Quarterly earnings results are a good time to check in on a company’s progress, especially compared to its peers in the same sector. Today we are looking at Nature's Sunshine (NASDAQ: NATR) and the best and worst performers in the personal care industry.

While personal care products products may seem more discretionary than food, consumers tend to maintain or even boost their spending on the category during tough times. This phenomenon is known as "the lipstick effect" by economists, which states that consumers still want some semblance of affordable luxuries like beauty and wellness when the economy is sputtering. Consumer tastes are constantly changing, and personal care companies are currently responding to the public’s increased desire for ethically produced goods by featuring natural ingredients in their products.

The 12 personal care stocks we track reported a mixed Q4. As a group, revenues beat analysts’ consensus estimates by 1.3% while next quarter’s revenue guidance was 1.5% above.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 9.5% since the latest earnings results.

Nature's Sunshine (NASDAQ: NATR)

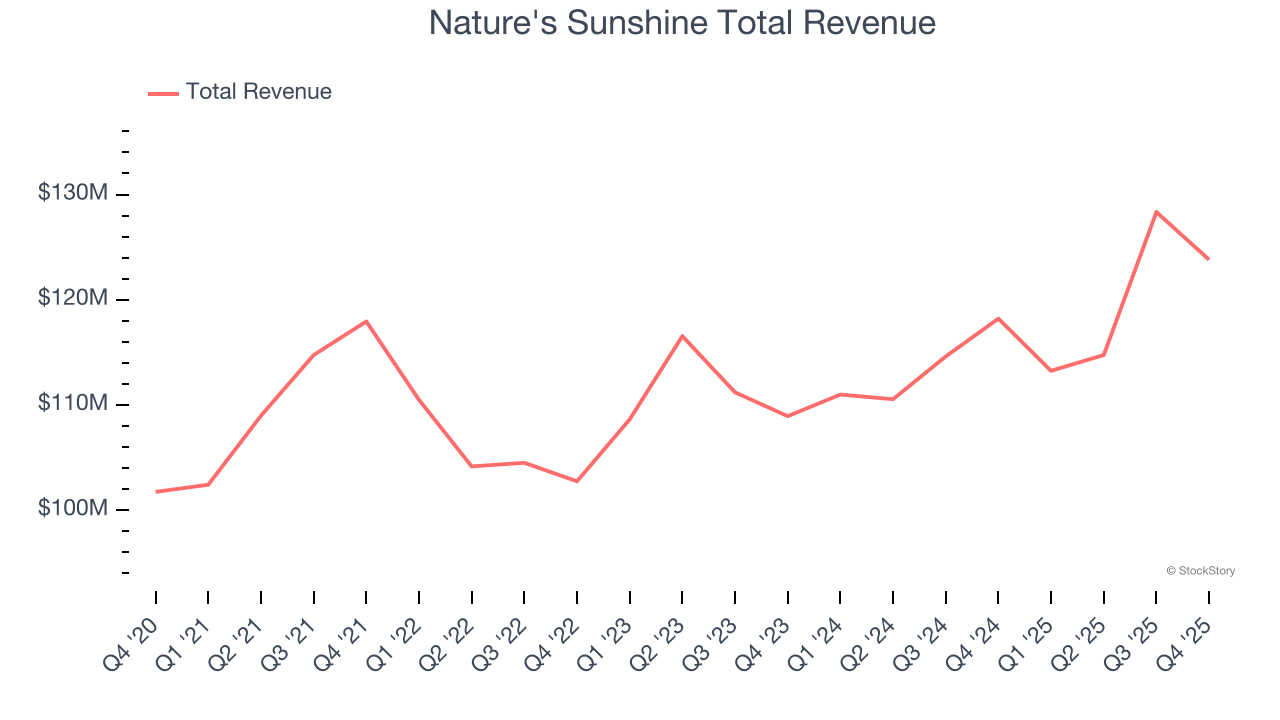

Started on a kitchen table in Utah, Nature’s Sunshine (NASDAQ: NATR) manufactures and sells nutritional and personal care products.

Nature's Sunshine reported revenues of $123.8 million, up 4.7% year on year. This print exceeded analysts’ expectations by 1.9%. Overall, it was an exceptional quarter for the company with a beat of analysts’ EPS estimates and an impressive beat of analysts’ EBITDA estimates.

“We finished a record year in sales and delivered our second‑best quarter ever and our largest Q4 on record, with sales and adjusted EBITDA up 5% and 16%, respectively,” said Ken Romanzi, CEO of Nature’s Sunshine.

Unsurprisingly, the stock is down 2.4% since reporting and currently trades at $24.48.

Is now the time to buy Nature's Sunshine? Access our full analysis of the earnings results here, it’s free.

Best Q4: e.l.f. Beauty (NYSE: ELF)

Short for "eyes, lips, face", e.l.f. Beauty (NYSE: ELF) is a developer of high-quality beauty products at accessible price points.

e.l.f. Beauty reported revenues of $489.5 million, up 37.8% year on year, outperforming analysts’ expectations by 6.4%. The business had a stunning quarter with a beat of analysts’ EPS estimates and an impressive beat of analysts’ EBITDA estimates.

e.l.f. Beauty delivered the biggest analyst estimates beat and fastest revenue growth among its peers. Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 13.7% since reporting. It currently trades at $73.01.

Is now the time to buy e.l.f. Beauty? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Medifast (NYSE: MED)

Known for its Optavia program that combines portion-controlled meal replacements with coaching, Medifast (NYSE: MED) has a broad product portfolio of bars, snacks, drinks, and desserts for those looking to lose weight or consume healthier foods.

Medifast reported revenues of $75.1 million, down 36.9% year on year, exceeding analysts’ expectations by 5.2%. Still, it was a softer quarter as it posted full-year revenue guidance missing analysts’ expectations significantly and full-year EPS guidance missing analysts’ expectations significantly.

Medifast delivered the highest full-year guidance raise but had the slowest revenue growth in the group. As expected, the stock is down 13% since the results and currently trades at $9.40.

Read our full analysis of Medifast’s results here.

Herbalife (NYSE: HLF)

With the first products sold out of the trunk of the founder’s car, Herbalife (NYSE: HLF) today offers a portfolio of shakes, supplements, personal care products, and weight management programs to help customers reach their nutritional and fitness goals.

Herbalife reported revenues of $1.28 billion, up 6.3% year on year. This print surpassed analysts’ expectations by 3.6%. Zooming out, it was a satisfactory quarter as it also produced a solid beat of analysts’ gross margin estimates but a significant miss of analysts’ EPS estimates.

The stock is down 6.8% since reporting and currently trades at $15.42.

Read our full, actionable report on Herbalife here, it’s free.

USANA (NYSE: USNA)

Going to market with a direct selling model rather than through traditional retailers, USANA Health Sciences (NYSE: USNA) manufactures and sells nutritional, personal care, and skincare products.

USANA reported revenues of $226.2 million, up 5.9% year on year. This result met analysts’ expectations. Overall, it was a strong quarter as it also produced a beat of analysts’ EPS estimates and a solid beat of analysts’ EBITDA estimates.

The stock is down 16.2% since reporting and currently trades at $17.31.

Read our full, actionable report on USANA here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our 9 Best Market-Beating Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.