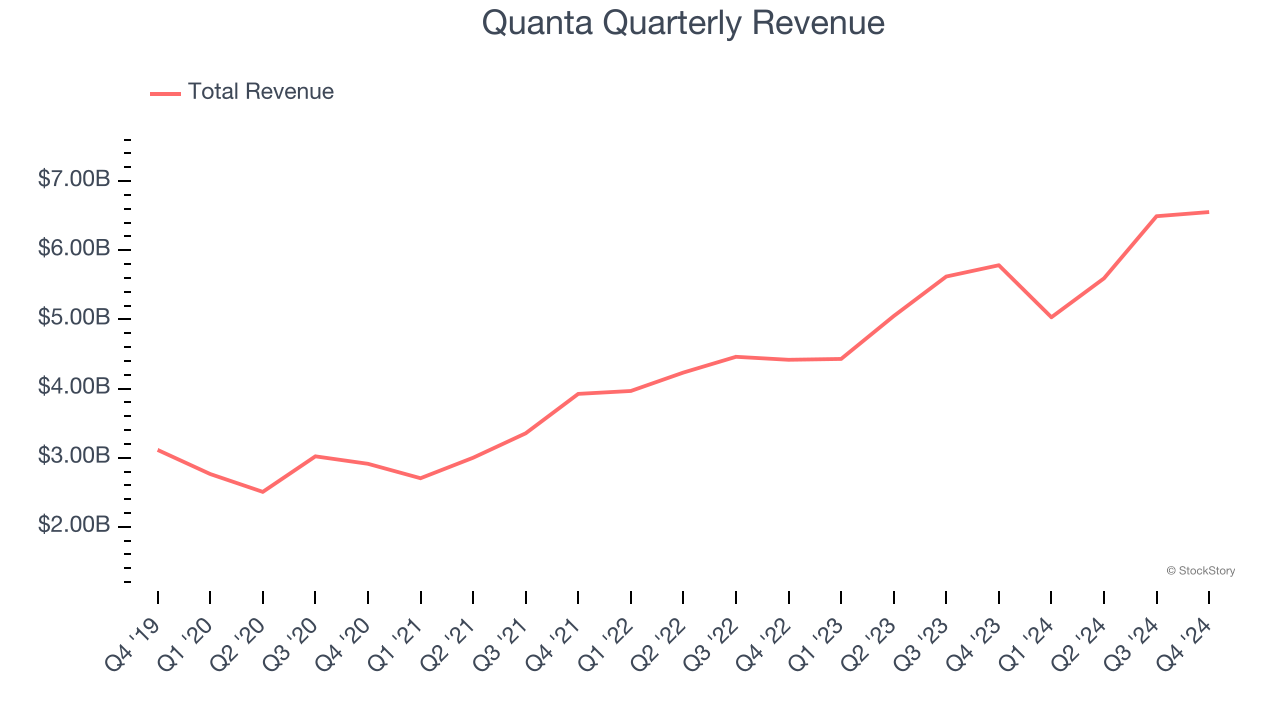

Infrastructure solutions provider Quanta (NYSE: PWR) fell short of the market’s revenue expectations in Q4 CY2024, but sales rose 13.3% year on year to $6.55 billion. Its non-GAAP profit of $2.94 per share was 12.1% above analysts’ consensus estimates.

Is now the time to buy Quanta? Find out by accessing our full research report, it’s free.

Quanta (PWR) Q4 CY2024 Highlights:

- Revenue: $6.55 billion vs analyst estimates of $6.62 billion (13.3% year-on-year growth, 1% miss)

- Adjusted EPS: $2.94 vs analyst estimates of $2.62 (12.1% beat)

- Adjusted EBITDA: $737.8 million vs analyst estimates of $685.1 million (11.3% margin, 7.7% beat)

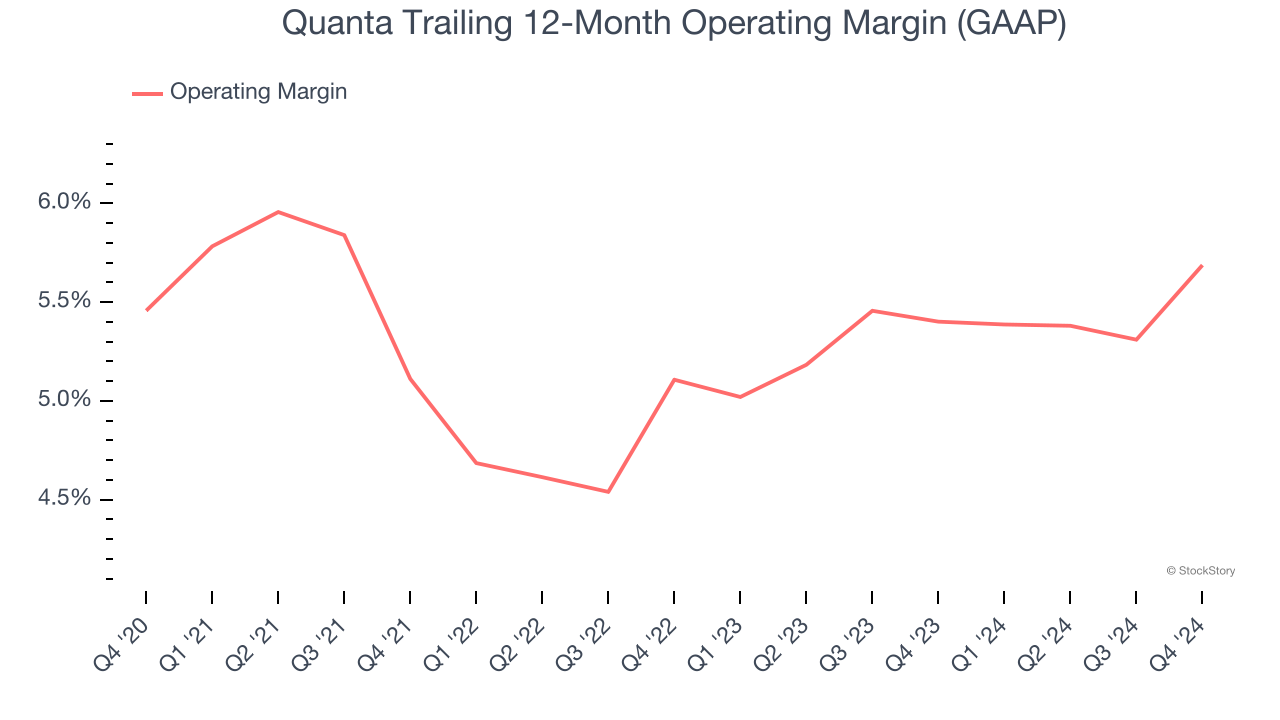

- Operating Margin: 6.9%, up from 5.6% in the same quarter last year

- Free Cash Flow Margin: 8.6%, down from 15.8% in the same quarter last year

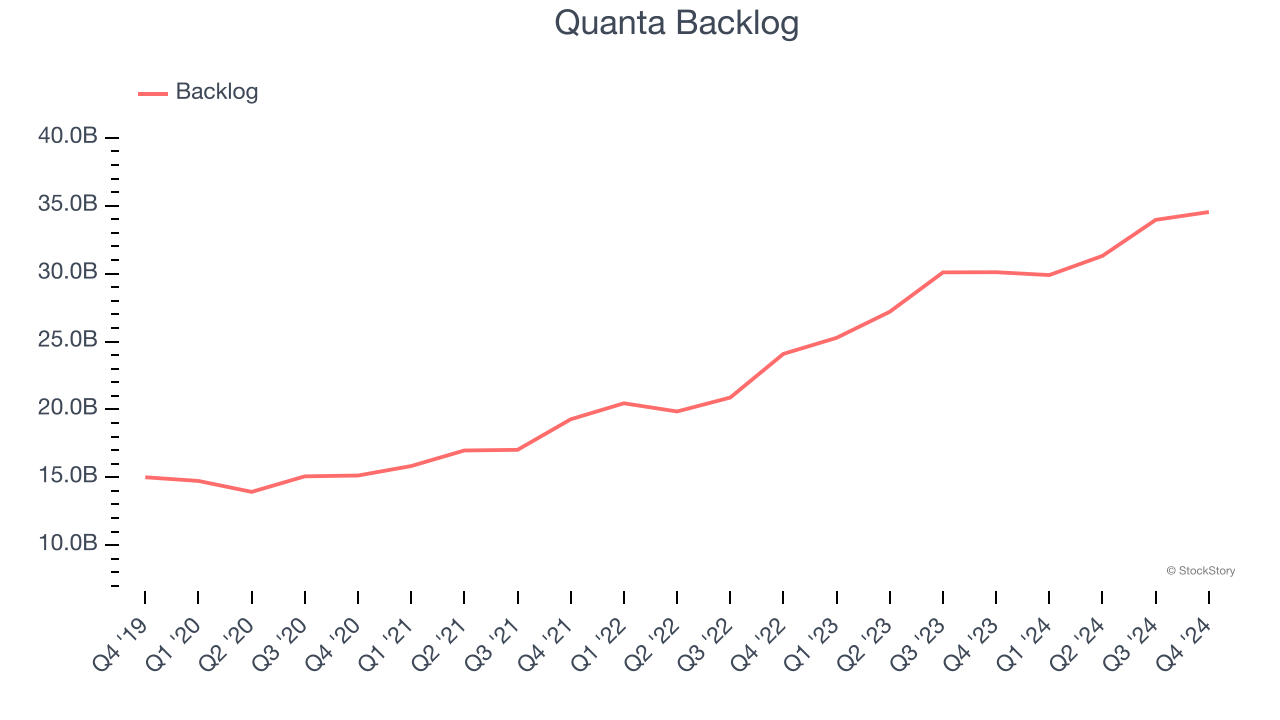

- Backlog: $34.54 billion at quarter end, up 14.7% year on year

- Market Capitalization: $43.11 billion

"Quanta's fourth-quarter results reflect the strength of our business, delivering double-digit growth across key financial metrics, $575 million in free cash flow and record backlog. This caps another year of success, with record revenues, profits and cash flow, while maintaining a rock-solid balance sheet that positions us for continued strategic growth. I want to recognize the unwavering dedication of our Quanta family, whose expertise and commitment to excellence continues to drive our success," said Duke Austin, President and Chief Executive Officer of Quanta Services.

Company Overview

A construction engineering services company, Quanta (NYSE: PWR) provides infrastructure solutions to a variety of sectors, including energy and communications.

Energy Products and Services

Areas like the energy transition and emission reduction are thematic and front of mind today. This can be a double-edged sword for the energy products and services industry. Those who innovate and build new expertise can jolt demand while those who cling to legacy technologies or fall behind in the trending areas could see their market shares diminish. Bigger picture, energy products and services companies are still at the whim of construction and infrastructure project volumes, which tend to be cyclical and can be impacted heavily by economic factors such as interest rates.

Sales Growth

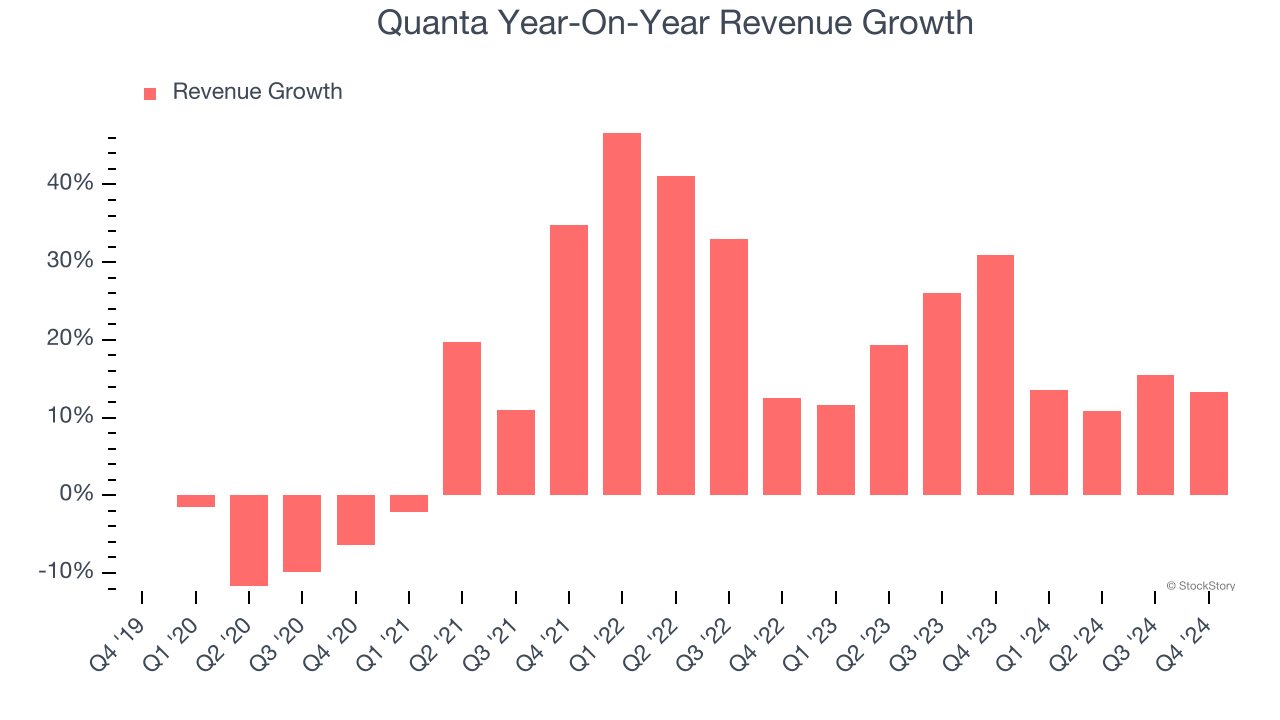

A company’s long-term sales performance signals its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Thankfully, Quanta’s 14.3% annualized revenue growth over the last five years was exceptional. Its growth beat the average industrials company and shows its offerings resonate with customers, a helpful starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Quanta’s annualized revenue growth of 17.7% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

We can better understand the company’s revenue dynamics by analyzing its backlog, or the value of its outstanding orders that have not yet been executed or delivered. Quanta’s backlog reached $34.54 billion in the latest quarter and averaged 23.8% year-on-year growth over the last two years. Because this number is better than its revenue growth, we can see the company accumulated more orders than it could fulfill and deferred revenue to the future. This could imply elevated demand for Quanta’s products and services but raises concerns about capacity constraints.

This quarter, Quanta’s revenue grew by 13.3% year on year to $6.55 billion but fell short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 13.2% over the next 12 months, a deceleration versus the last two years. We still think its growth trajectory is attractive given its scale and suggests the market is factoring in success for its products and services.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Operating Margin

Quanta was profitable over the last five years but held back by its large cost base. Its average operating margin of 5.4% was weak for an industrials business. This result isn’t too surprising given its low gross margin as a starting point.

Looking at the trend in its profitability, Quanta’s operating margin might have seen some fluctuations but has generally stayed the same over the last five years, meaning it will take a fundamental shift in the business to change.

This quarter, Quanta generated an operating profit margin of 6.9%, up 1.3 percentage points year on year. Since its gross margin expanded more than its operating margin, we can infer that leverage on its cost of sales was the primary driver behind the recently higher efficiency.

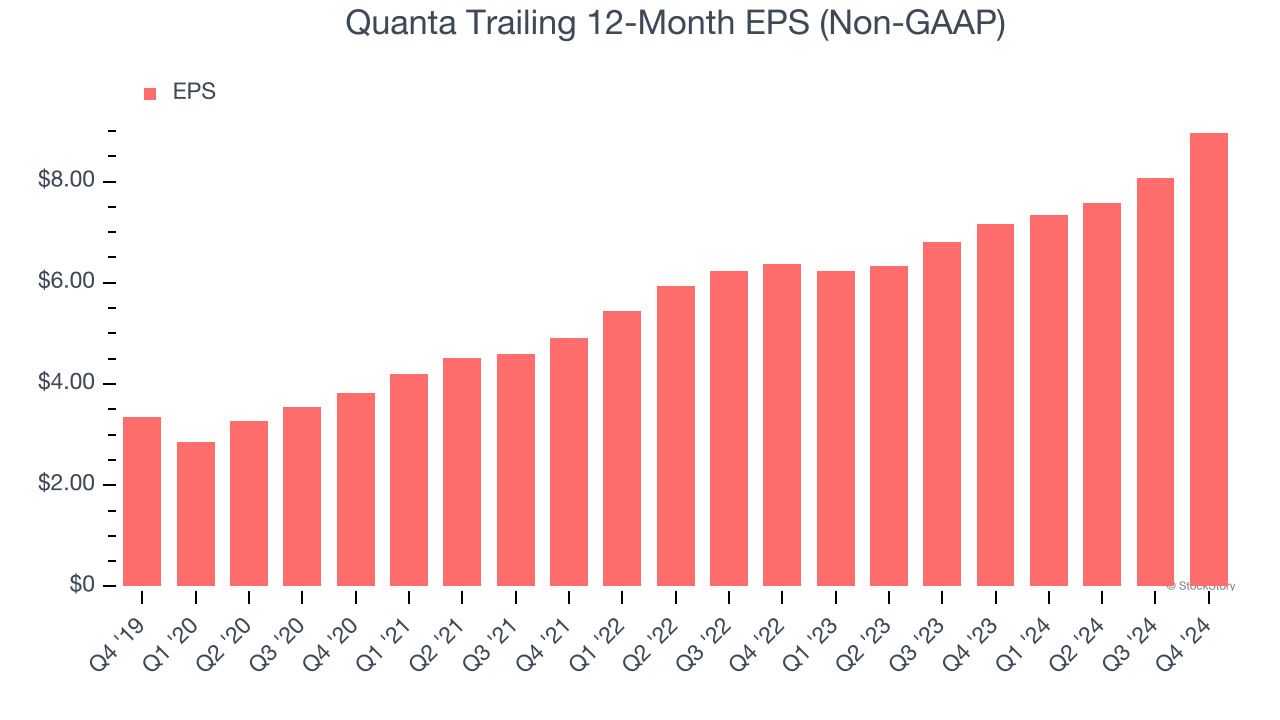

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Quanta’s EPS grew at an astounding 21.8% compounded annual growth rate over the last five years, higher than its 14.3% annualized revenue growth. However, we take this with a grain of salt because its operating margin didn’t expand and it didn’t repurchase its shares, meaning the delta came from reduced interest expenses or taxes.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Quanta, its two-year annual EPS growth of 18.7% was lower than its five-year trend. We still think its growth was good and hope it can accelerate in the future.

In Q4, Quanta reported EPS at $2.94, up from $2.04 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Quanta’s full-year EPS of $8.97 to grow 15.4%.

Key Takeaways from Quanta’s Q4 Results

We were impressed by how significantly Quanta blew past analysts’ EBITDA expectations this quarter. We were also glad its backlog outperformed Wall Street’s estimates. On the other hand, its revenue slightly missed. Zooming out, we think this was a solid quarter. The stock traded up 8.6% to $316.90 immediately following the results.

Quanta had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.