Workday trades at $259.99 per share and has stayed right on track with the overall market, gaining 16.7% over the last six months. At the same time, the S&P 500 has returned 12.2%.

Is WDAY a buy right now? Find out in our full research report, it’s free.

Why Does Workday Spark Debate?

Founded by industry veterans Aneel Bushri and Dave Duffield after their former company PeopleSoft was acquired by Oracle in a hostile takeover, Workday (NASDAQ: WDAY) provides cloud-based software for organizations to manage and plan finance and human resources.

Two Positive Attributes:

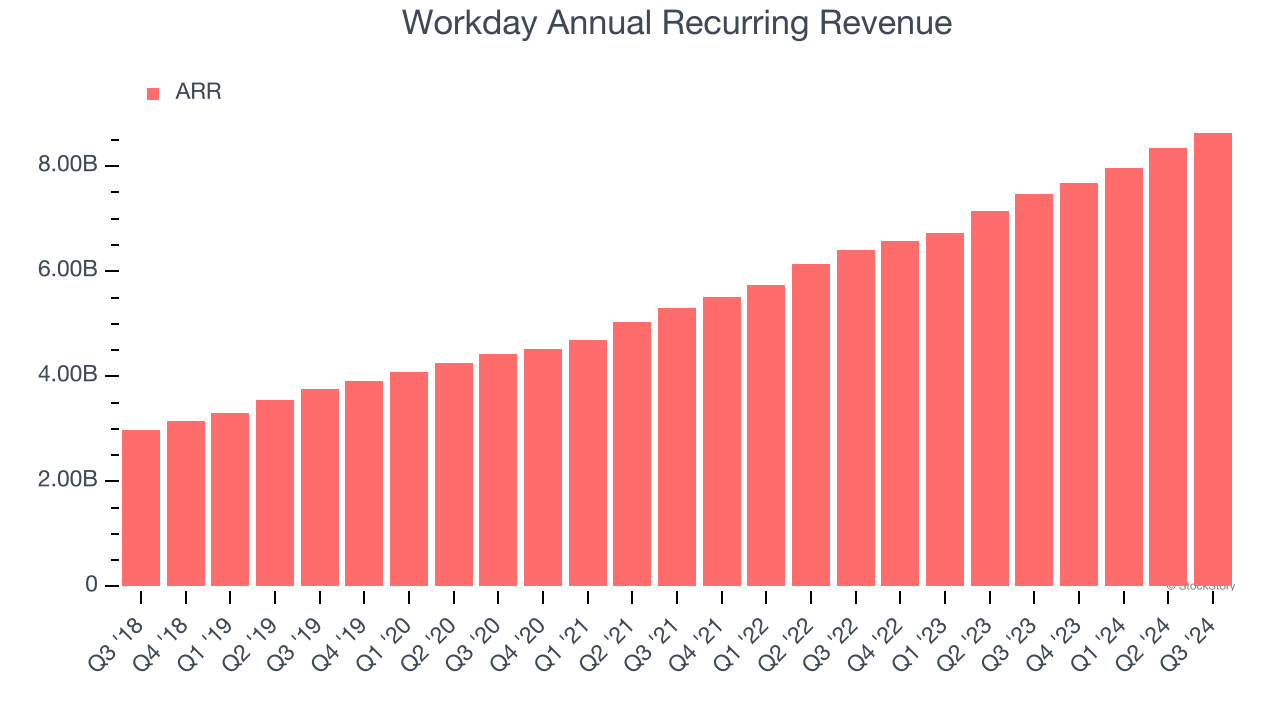

1. ARR Growth Powers Predictable Revenues

While reported revenue for a software company can include low-margin items like implementation fees, annual recurring revenue (ARR) is a sum of the next 12 months of contracted revenue purely from software subscriptions, or the high-margin, predictable revenue streams that make SaaS businesses so valuable.

Workday’s ARR punched in at $8.64 billion in Q3, and over the last four quarters, its year-on-year growth averaged 16.8%. This performance was solid, reflecting the company’s ability to maintain strong customer relationships and secure longer-term commitments. Its growth also contributes positively to Workday’s predictability and valuation, as investors typically prefer businesses with recurring revenue.

2. Excellent Free Cash Flow Margin Boosts Reinvestment Potential

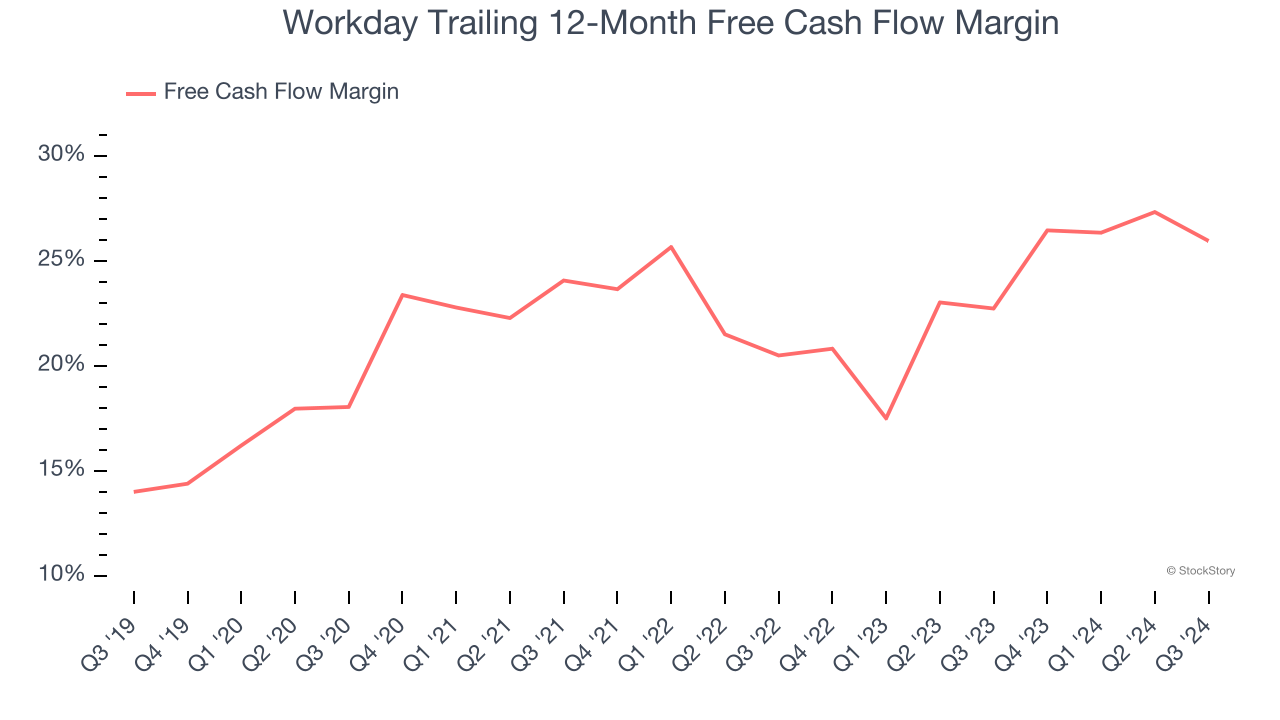

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Workday has shown robust cash profitability, driven by its attractive business model and cost-effective customer acquisition strategy that enable it to invest in new products and services rather than sales and marketing. The company’s free cash flow margin averaged 25.9% over the last year, quite impressive for a software business.

One Reason to be Careful:

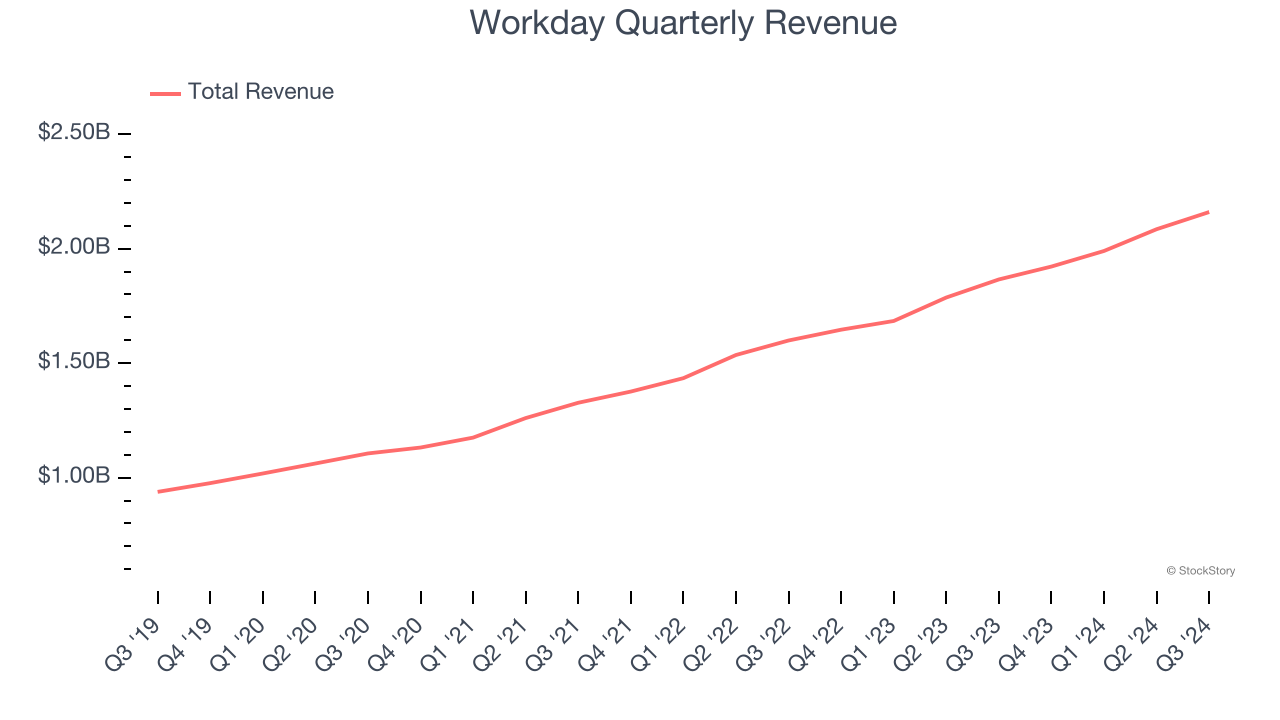

Long-Term Revenue Growth Disappoints

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Over the last three years, Workday grew its sales at a 18.6% compounded annual growth rate. Although this growth is acceptable on an absolute basis, it fell slightly short of our benchmark for the software sector, which enjoys a number of secular tailwinds. Luckily, there are other things to like about Workday.

Final Judgment

Workday’s merits more than compensate for its flaws, but at $259.99 per share (or 7.6× forward price-to-sales), is now the time to initiate a position? See for yourself in our full research report, it’s free.

Stocks We Like Even More Than Workday

The elections are now behind us. With rates dropping and inflation cooling, many analysts expect a breakout market - and we’re zeroing in on the stocks that could benefit immensely.

Take advantage of the rebound by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today for free.