revenue growth of 7.4%, and its $1.09 billion of revenue exceeded Wall Street’s estimates by 1.6%. Company management is currently guiding for a 5.7% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 5% over the next 12 months, similar to its two-year rate. This projection is underwhelming and indicates its newer products and services will not accelerate its top-line performance yet.

Microsoft, Alphabet, Coca-Cola, Monster Beverage—all began as under-the-radar growth stories riding a massive trend. We’ve identified the next one: a profitable AI semiconductor play Wall Street is still overlooking. Go here for access to our full report.

Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

Akamai Technologies’s recent customer acquisition efforts haven’t yielded returns as its CAC payback period was negative this quarter, meaning its incremental sales and marketing investments outpaced its revenue. The company’s inefficiency indicates it operates in a highly competitive environment where there is little differentiation between Akamai Technologies’s products and its peers.

Key Takeaways from Akamai Technologies’s Q4 Results

It was great to see Akamai Technologies expecting revenue growth to accelerate next year. We were also glad its full-year revenue guidance slightly exceeded Wall Street’s estimates. On the other hand, its full-year EPS guidance missed and its EPS guidance for next quarter fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 9% to $99.67 immediately following the results.

The latest quarter from Akamai Technologies’s wasn’t that good. One earnings report doesn’t define a company’s quality, though, so let’s explore whether the stock is a buy at the current price. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).