Quest has followed the market’s trajectory closely, rising in tandem with the S&P 500 over the past six months. The stock has climbed by 13% to $170.50 per share while the index has gained 9.4%.

Is there a buying opportunity in Quest, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

We're cautious about Quest. Here are three reasons why DGX doesn't excite us and a stock we'd rather own.

Why Is Quest Not Exciting?

Founded in 1967 as MetPath, Quest Diagnostics (NYSE: DGX) is a provider of diagnostic testing services, offering a broad range of tests for medical conditions such as diabetes, heart disease, and infections, as well as genetic testing and drug monitoring services.

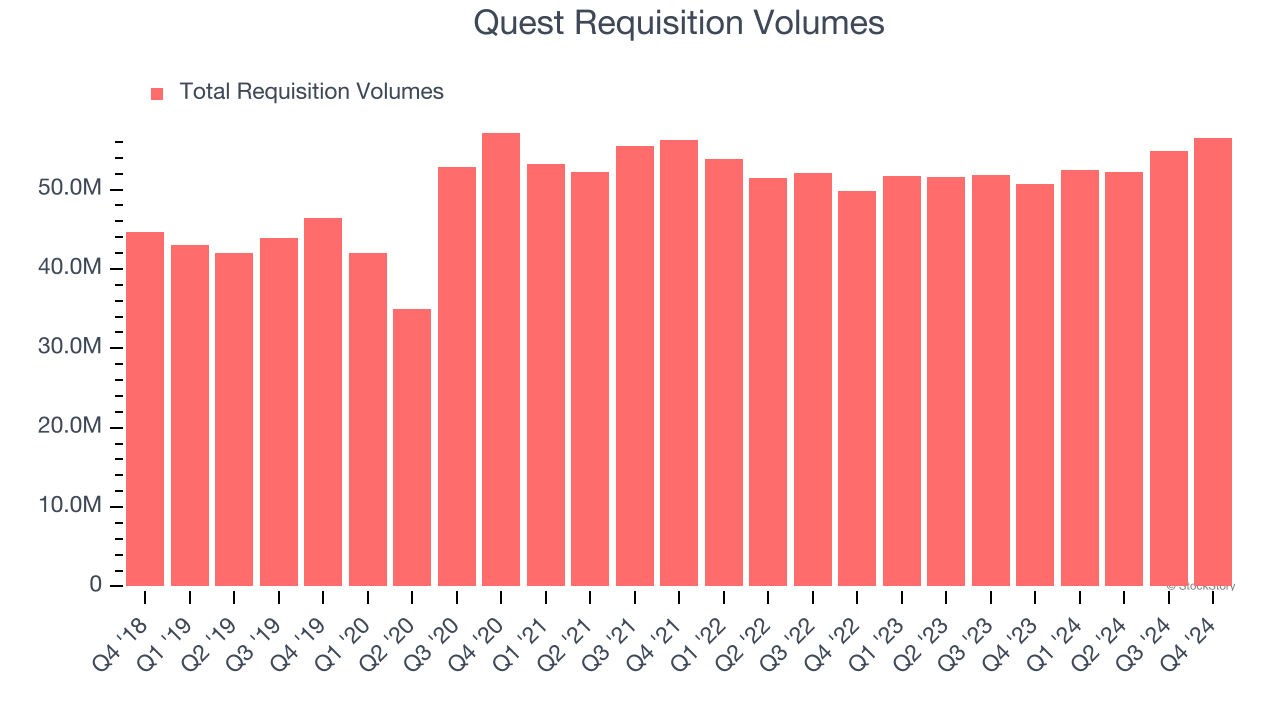

1. Weak Sales Volumes Indicate Waning Demand

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful Testing & Diagnostics Services company because there’s a ceiling to what customers will pay.

Quest’s requisition volumes came in at 56.51 million in the latest quarter, and over the last two years, averaged 2.5% year-on-year growth. This performance slightly lagged the sector and suggests it might have to lower prices or invest in product improvements to accelerate growth, factors that can hinder near-term profitability.

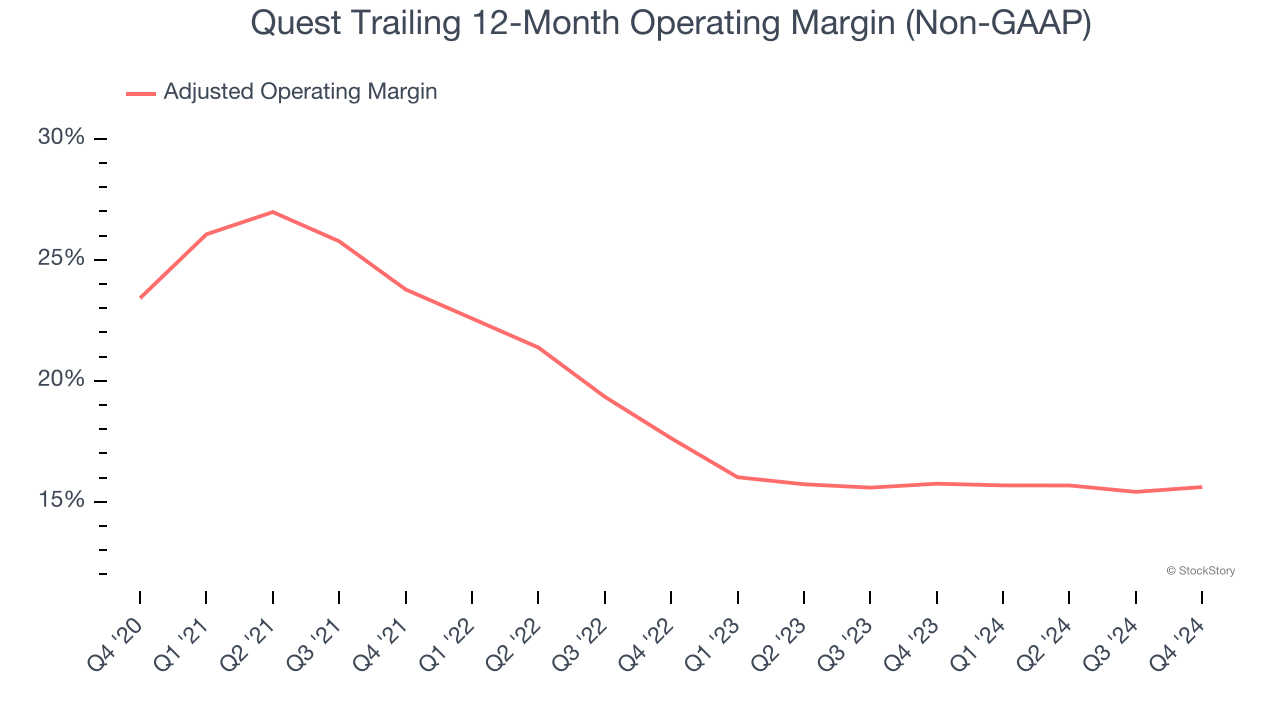

2. Shrinking Adjusted Operating Margin

Adjusted operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D. It also removes various one-time costs to paint a better picture of normalized profits.

Analyzing the trend in its profitability, Quest’s adjusted operating margin decreased by 7.8 percentage points over the last five years. Even though its historical margin is high, shareholders will want to see Quest become more profitable in the future. Its adjusted operating margin for the trailing 12 months was 15.6%.

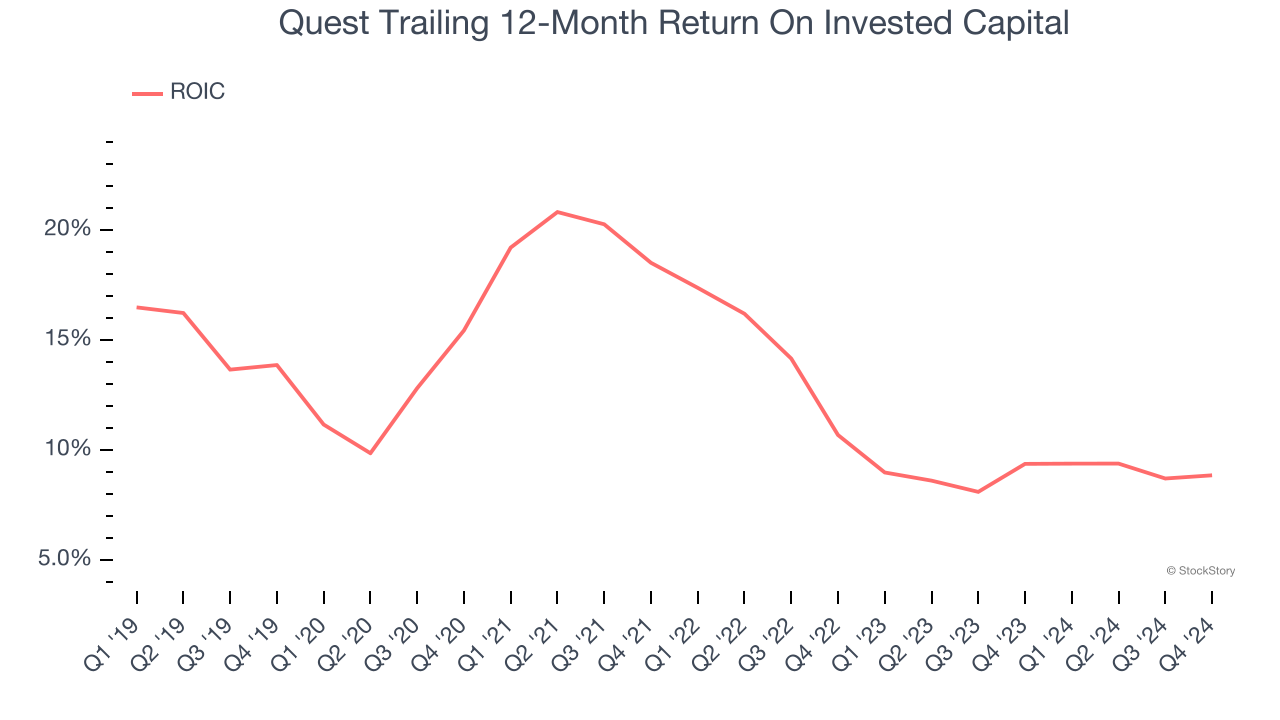

3. New Investments Fail to Bear Fruit as ROIC Declines

A company’s ROIC, or return on invested capital, shows how much operating profit it makes compared to the money it has raised (debt and equity).

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Quest’s ROIC has decreased over the last few years. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

Final Judgment

Quest isn’t a terrible business, but it doesn’t pass our bar. That said, the stock currently trades at 17.7× forward price-to-earnings (or $170.50 per share). Investors with a higher risk tolerance might like the company, but we think the potential downside is too great. We're fairly confident there are better stocks to buy right now. We’d suggest looking at our favorite semiconductor picks and shovels play.

Stocks We Would Buy Instead of Quest

The elections are now behind us. With rates dropping and inflation cooling, many analysts expect a breakout market - and we’re zeroing in on the stocks that could benefit immensely.

Take advantage of the rebound by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free.