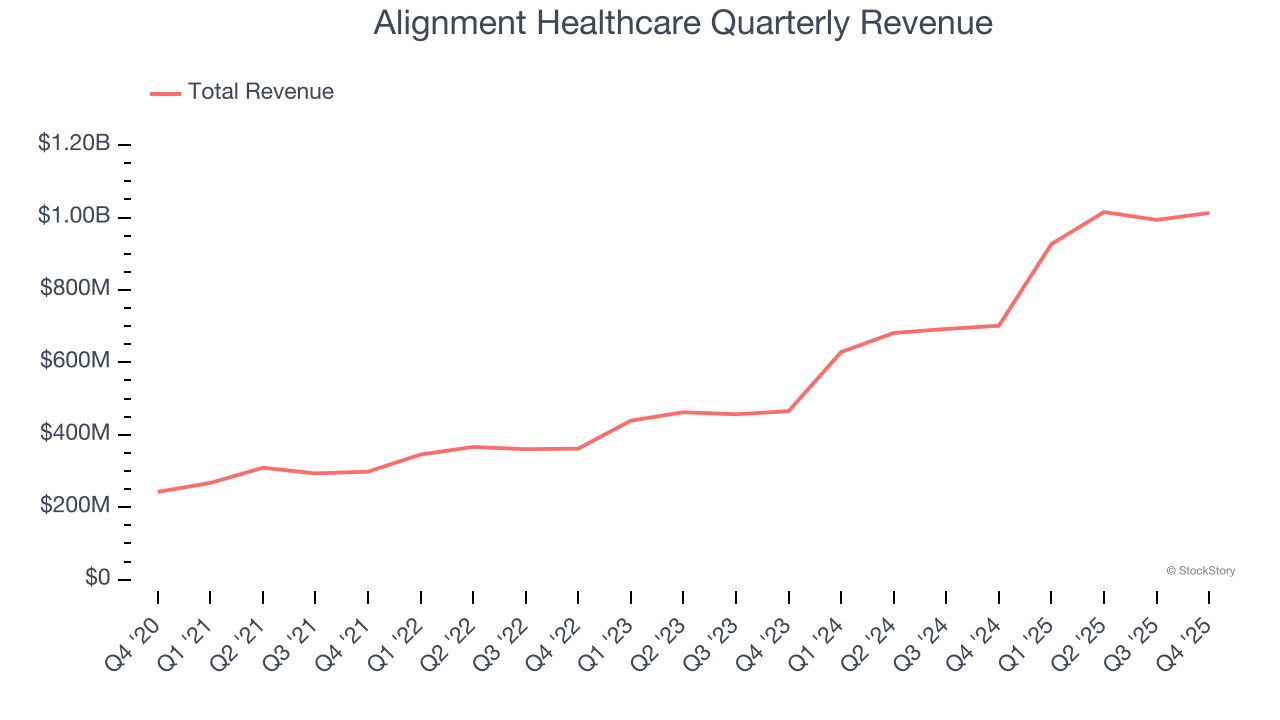

Health insurance company Alignment Healthcare (NASDAQ: ALHC) reported revenue ahead of Wall Street’s expectations in Q4 CY2025, with sales up 44.4% year on year to $1.01 billion. On the other hand, next quarter’s revenue guidance of $1.22 billion was less impressive, coming in 1.9% below analysts’ estimates. Its GAAP loss of $0.05 per share was 67.1% above analysts’ consensus estimates.

Is now the time to buy Alignment Healthcare? Find out by accessing our full research report, it’s free.

Alignment Healthcare (ALHC) Q4 CY2025 Highlights:

- Revenue: $1.01 billion vs analyst estimates of $1 billion (44.4% year-on-year growth, 1% beat)

- EPS (GAAP): -$0.05 vs analyst estimates of -$0.15 (67.1% beat)

- Adjusted EBITDA: $11.41 million (1.1% margin, 737% year-on-year growth)

- Revenue Guidance for Q1 CY2026 is $1.22 billion at the midpoint, below analyst estimates of $1.24 billion

- EBITDA guidance for the upcoming financial year 2026 is $148 million at the midpoint, in line with analyst expectations

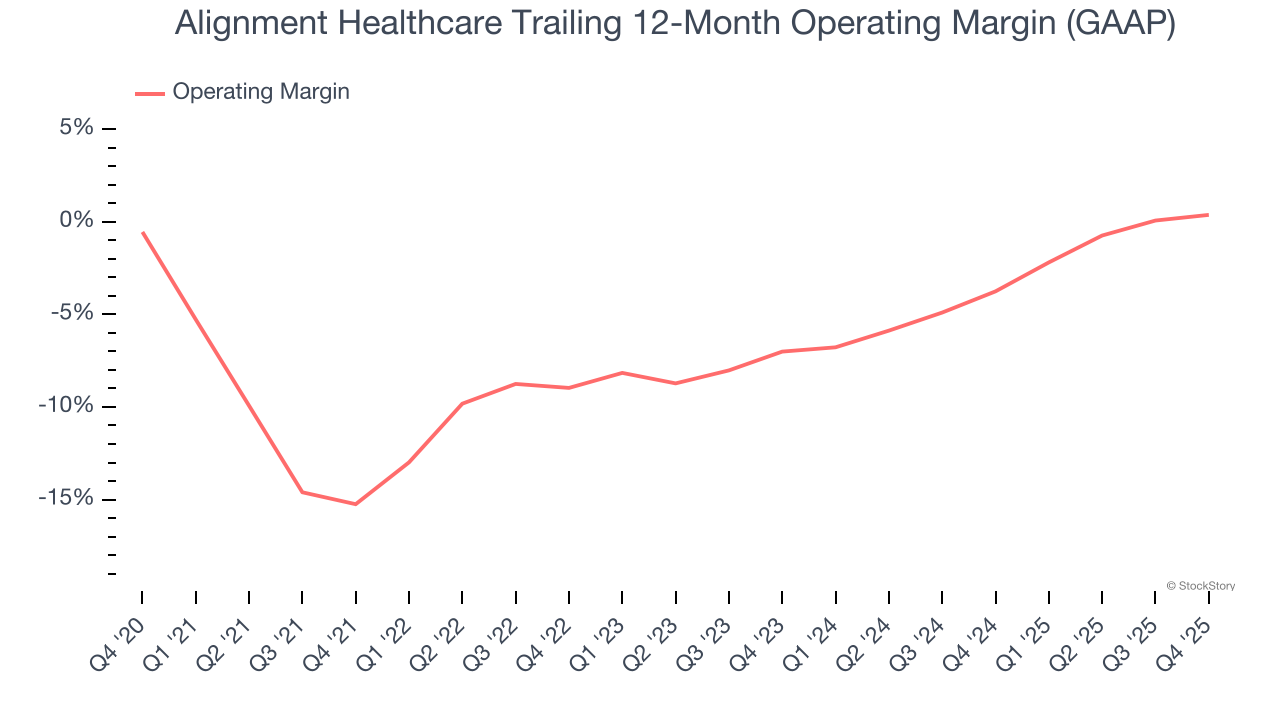

- Operating Margin: -1%, up from -3.2% in the same quarter last year

- Free Cash Flow was -$55.4 million compared to -$18 million in the same quarter last year

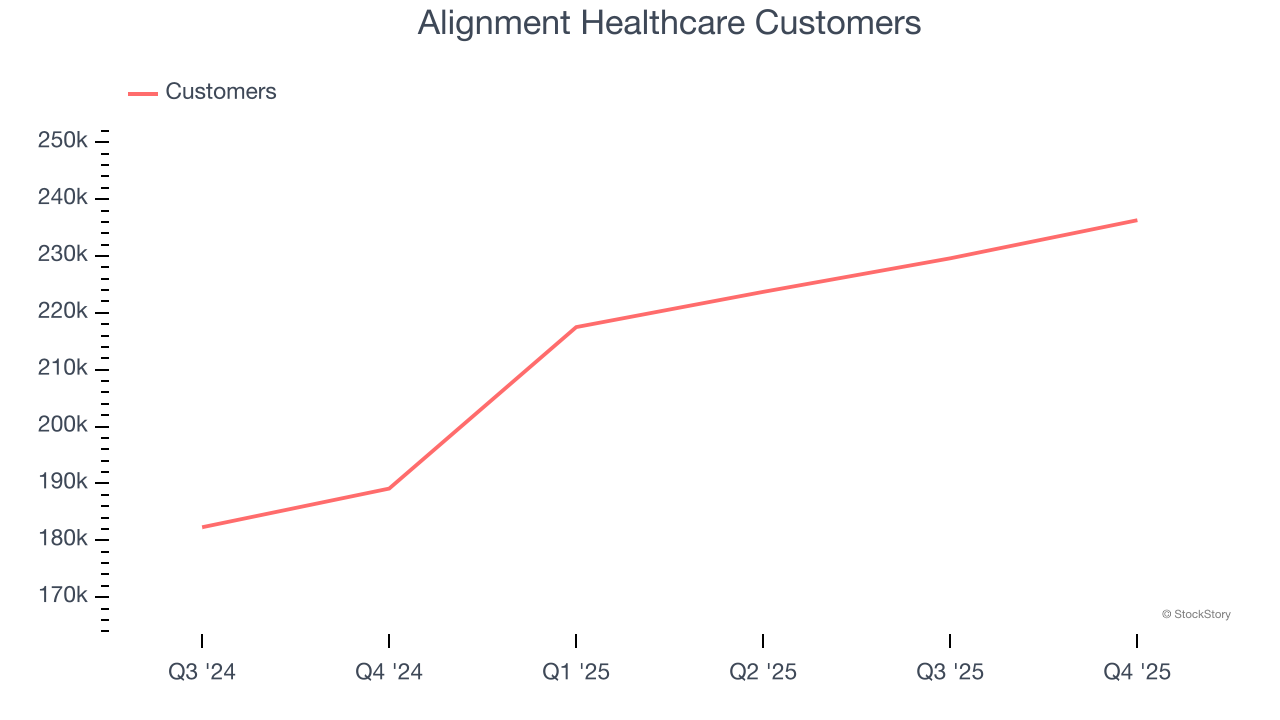

- Customers: 236,300, up from 229,600 in the previous quarter

- Market Capitalization: $4.03 billion

Company Overview

Founded in 2013 with a mission to transform healthcare for seniors, Alignment Healthcare (NASDAQ: ALHC) provides Medicare Advantage health plans for seniors with features like concierge services, transportation benefits, and technology-driven care coordination.

Revenue Growth

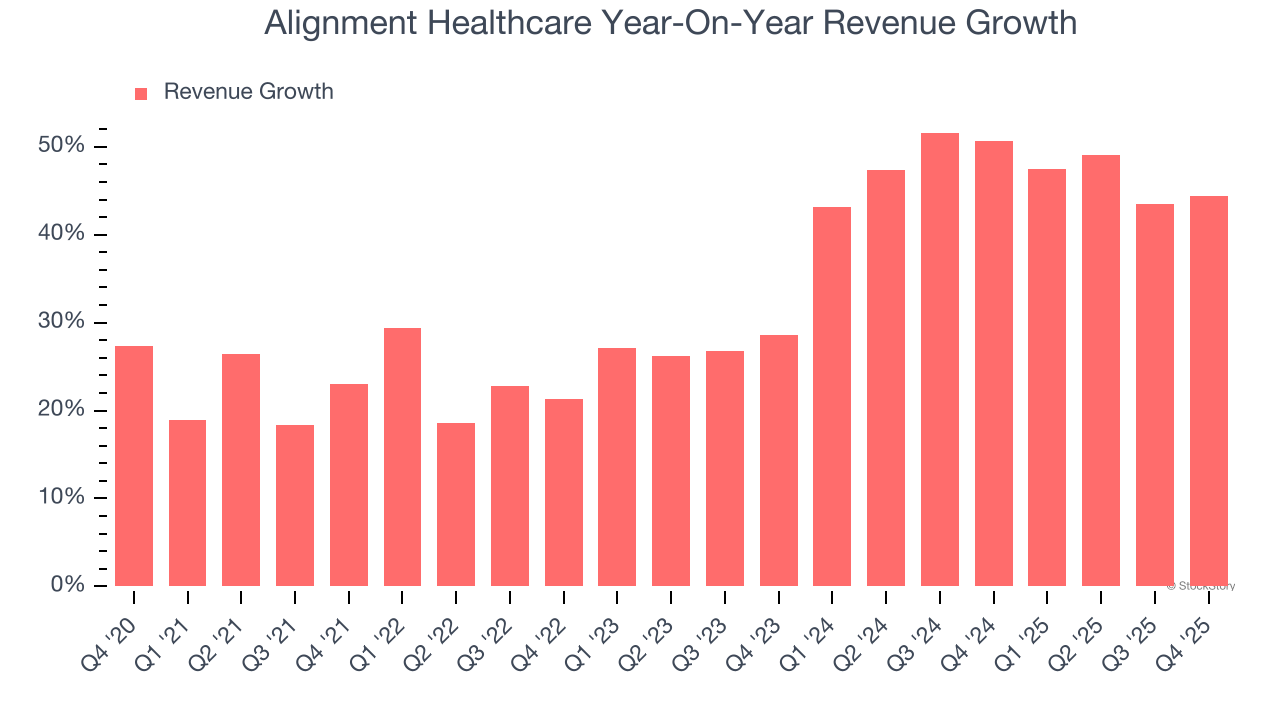

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Luckily, Alignment Healthcare’s sales grew at an incredible 32.7% compounded annual growth rate over the last five years. Its growth surpassed the average healthcare company and shows its offerings resonate with customers, a great starting point for our analysis.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Alignment Healthcare’s annualized revenue growth of 47.1% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

Alignment Healthcare also reports its number of customers, which reached 236,300 in the latest quarter. Over the last two years, Alignment Healthcare’s customer base averaged 25.5% year-on-year growth. Because this number is lower than its revenue growth, we can see the average customer spent more money each year on the company’s products and services.

This quarter, Alignment Healthcare reported magnificent year-on-year revenue growth of 44.4%, and its $1.01 billion of revenue beat Wall Street’s estimates by 1%. Company management is currently guiding for a 31.1% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 31.2% over the next 12 months, a deceleration versus the last two years. Still, this projection is admirable and implies the market is baking in success for its products and services.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Operating Margin

Alignment Healthcare’s high expenses have contributed to an average operating margin of negative 4.7% over the last five years. Unprofitable healthcare companies require extra attention because they could get caught swimming naked when the tide goes out.

On the plus side, Alignment Healthcare’s operating margin rose by 15.6 percentage points over the last five years, as its sales growth gave it operating leverage. Zooming in on its more recent performance, we can see the company’s trajectory is intact as its margin has also increased by 7.4 percentage points on a two-year basis. These data points are very encouraging and show momentum is on its side.

This quarter, Alignment Healthcare generated a negative 1% operating margin.

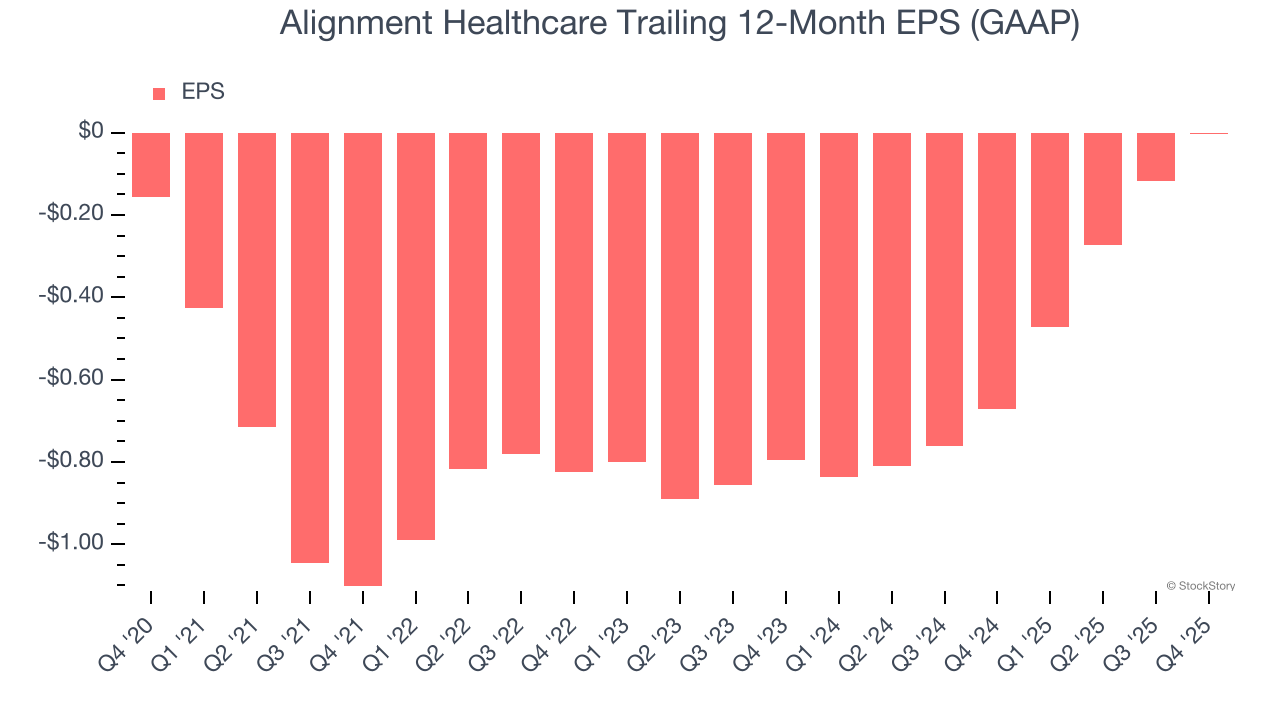

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Alignment Healthcare’s full-year EPS flipped from negative to breakeven over the last five years. This is a good sign and shows it’s at an inflection point.

In Q4, Alignment Healthcare reported EPS of negative $0.05, up from negative $0.16 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street is optimistic. Analysts forecast Alignment Healthcare’s full-year EPS of negative $0 will flip to positive $0.10.

Key Takeaways from Alignment Healthcare’s Q4 Results

It was good to see Alignment Healthcare beat analysts’ EPS expectations this quarter. We were also happy its revenue narrowly outperformed Wall Street’s estimates. On the other hand, its revenue guidance for next quarter missed and its EBITDA guidance for next quarter fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 4.5% to $19.50 immediately following the results.

Is Alignment Healthcare an attractive investment opportunity at the current price? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).