")

While OKYO Pharma Ltd. (NASDAQ: OKYO) stock is now around 89% higher than its August low, recent news supports that the gain is likely a precursor to an even more appreciable increase. Why? Because at $2.37 per share*, OKYO is in a better position today compared to when it scored its 52-week high 66% higher than current levels. But that disconnect may not last much longer. With shares higher by 24% since Monday, investors appear clued into more than OKYO stocks' rebound momentum; they appear confident OKYO can expedite getting its flagship drug candidate, OK-101, to market. (*share price on 10/4/23, Yahoo! Finance at 11:08 AM EST)

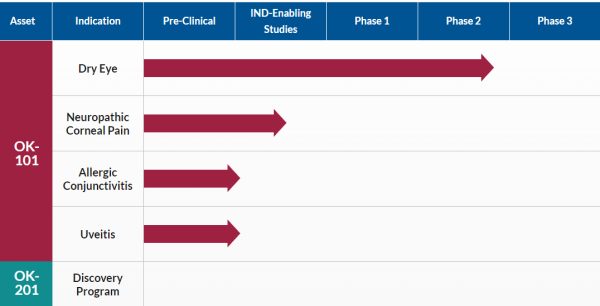

OKYO's OK-101 is a lipidated chemerin-peptide designed to target a critical ocular receptor controlling inflammation and ocular pain. Its differences, which include a unique proprietary membrane-anchored technology, make the treatment candidate stand out among competitors. Moreover, because it's designed to increase agonist potency and ocular residence time, OKYO believes it can become a leading drug against inflammatory dry eye (DED) disease.

If so, OKYO's next-gen drug could bring life-changing relief to the estimated 700 million people worldwide suffering from dry eye disease, including the 30 million patients in the US alone. Compounding the issue is that the current standard of care has significant limitations, especially those associated with care providers prescribing eyedrops containing antihistamines or steroids. That's not an ideal solution since steroids often increase eye pressure and raise the risk of infection and cataracts if used for long periods. Fortunately, OKYO intends to change that practice.

The company is focused on bringing patients a safe and well-tolerated drug that overcomes the limitations of current DED treatments. Better yet, they are on the right path to deliver, with its OK-101 drug candidate demonstrating its worth as a first-in-class drug combining both anti-inflammatory and pain-reducing activity.

OK-101 is Timely to Its Opportunities

In addition to being on the right path, OKYO is timely to the need. Dry Eye Disease affects over 35% of the population aged 50+, with women representing approximately two-thirds of those impacted. While that affliction rate is high today, it's forecasted to worsen due to an aging population and increased use of contact lenses and digital screen time. Those affected know that better treatments are needed, particularly ones that don't have inherent side effects that can be as bad as the condition treated. OKYO Pharma checks that box.

That's excellent news to those suffering from DED conditions, including the over five million suffering from neuropathic corneal pain, a severe, chronic, and debilitating disease for which no currently approved commercial treatments exist. The ones used in the meantime include short-term NSAIDs, steroids, and even opioids in severe cases, all associated with known adverse side effects. Opioids also add the risk of addiction, causing some prescribers to not offer it, sometimes leaving patients with untreated severe pain.

In contrast, OKYO's OK-101 does not come with the added side effect baggage. Furthermore, topical administration of OK-101 effectively suppresses corneal pain in a ciliary nerve ligation mouse model of neuropathic corneal pain. Better still, it exhibited a potency similar to gabapentin, a commonly used oral drug for neuropathic pain delivered by intraperitoneal injection. That market alone represents an estimated $500 million revenue-generating opportunity, income that could accrue quickly from OK-101 providing ocular pain relief and anti-inflammatory effects. Best of all, considering no commercially approved topical treatments are available for this condition, OKYO could earn a significant market share faster than expected.

OKYO isn't stopping there, however. The company has identified additional target markets that may benefit from its game-changing treatment candidate.

Treating Eye Disease in a Safer Way

That includes an over $1 billion opportunity in the US markets to effectively treat allergic conjunctivitis, often called 'pink eye.' This condition results from an inflammation of the conjunctiva caused by an allergic reaction to pollen, mold, smoke, dust, and other contaminants. It, too, affects a significant patient population. Reports indicate that up to 40% of the global population suffers from allergic conjunctivitis, primarily treated with antihistamines and corticosteroids.

The issue with prescribing those drugs is that many patients do not respond to antihistamines, which, in many cases, leads to the overuse of corticosteroids in these patients. In an animal model, OKYO's OK-101 effectively suppressed ocular inflammation by downregulating key inflammatory CD4+ T cells. Additional studies are ongoing to determine the efficacy of OK-101 in diminishing ocular redness, the most common symptom of allergic conjunctivitis.

OKYO is further targeting effective treatment of uveitis, the third leading cause of blindness worldwide. The most common type of uveitis is an inflammation of the iris called iritis. Worst case, uveitis damages vital eye tissue, leading to permanent vision loss. Similar to other eye diseases, treatment for this condition also involves prescription steroids, most commonly corticosteroid eyedrops, and injections that reduce inflammation. Again, that's not an optimal solution.

The long-term use of corticosteroids causes the risk of cataracts and glaucoma, requiring close monitoring for their potential side effects. That's not a tradeoff OKYO is willing to accept. Its focus is to use OK-101 to suppress the inflammation and pain associated with uveitis, which in animal models shows effectiveness in suppressing ocular inflammation by downregulating key inflammatory biomarkers CD4+ T cells.

As noted, OKYO intends to get its innovative, potential front-line treatments to market sooner rather than later.

Expediting Trial Pace Toward FDA Approvals

They intend to do that by skipping Phase I, designing its Phase II trial as a Phase III registration trial. More simply said, the strategy is to shave what could amount to years off its total trial duration. And they very well could, given that OK-101 overcomes the major challenge associated with topical administration treating any ocular eye disease: wash-out. Wash-out occurs through the natural processes of tearing and blinking, minimizing drug 'residence' time and pharmacologic benefits at the ocular site. That isn't a concern with OKYO's OK-101.

Its formulation includes Membrane Anchored Peptide (MAP) technology, which enables a long-acting and stable therapeutic delivery. The innovative approach includes using a 10-mer C-terminal chemerin peptide sequence, a linker component, and an anchoring lipid domain. Results to date are impressive. OKYO published that animals induced with scopolamine to generate acute dry eye disease (DED) showed a dramatic, statistically significant increase in corneal permeability relative to naïve non-stressed animals. Cyclosporine, the positive control in the DED study, showed a statistically significant reduction in corneal permeability (p ≤ 0.001) in scopolamine-induced DED animals.

The excellent news for OKYO, as well as its potential patients and investors, is that OK-101's effect in reducing DED-induced corneal permeability was virtually identical to that of the cyclosporine positive control and close to the baseline corneal permeability observed in non-stressed control animals. In other words, it demonstrated compelling and positive results while at the same time showing itself to be a safer treatment option.

Also notable is that OK-101 demonstrated a statistically significant (p ≤ 0.01) reduction in dry-eye-induced enhancement of inflammatory CD4+ T-cells. The levels of CD4+ T cells observed in OK-101 treated animals were equivalent to the CD4+ T cell level observed in naïve untreated animals. Results are driven by unique MAP technology enabling the development of OK-101 with enhanced potency and the expectation of increased drug residence time on the ocular surface. Thus, the precedent of positive results is expected to continue.

Positioned to Capitalize on DED Market Opportunities

That should contribute to OKYO capitalizing on a combined $5 billion dry eye market opportunity. Growth could come faster than many think, noting the company submitted an IND in Q4 2022. That combines with OKYO's plans of skipping Phase I and going directly to a Phase II safety and efficacy trial, a process that began in May 2023 to treat eye diseased patients.

More good news related to that trial is that topline results are expected in Q4 of this year. That puts a milestone in the queue that could catalyze company growth and share price appreciation. In other words, just as OKYO is timely to its enormous revenue-generating opportunities, so are the investors taking advantage of a valuation disconnect between share price and its assets and pipeline. In fact, well off its 52-week high, and after completing a gross proceeds capital raise of $4 million in September, OKYO looks better positioned than ever to do more than capitalize on its opportunities; it can maximize them.

Disclaimers: Shore Thing Media, LLC. (STM) is responsible for the production and distribution of this content. STM is not operated by a licensed broker, a dealer, or a registered investment adviser. It should be expressly understood that under no circumstances does any information published herein represent a recommendation to buy or sell a security. Our reports/releases are a commercial advertisement and are for general information purposes ONLY. We are engaged in the business of marketing and advertising companies for monetary compensation. Never invest in any stock featured on our site or emails unless you can afford to lose your entire investment. The information made available by STM is not intended to be, nor does it constitute, investment advice or recommendations. The contributors may buy and sell securities before and after any particular article, report and publication. In no event shall STM be liable to any member, guest or third party for any damages of any kind arising out of the use of any content or other material published or made available by STM, including, without limitation, any investment losses, lost profits, lost opportunity, special, incidental, indirect, consequential or punitive damages. Past performance is a poor indicator of future performance. The information in this video, article, and in its related newsletters, is not intended to be, nor does it constitute, investment advice or recommendations. STM strongly urges you conduct a complete and independent investigation of the respective companies and consideration of all pertinent risks. Readers are advised to review SEC periodic reports: Forms 10-Q, 10K, Form 8-K, insider reports, Forms 3, 4, 5 Schedule 13D. For some content, STM, its authors, contributors, or its agents, may be compensated for preparing research, video graphics, and editorial content. Shore Thing Media Group, LLC., through its digital website property, Primetime Profiles, has been compensated two-thousand-dollars cash via wire transfer to produce and syndicate content for OKYO Pharma, Ltd. for a period of one day beginning and ending on 10/05/23. Please read the full disclaimer at https://primetimeprofiles.com/disclaimer/ for important information about this content. This compensation is a major conflict of interest in our ability to be unbiased regarding our alerts. Therefore, this communication should be viewed as a commercial advertisement only. Any non- compensated alerts are purely for the purpose of expanding our database for the benefit of our future financially compensated investor relations efforts. As part of all content, readers, subscribers, and website viewers, are expected to read the full disclaimers and financial disclosures statement that can be found on our website. Contributors reserve the right, but are not obligated to, submit articles for fact-checking prior to publication. Contributors are under no obligation to accept revisions when not factually supported. Furthermore, because contributors are compensated, readers and viewers of this content should always assume that content provided shows only the positive side of companies, and rarely, if ever, highlights the risks associated with investment. Thus, readers and viewers should accept the content as an advertorial that highlights only the best features of a company. Never take opinion, articles presented, or content provided as a sole reason to invest in any featured company. Investors must always perform their own due diligence prior to investing in any publicly traded company and understand the risks involved, including losing their entire investment.

The Private Securities Litigation Reform Act of 1995 provides investors a safe harbor in regard to forward-looking statements. Any statements that express or involve discussions with respect to predictions, expectations, beliefs, plans, projections, objectives, goals, assumptions or future events or performance are not statements of historical fact may be forward looking statements. Forward looking statements are based on expectations, estimates, and projections at the time the statements are made that involve a number of risks and uncertainties which could cause actual results or events to differ materially from those presently anticipated. Forward looking statements in this action may be identified through use of words such as projects, foresee, expects, will, anticipates, estimates, believes, understands, or that by statements indicating certain actions & quote; may, could, or might occur. Understand there is no guarantee past performance will be indicative of future results. Investing in micro-cap and growth securities is highly speculative and carries an extremely high degree of risk. It is possible that an investors investment may be lost or impaired due to the speculative nature of the companies profiled.

Media Contact

Company Name: STM, LLC.

Contact Person: Michael Thomas

Email: contact@primetimeprofiles.com

Country: United States

Website: https://primetimeprofiles.com/