Texas Roadhouse has followed the market’s trajectory closely. The stock is down 10.6% to $162.91 per share over the past six months while the S&P 500 has lost 8.9%. This might have investors contemplating their next move.

Given the weaker price action, is now a good time to buy TXRH? Find out in our full research report, it’s free.

Why Is Texas Roadhouse a Good Business?

With locations often featuring Western-inspired decor, Texas Roadhouse (NASDAQ: TXRH) is an American restaurant chain specializing in Southern-style cuisine and steaks.

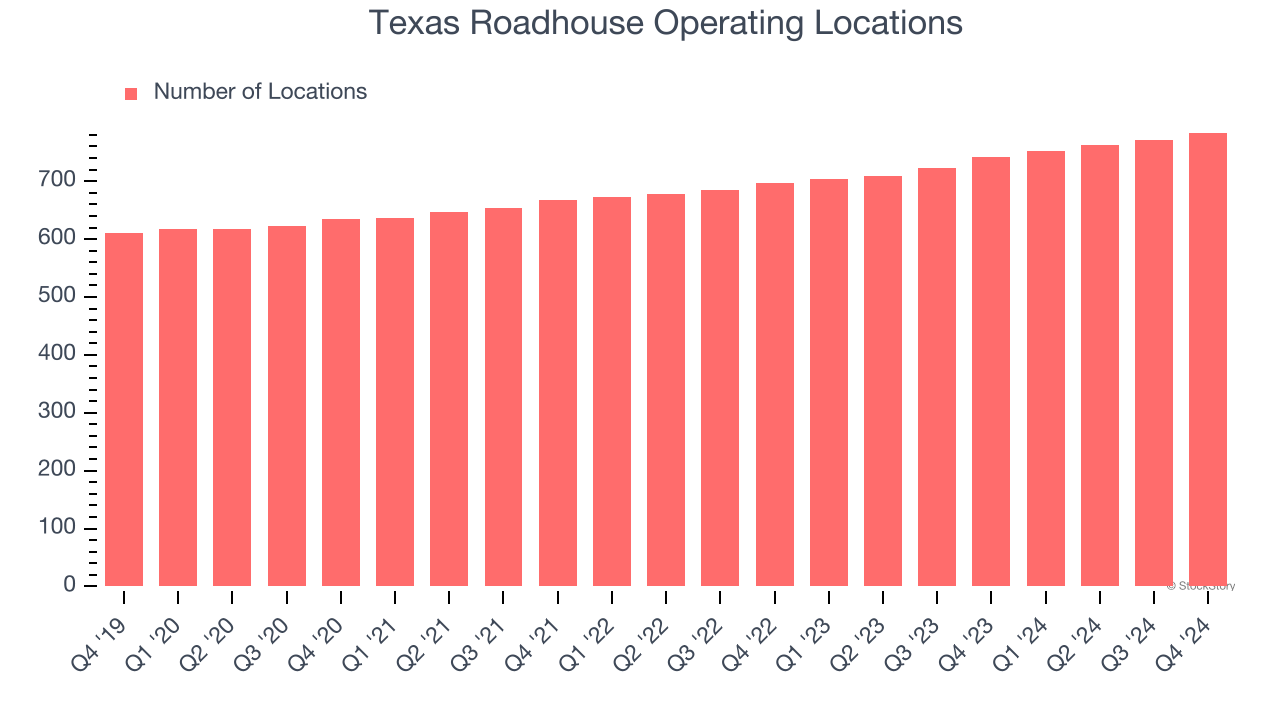

1. Restaurant Growth Signals an Offensive Strategy

The number of dining locations a restaurant chain operates is a critical driver of how quickly company-level sales can grow.

Texas Roadhouse operated 784 locations in the latest quarter. It has opened new restaurants at a rapid clip over the last two years, averaging 6% annual growth, much faster than the broader restaurant sector.

When a chain opens new restaurants, it usually means it’s investing for growth because there’s healthy demand for its meals and there are markets where its concepts have few or no locations.

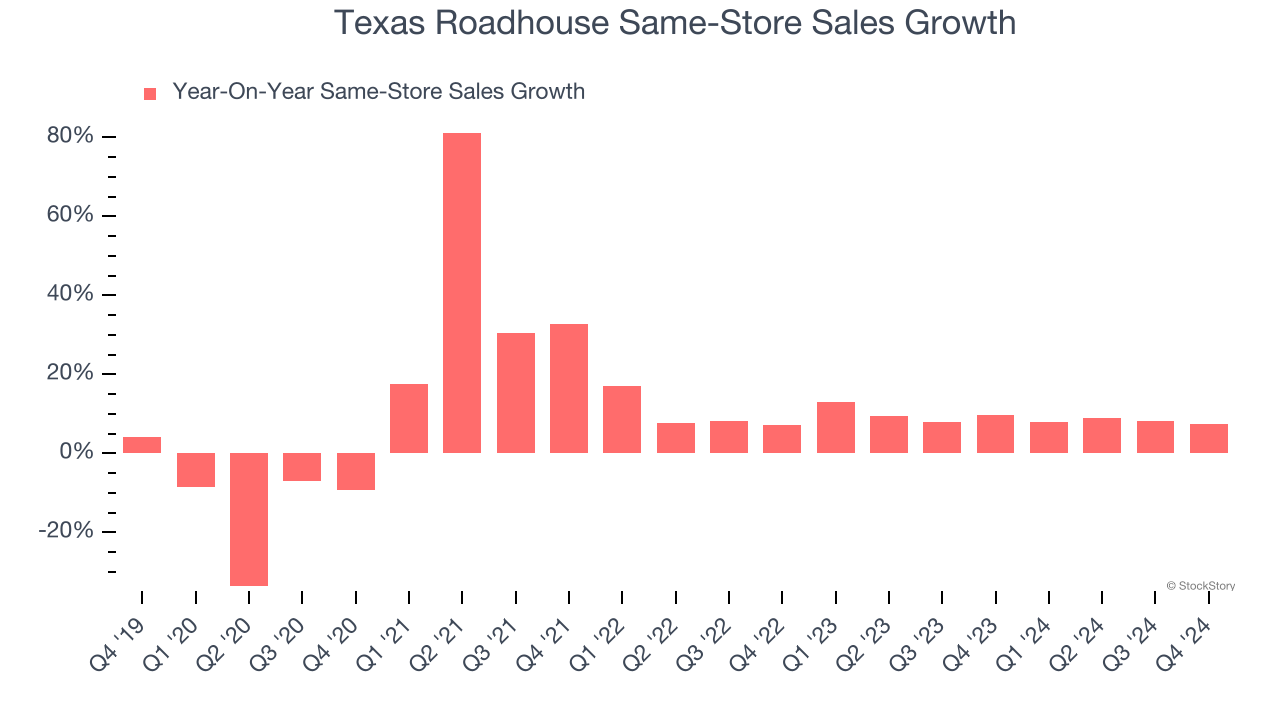

2. Surging Same-Store Sales Show Increasing Demand

Same-store sales is a key performance indicator used to measure organic growth at restaurants open for at least a year.

Texas Roadhouse has been one of the most successful restaurant chains over the last two years thanks to skyrocketing demand within its existing dining locations. On average, the company has posted exceptional year-on-year same-store sales growth of 9.1%.

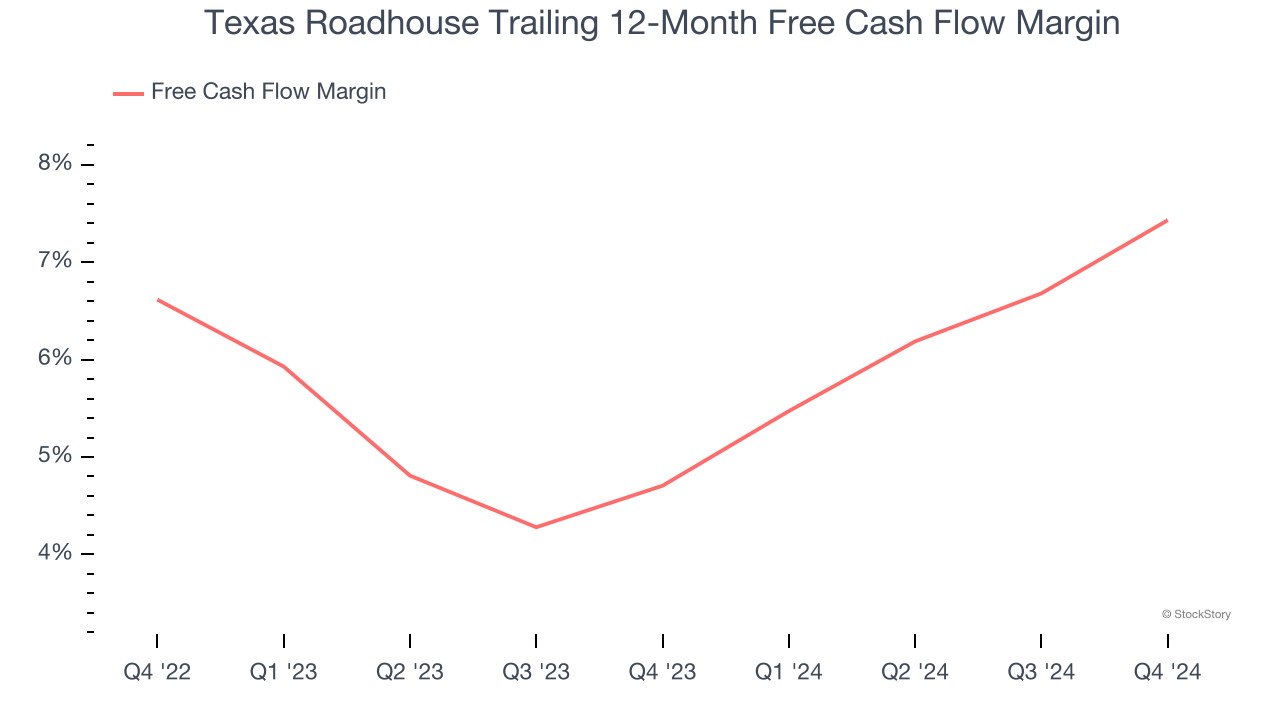

3. Increasing Free Cash Flow Margin Juices Financials

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Texas Roadhouse’s margin expanded by 2.7 percentage points over the last year. This is encouraging because it gives the company more optionality. Texas Roadhouse’s free cash flow margin for the trailing 12 months was 7.4%.

Final Judgment

These are just a few reasons why we think Texas Roadhouse is a great business. With the recent decline, the stock trades at 22.3× forward price-to-earnings (or $162.91 per share). Is now the right time to buy? See for yourself in our in-depth research report, it’s free.

Stocks We Like Even More Than Texas Roadhouse

Donald Trump’s victory in the 2024 U.S. Presidential Election sent major indices to all-time highs, but stocks have retraced as investors debate the health of the economy and the potential impact of tariffs.

While this leaves much uncertainty around 2025, a few companies are poised for long-term gains regardless of the political or macroeconomic climate, like our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today for free.