Automotive parts company LKQ (NASDAQ: LKQ) missed Wall Street’s revenue expectations in Q4 CY2024, with sales falling 4.1% year on year to $3.36 billion. Its non-GAAP profit of $0.80 per share was 7.8% above analysts’ consensus estimates.

Is now the time to buy LKQ? Find out by accessing our full research report, it’s free.

LKQ (LKQ) Q4 CY2024 Highlights:

- Revenue: $3.36 billion vs analyst estimates of $3.43 billion (4.1% year-on-year decline, 2% miss)

- Adjusted EPS: $0.80 vs analyst estimates of $0.74 (7.8% beat)

- Adjusted EBITDA: $408 million vs analyst estimates of $379 million (12.2% margin, 7.7% beat)

- Adjusted EPS guidance for the upcoming financial year 2025 is $3.55 at the midpoint, missing analyst estimates by 1.8%

- Operating Margin: 8.1%, in line with the same quarter last year

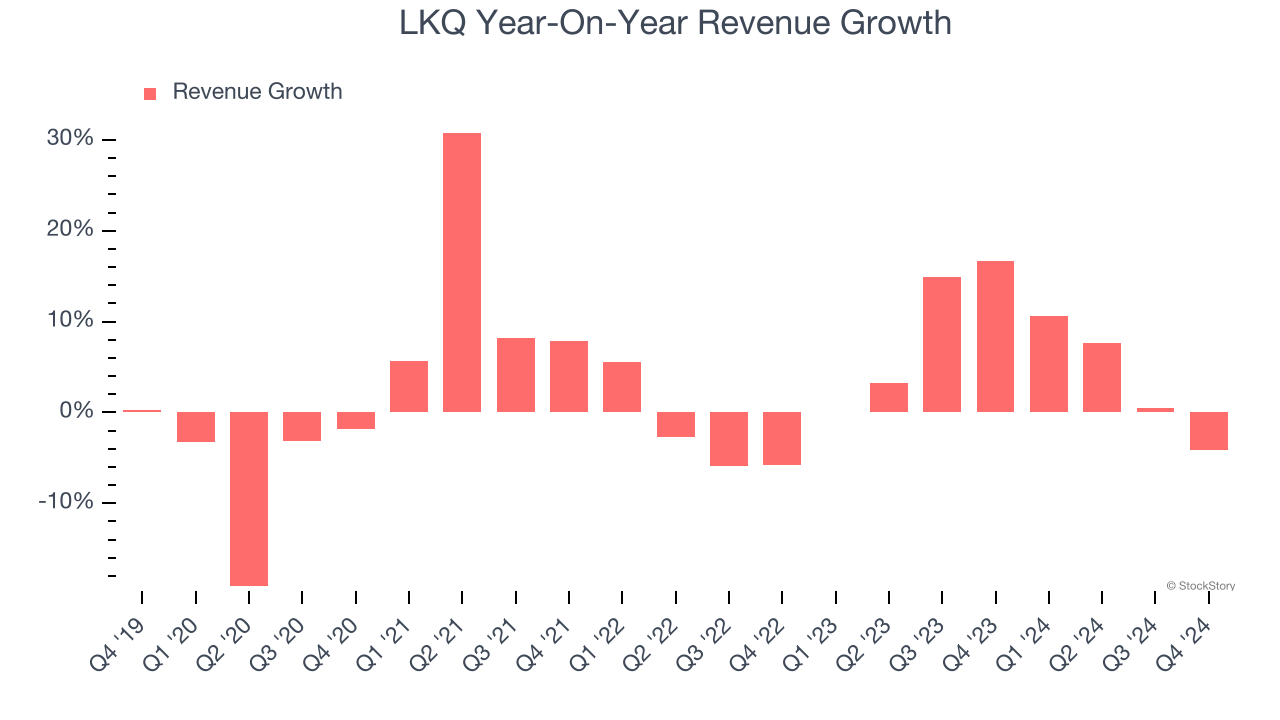

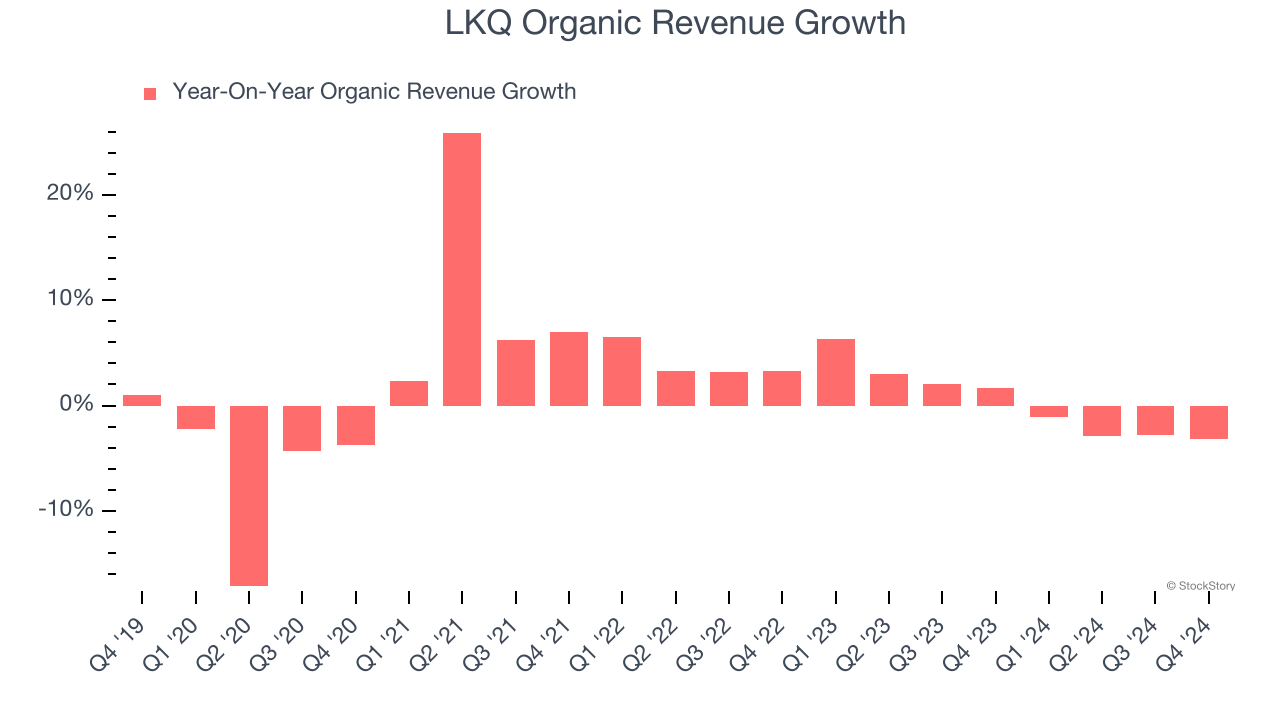

- Organic Revenue fell 3.2% year on year (1.7% in the same quarter last year)

- Market Capitalization: $10.24 billion

ANTIOCH, Tenn., Feb. 20, 2025 (GLOBE NEWSWIRE) -- LKQ Corporation (Nasdaq: LKQ) today reported fourth quarter and full year 2024 financial results. “The LKQ team focused on our core strengths to manage difficult market conditions in 2024 and position the Company for greater success in the future. I am proud of the team’s strong finish. Specifically, our Europe segment achieved an EBITDA margin of 10.1% in the quarter, which is a record for the segment in the fourth quarter. This was the third consecutive quarter the Europe segment attained double-digit EBITDA margins, and the Europe segment achieved its highest level of EBITDA dollars for a full year in 2024,” stated Justin Jude, President and Chief Executive Officer.

Company Overview

A global distributor of vehicle parts and accessories, LKQ (NASDAQ: LKQ) offers its customers a comprehensive selection of high-quality, affordably priced automobile products.

Specialized Consumer Services

Some consumer discretionary companies don’t fall neatly into a category because their products or services are unique. Although their offerings may be niche, these companies have often found more efficient or technology-enabled ways of doing or selling something that has existed for a while. Technology can be a double-edged sword, though, as it may lower the barriers to entry for new competitors and allow them to do serve customers better.

Sales Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, LKQ grew its sales at a weak 2.8% compounded annual growth rate. This fell short of our benchmarks and is a poor baseline for our analysis.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. LKQ’s annualized revenue growth of 5.9% over the last two years is above its five-year trend, but we were still disappointed by the results.

LKQ also reports organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, LKQ’s organic revenue was flat. Because this number is lower than its normal revenue growth, we can see that some mixture of acquisitions and foreign exchange rates boosted its headline results.

This quarter, LKQ missed Wall Street’s estimates and reported a rather uninspiring 4.1% year-on-year revenue decline, generating $3.36 billion of revenue.

Looking ahead, sell-side analysts expect revenue to grow 1.1% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and implies its products and services will see some demand headwinds.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

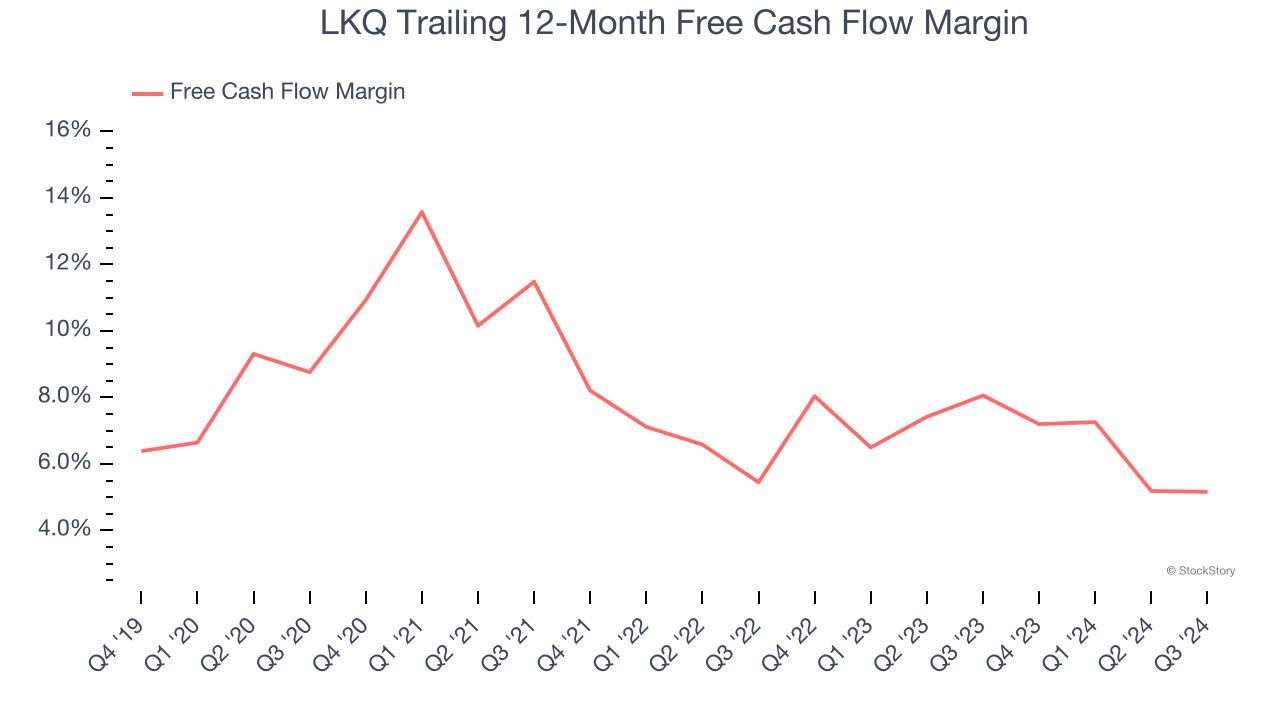

Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

LKQ has shown weak cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 6.7%, subpar for a consumer discretionary business.

Key Takeaways from LKQ’s Q4 Results

It was encouraging to see LKQ beat analysts’ EBITDA expectations this quarter. We were also happy its EPS outperformed Wall Street’s estimates. On the other hand, its revenue missed and its full-year EPS guidance fell short of Wall Street’s estimates. Overall, this quarter was mixed, and it seems the market is focusing on the positives for now. The stock traded up 2.3% to $40.28 immediately after reporting.

Is LKQ an attractive investment opportunity at the current price? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.