Valued at a market cap of $10.2 billion, FactSet Research Systems Inc. (FDS) is a financial digital platform and enterprise solutions provider for the investment community. The Norwalk, Connecticut-based company offers comprehensive data feeds, research tools, portfolio analytics, trading solutions, and workflow automation used by asset managers, investment banks, hedge funds, and corporate clients.

Shares of this financial company have significantly underperformed the broader market over the past 52 weeks. FDS has declined 44.3% over this time frame, while the broader S&P 500 Index ($SPX) has soared 11%. Moreover, on a YTD basis, the stock is down 43.4%, compared to SPX’s 14% return.

Narrowing the focus, FDS has also notably lagged behind the iShares U.S. Broker-Dealers & Securities Exchanges ETF (IAI), which has gained 11.6% over the past 52 weeks and 17.7% on a YTD basis.

On Sep. 18, shares of FDS plunged 10.4% after its mixed Q4 earnings release. On the upside, the company’s revenue increased 6.2% year-over-year to $596.9 million, beating consensus estimates by a slight margin. However, despite this, its adjusted operating margin declined by 200 basis points from the year-ago quarter, and its adjusted EPS of $4.05 fell 2.4% short of analyst expectations, dampening investor confidence.

For fiscal 2026, ending in August, analysts expect FDS’ EPS to grow 1.9% year over year to $17.30. The company’s earnings surprise history is mixed. It exceeded the consensus estimates in two of the last four quarters, while missing on two other occasions.

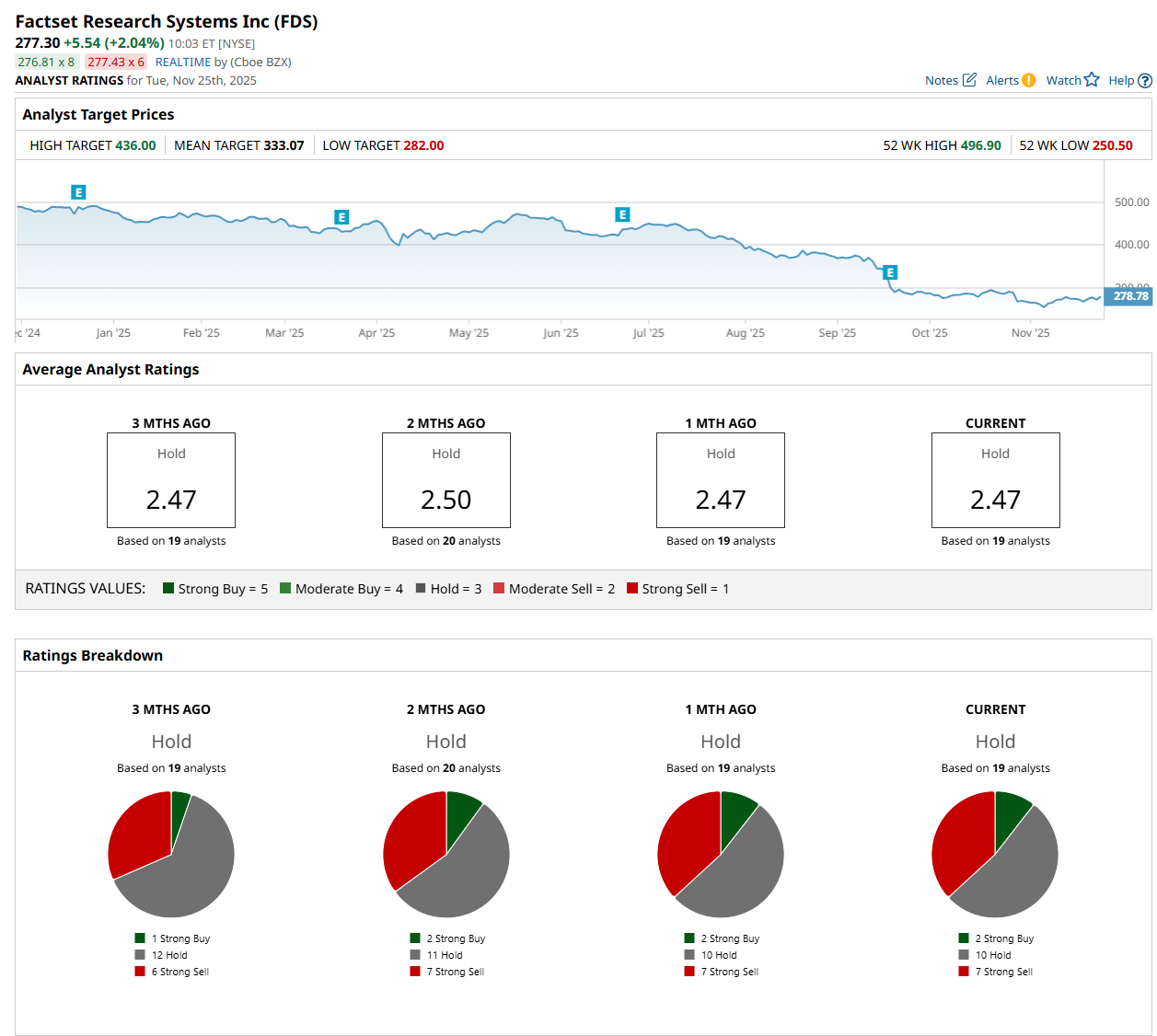

Among the 19 analysts covering the stock, the consensus rating is a "Hold,” which is based on two “Strong Buy,” 10 "Hold,” and seven "Strong Sell” ratings.

The configuration has changed since the past three months, with one analyst suggesting a "Strong Buy” rating and six recommending “Strong Sell.”

On Sep. 22, UBS Group AG (UBS) upgraded FDS to “Buy,” with a price target of $425, indicating a 53.3% potential upside from the current levels.

The mean price target of $333.07 represents a 20.1% premium from FDS’ current price levels, while the Street-high price target of $436 suggests an ambitious 57.2% potential upside from the current levels.

On the date of publication, Neharika Jain did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Occidental Petroleum Could Hike Its Dividend - Price Target is At Least 21% Higher

- This ‘Strong Buy’ Retail Stock Has Great Earnings Growth and Has Doubled This Year

- Our Top Chart Strategist Analyzes the 'Generational Buying Opportunity' in Meta Stock

- Corporate Insiders Have Sold $25 Billion in Stock in Just 60 Days. Before You Panic and Sell Your Shares, Read This.