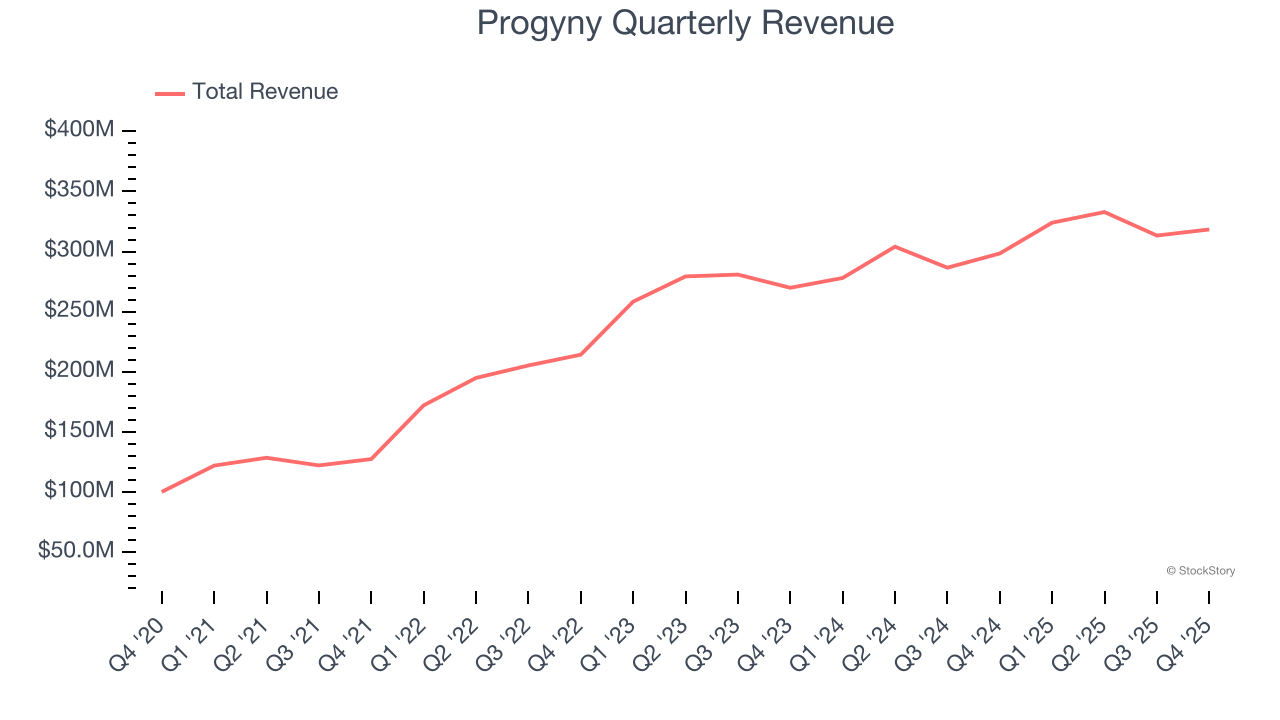

Fertility benefits company Progyny (NASDAQ: PGNY) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 6.7% year on year to $318.4 million. On the other hand, next quarter’s revenue guidance of $325.5 million was less impressive, coming in 5.1% below analysts’ estimates. Its non-GAAP profit of $0.48 per share was 19.9% above analysts’ consensus estimates.

Is now the time to buy Progyny? Find out by accessing our full research report, it’s free.

Progyny (PGNY) Q4 CY2025 Highlights:

- Revenue: $318.4 million vs analyst estimates of $308.4 million (6.7% year-on-year growth, 3.2% beat)

- Adjusted EPS: $0.48 vs analyst estimates of $0.40 (19.9% beat)

- Adjusted EBITDA: $51.39 million vs analyst estimates of $50.91 million (16.1% margin, 0.9% beat)

- Revenue Guidance for Q1 CY2026 is $325.5 million at the midpoint, below analyst estimates of $343 million

- Adjusted EPS guidance for the upcoming financial year 2026 is $1.89 at the midpoint, missing analyst estimates by 3.4%

- EBITDA guidance for the upcoming financial year 2026 is $231.5 million at the midpoint, below analyst estimates of $240.2 million

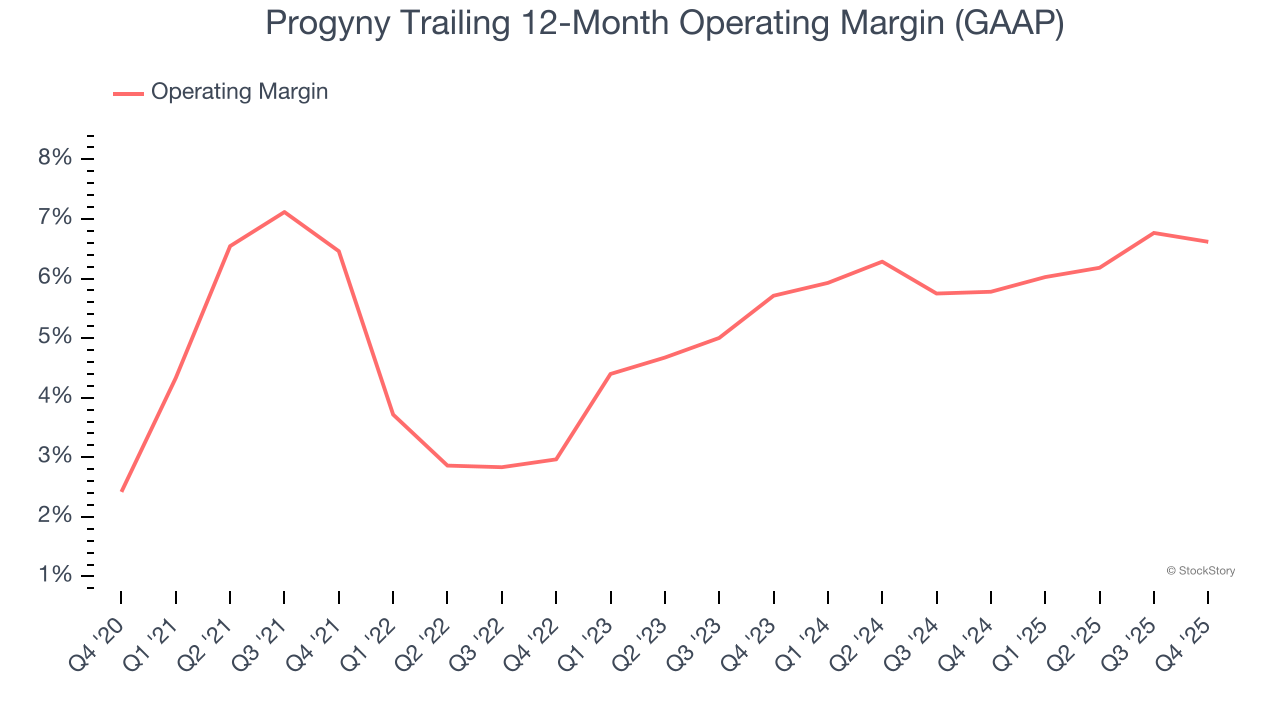

- Operating Margin: 4.8%, in line with the same quarter last year

- Free Cash Flow Margin: 15.3%, down from 16.8% in the same quarter last year

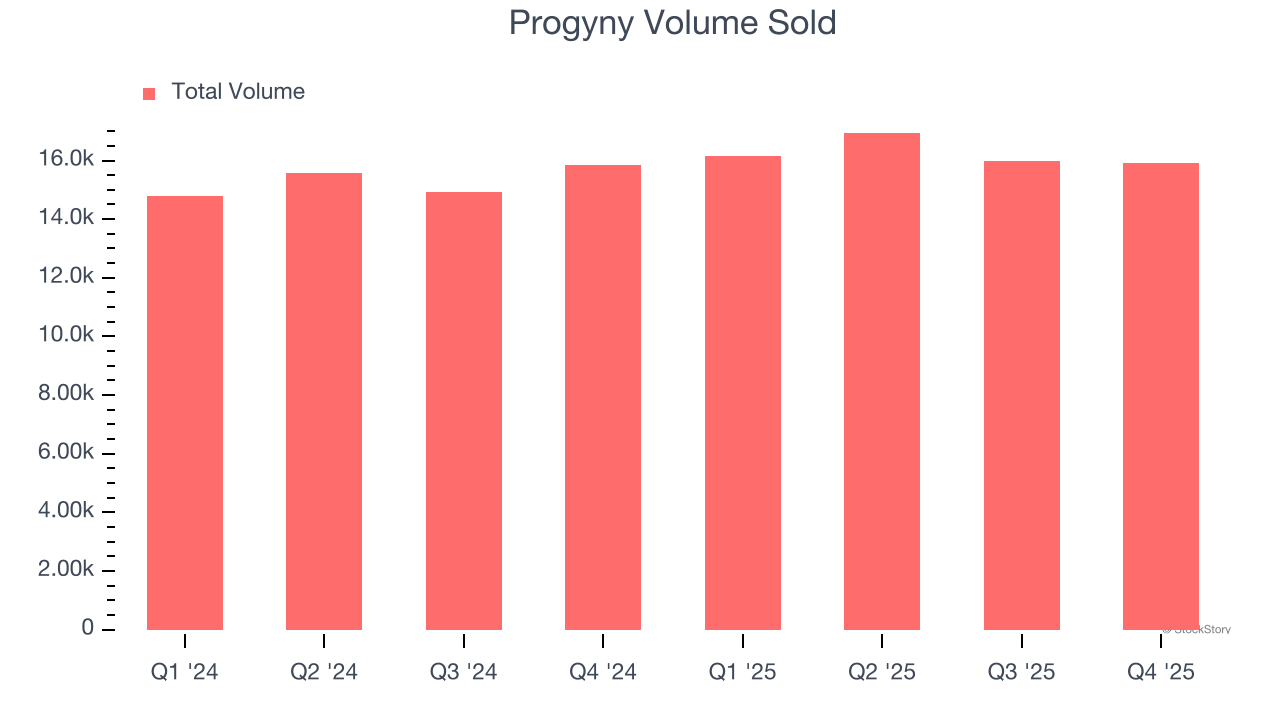

- Sales Volumes were flat year on year

- Market Capitalization: $1.84 billion

“We're pleased to report that 2025 ended strongly, concluding a record year for Progyny, one in which we achieved our highest ever levels of full year revenue, Adjusted EBITDA, and operating cash flow,” said Pete Anevski, Chief Executive Officer of Progyny.

Company Overview

Pioneering a data-driven approach to family building that has achieved an industry-leading patient satisfaction score of +80, Progyny (NASDAQ: PGNY) provides comprehensive fertility and family building benefits solutions to employers, helping employees access quality fertility treatments and support services.

Revenue Growth

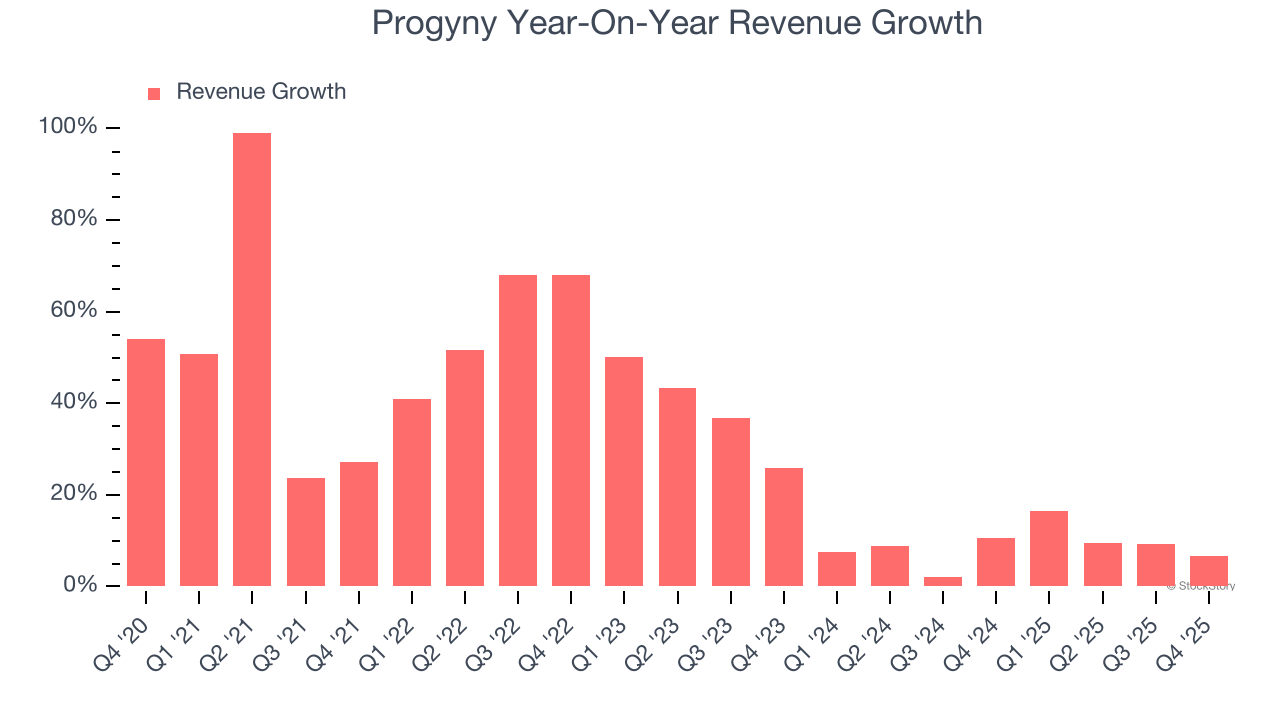

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Thankfully, Progyny’s 30.2% annualized revenue growth over the last five years was incredible. Its growth beat the average healthcare company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Progyny’s annualized revenue growth of 8.8% over the last two years is below its five-year trend, but we still think the results were respectable.

We can dig further into the company’s revenue dynamics by analyzing its number of units sold, which reached 15,927 in the latest quarter. Over the last two years, Progyny’s units sold averaged 6.4% year-on-year growth. Because this number is lower than its revenue growth, we can see the company benefited from price increases.

This quarter, Progyny reported year-on-year revenue growth of 6.7%, and its $318.4 million of revenue exceeded Wall Street’s estimates by 3.2%. Company management is currently guiding for flat sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 8.2% over the next 12 months, similar to its two-year rate. This projection is healthy and implies the market sees success for its products and services.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D.

Progyny’s operating margin might fluctuated slightly over the last 12 months but has generally stayed the same, averaging 5.6% over the last five years. This profitability was paltry for a healthcare business and caused by its suboptimal cost structure.

Looking at the trend in its profitability, Progyny’s operating margin might fluctuated slightly but has generally stayed the same over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, Progyny generated an operating margin profit margin of 4.8%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

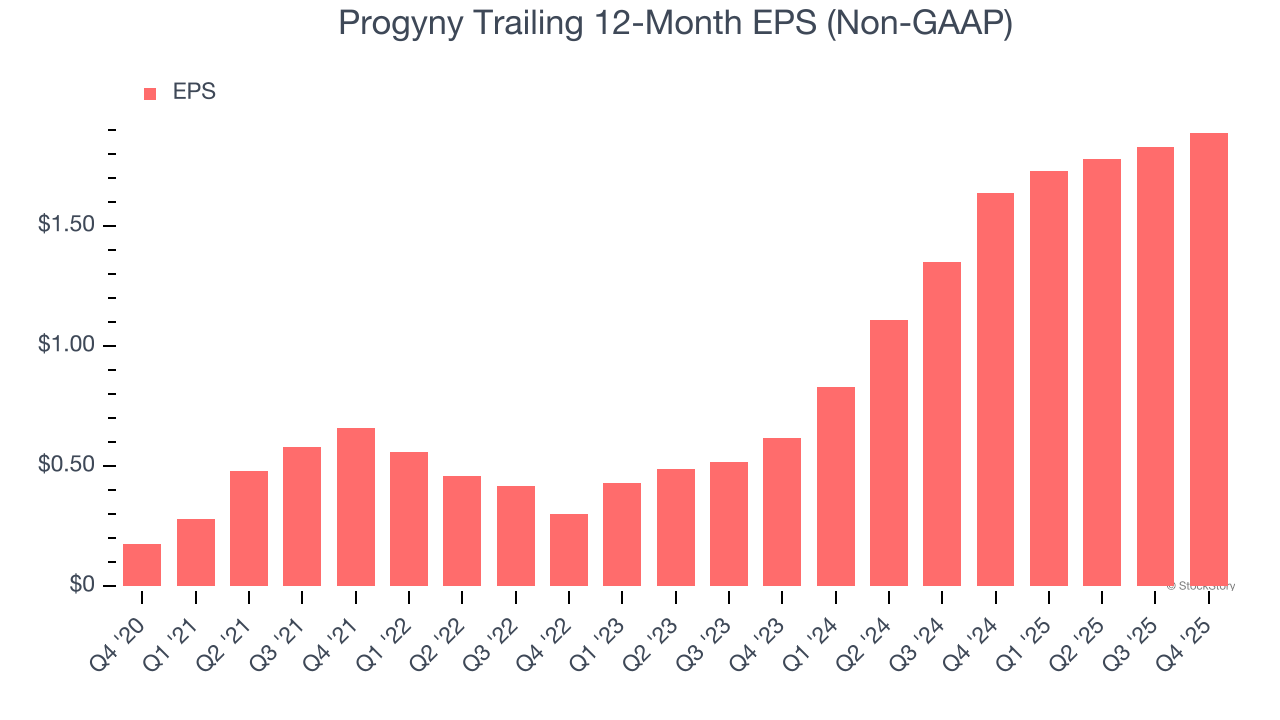

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Progyny’s EPS grew at an astounding 60.5% compounded annual growth rate over the last five years, higher than its 30.2% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

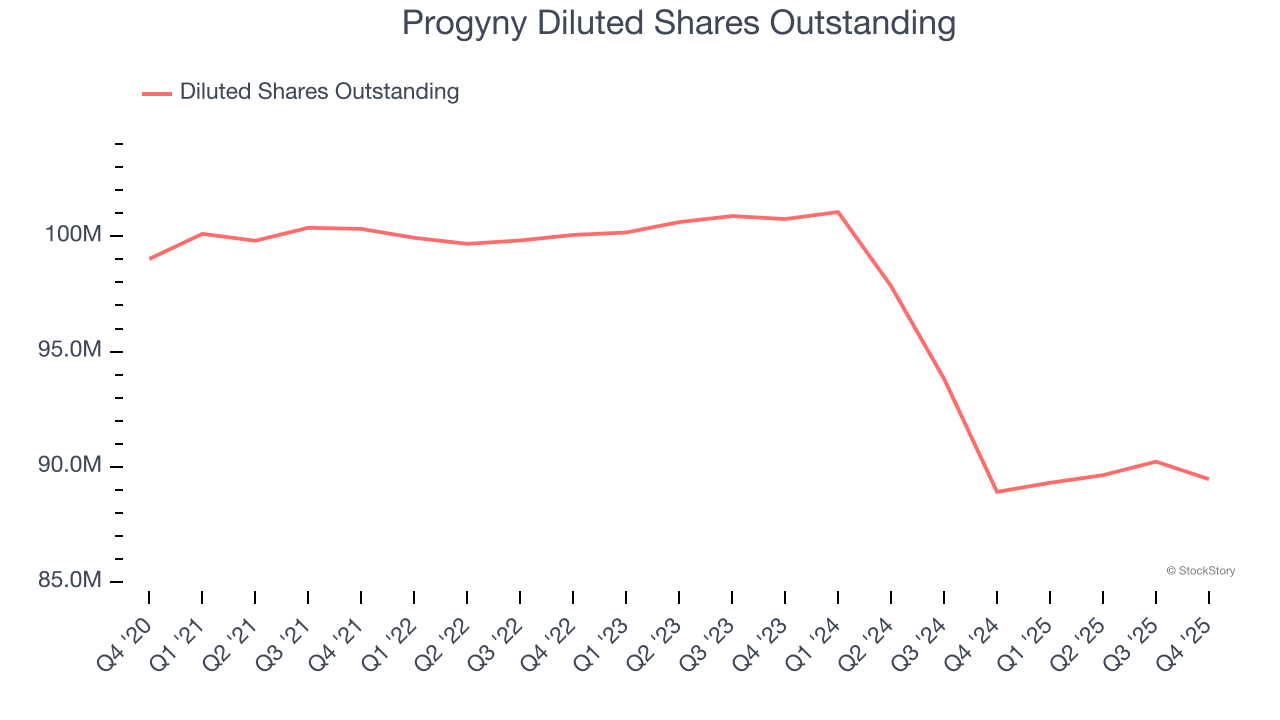

Diving into the nuances of Progyny’s earnings can give us a better understanding of its performance. A five-year view shows that Progyny has repurchased its stock, shrinking its share count by 9.7%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

In Q4, Progyny reported adjusted EPS of $0.48, up from $0.42 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Progyny’s full-year EPS of $1.89 to grow 2.7%.

Key Takeaways from Progyny’s Q4 Results

It was good to see Progyny beat analysts’ EPS expectations this quarter. We were also glad its revenue outperformed Wall Street’s estimates. On the other hand, its full-year EPS guidance missed and its revenue guidance for next quarter fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 2.3% to $21.75 immediately following the results.

Progyny’s latest earnings report disappointed. One quarter doesn’t define a company’s quality, so let’s explore whether the stock is a buy at the current price. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).