Steel and waste handling company Enviri (NYSE: NVRI) fell short of the market’s revenue expectations in Q4 CY2024, but sales rose 5.7% year on year to $558.7 million. Its non-GAAP loss of $0.04 per share was 61% above analysts’ consensus estimates.

Is now the time to buy Enviri? Find out by accessing our full research report, it’s free.

Enviri (NVRI) Q4 CY2024 Highlights:

- Revenue: $558.7 million vs analyst estimates of $579 million (5.7% year-on-year growth, 3.5% miss)

- Adjusted EPS: -$0.04 vs analyst estimates of -$0.10 (61% beat)

- Adjusted EBITDA: $70.2 million vs analyst estimates of $72.63 million (12.6% margin, 3.3% miss)

- Adjusted EPS guidance for the upcoming financial year 2025 is -$0.13 at the midpoint, missing analyst estimates by 193%

- EBITDA guidance for the upcoming financial year 2025 is $315 million at the midpoint, below analyst estimates of $337.2 million

- Operating Margin: -11.2%, down from 5.1% in the same quarter last year

- Free Cash Flow Margin: 0.3%, down from 4.3% in the same quarter last year

- Market Capitalization: $699.6 million

“Enviri performed well in 2024, and we continued to focus on consistent execution in the fourth quarter as we faced ongoing headwinds at Harsco Environmental and Rail,” said Enviri Chairman and CEO Nick Grasberger.

Company Overview

Cooling America’s first indoor ice rink in the 19th century, Enviri (NYSE: NVRI) offers steel and waste handling services.

Waste Management

Waste management companies can possess licenses permitting them to handle hazardous materials. Furthermore, many services are performed through contracts and statutorily mandated, non-discretionary, or recurring, leading to more predictable revenue streams. However, regulation can be a headwind, rendering existing services obsolete or forcing companies to invest precious capital to comply with new, more environmentally-friendly rules. Lastly, waste management companies are at the whim of economic cycles. Interest rates, for example, can greatly impact industrial production or commercial projects that create waste and byproducts.

Sales Growth

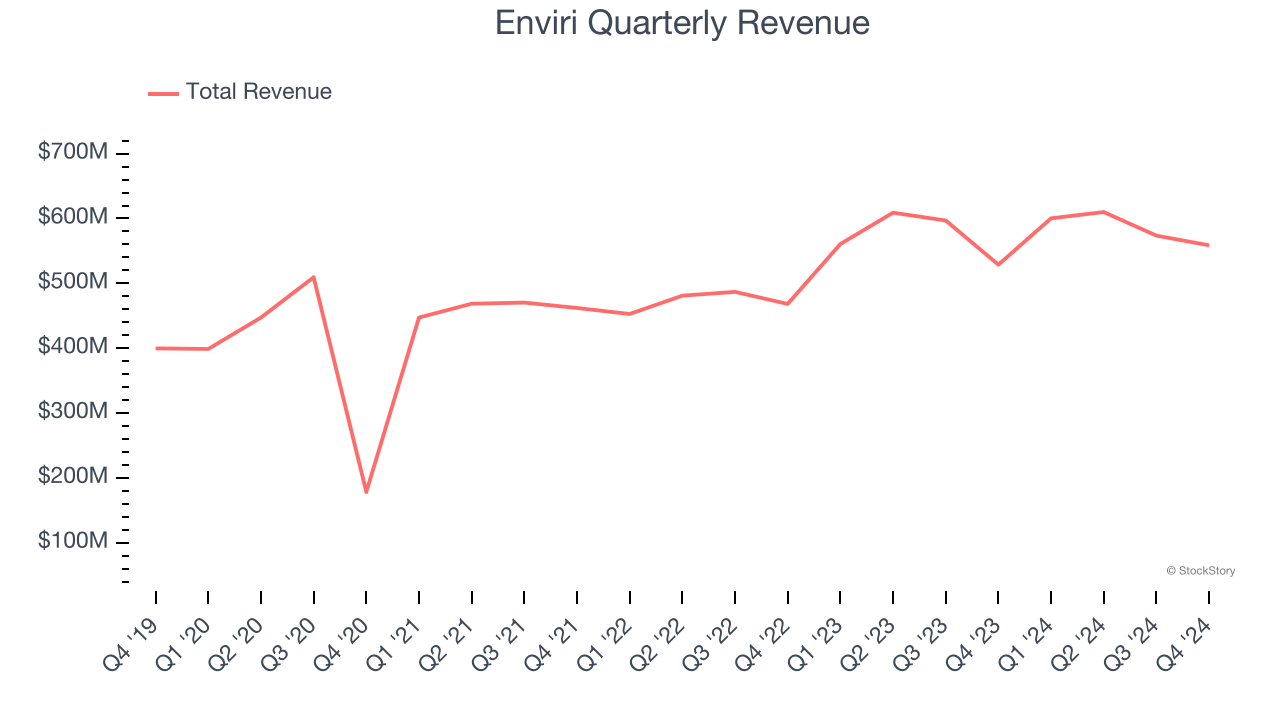

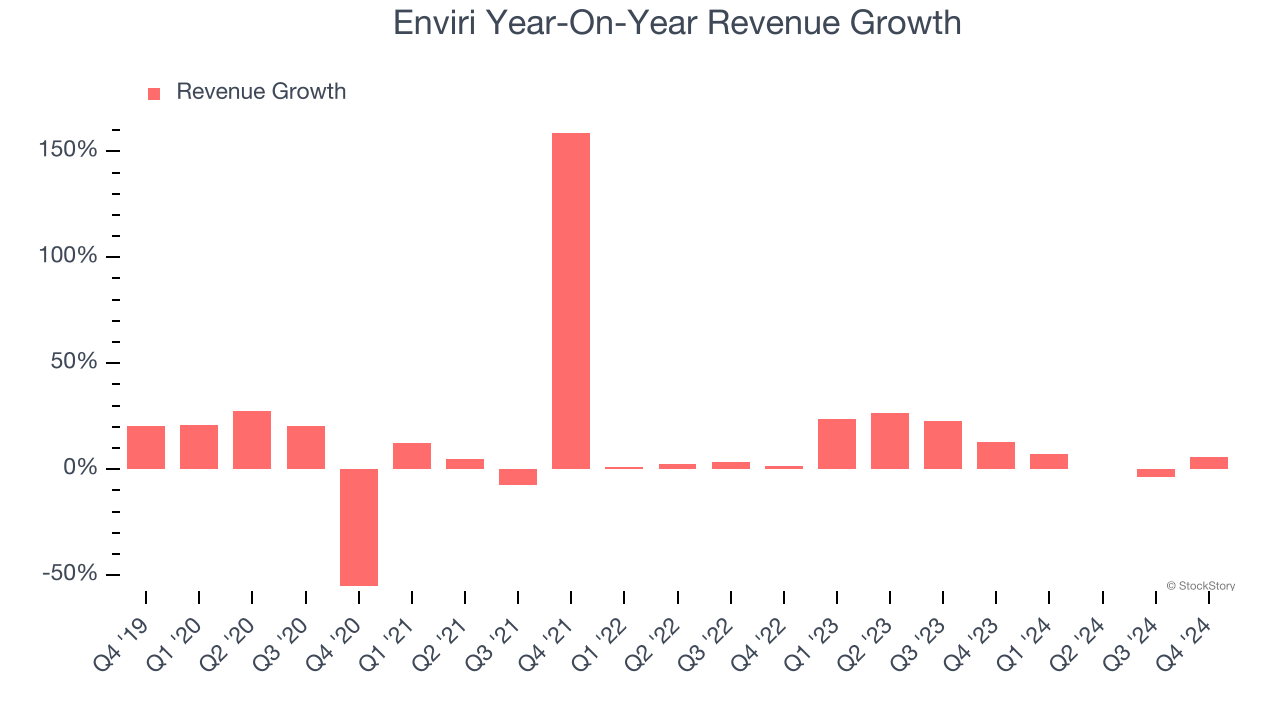

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Thankfully, Enviri’s 9.3% annualized revenue growth over the last five years was solid. Its growth beat the average industrials company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Enviri’s annualized revenue growth of 11.4% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

This quarter, Enviri’s revenue grew by 5.7% year on year to $558.7 million, missing Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 1.7% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and implies its products and services will face some demand challenges.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Operating Margin

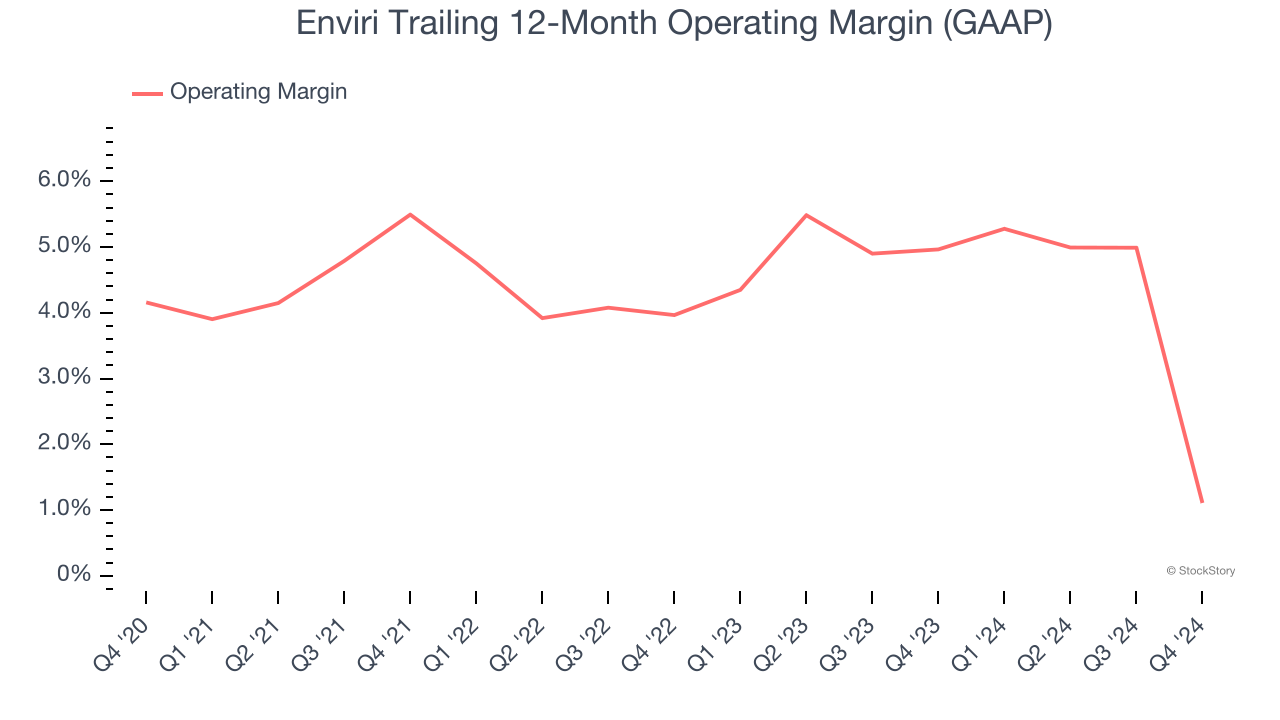

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

Enviri was profitable over the last five years but held back by its large cost base. Its average operating margin of 3.8% was weak for an industrials business. This result isn’t too surprising given its low gross margin as a starting point.

Analyzing the trend in its profitability, Enviri’s operating margin decreased by 3 percentage points over the last five years. The company’s performance was poor no matter how you look at it - it shows its expenses were rising and it couldn’t pass those costs onto its customers.

This quarter, Enviri generated an operating profit margin of negative 11.2%, down 16.3 percentage points year on year. Since Enviri’s operating margin decreased more than its gross margin, we can assume it was recently less efficient because expenses such as marketing, R&D, and administrative overhead increased.

Earnings Per Share

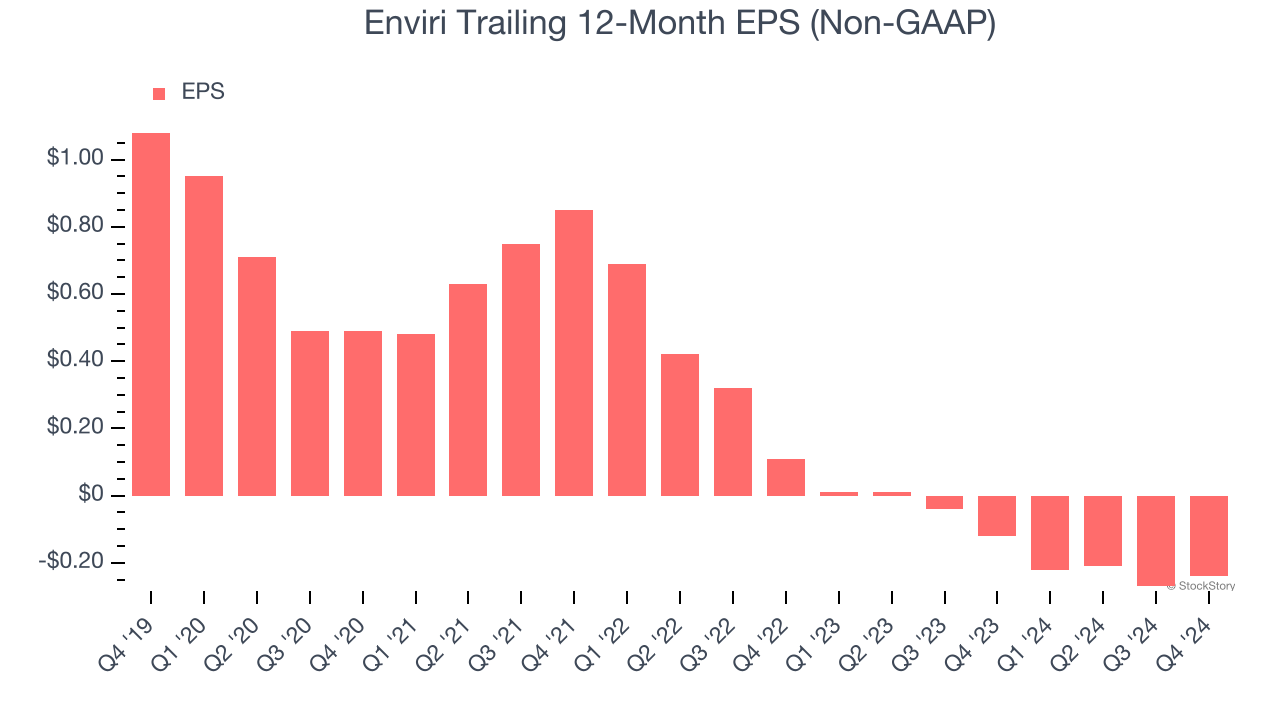

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Enviri, its EPS declined by 17.3% annually over the last five years while its revenue grew by 9.3%. This tells us the company became less profitable on a per-share basis as it expanded.

We can take a deeper look into Enviri’s earnings to better understand the drivers of its performance. As we mentioned earlier, Enviri’s operating margin declined by 3 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Enviri, its two-year annual EPS declines of 104% show it’s continued to underperform. These results were bad no matter how you slice the data.

In Q4, Enviri reported EPS at negative $0.04, up from negative $0.07 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street is optimistic. Analysts forecast Enviri’s full-year EPS of negative $0.24 will reach break even.

Key Takeaways from Enviri’s Q4 Results

We were impressed by how significantly Enviri blew past analysts’ EPS expectations this quarter. On the other hand, its full-year EBITDA guidance missed significantly and its revenue fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock remained flat at $8.73 immediately after reporting.

Enviri’s earnings report left more to be desired. Let’s look forward to see if this quarter has created an opportunity to buy the stock. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.