As the Q3 earnings season comes to a close, it’s time to take stock of this quarter’s best and worst performers in the gas and liquid handling industry, including Atmus Filtration Technologies (NYSE: ATMU) and its peers.

Gas and liquid handling companies possess the technical know-how and specialized equipment to handle valuable (and sometimes dangerous) substances. Lately, water conservation and carbon capture–which requires hydrogen and other gasses as well as specialized infrastructure–have been trending up, creating new demand for products such as filters, pumps, and valves. On the other hand, gas and liquid handling companies are at the whim of economic cycles. Consumer spending and interest rates, for example, can greatly impact the industrial production that drives demand for these companies’ offerings.

The 13 gas and liquid handling stocks we track reported a strong Q3. As a group, revenues beat analysts’ consensus estimates by 0.8% while next quarter’s revenue guidance was 0.7% below.

Luckily, gas and liquid handling stocks have performed well with share prices up 14.8% on average since the latest earnings results.

Best Q3: Atmus Filtration Technologies (NYSE: ATMU)

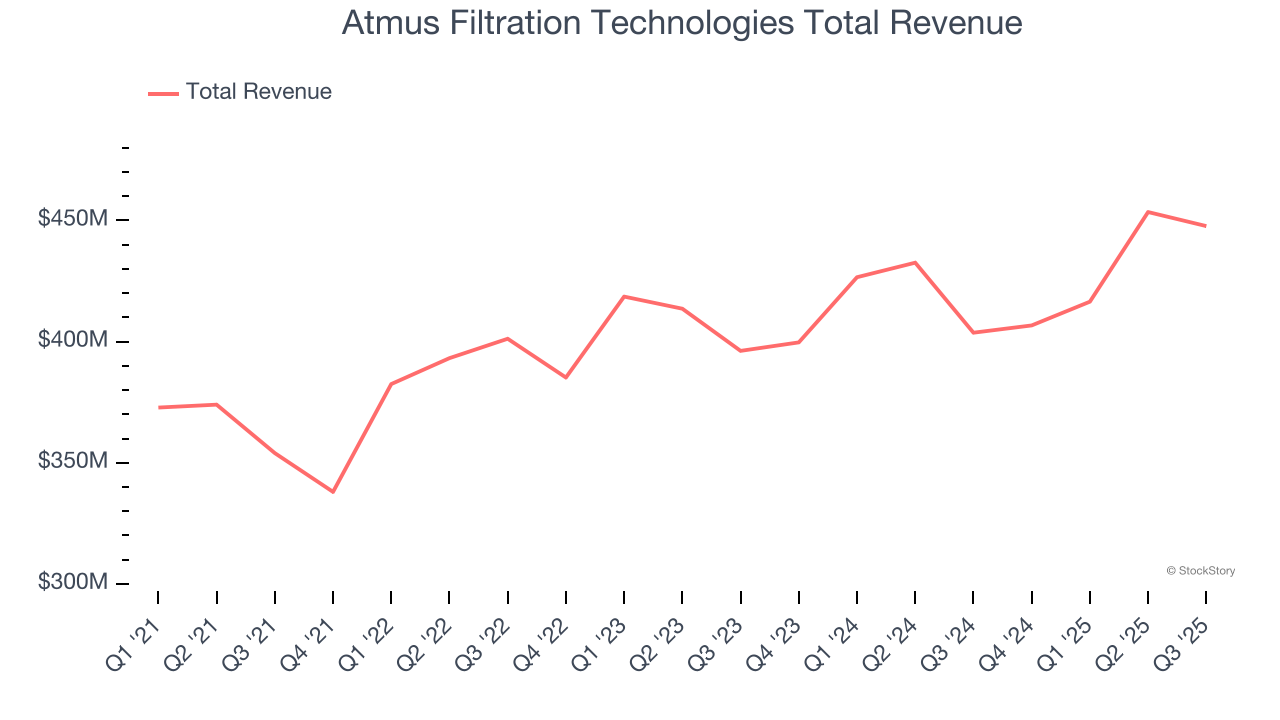

Spun out of Cummins in 2023 after 65 years as part of the engine maker, Atmus Filtration Technologies (NYSE: ATMU) manufactures filters for trucks, construction equipment, and agriculture machinery to reduce emissions and protect engines.

Atmus Filtration Technologies reported revenues of $447.7 million, up 10.9% year on year. This print exceeded analysts’ expectations by 7.5%. Overall, it was a stunning quarter for the company with an impressive beat of analysts’ EBITDA estimates and a solid beat of analysts’ adjusted operating income estimates.

Atmus Filtration Technologies scored the biggest analyst estimates beat of the whole group. Unsurprisingly, the stock is up 23.9% since reporting and currently trades at $57.62.

Is now the time to buy Atmus Filtration Technologies? Access our full analysis of the earnings results here, it’s free.

SPX Technologies (NYSE: SPXC)

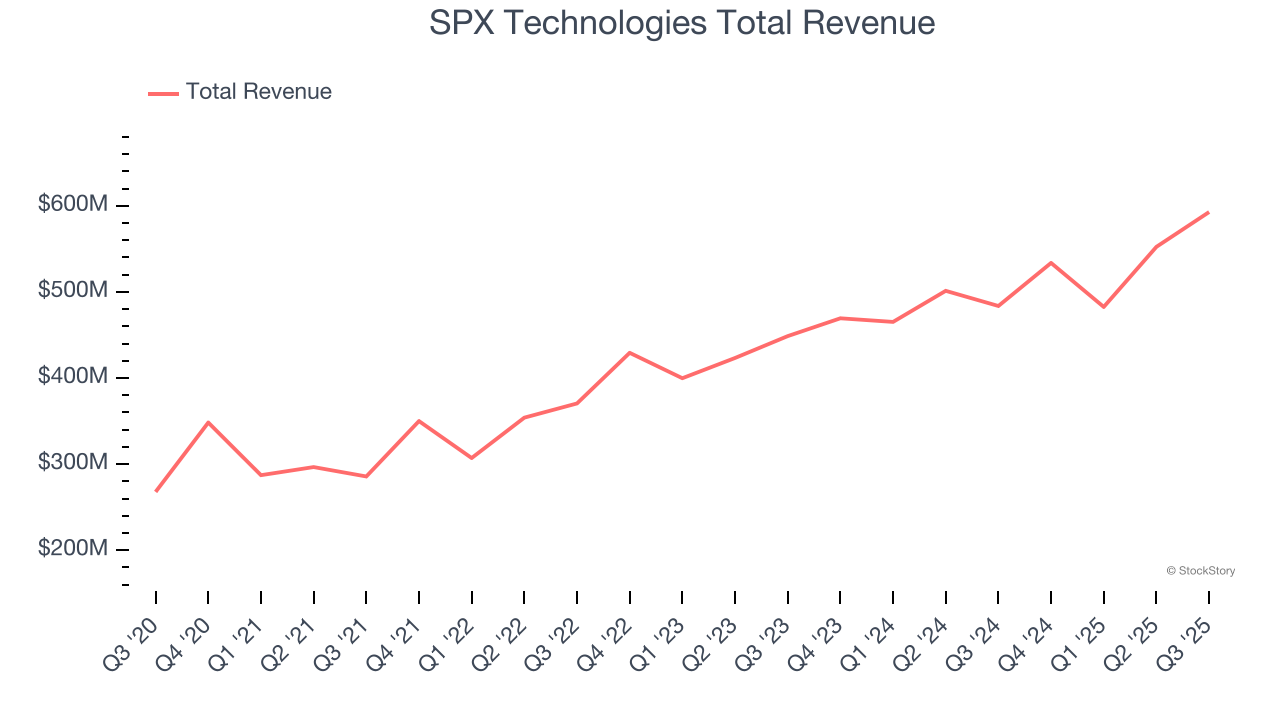

With roots dating back to 1912 as the Piston Ring Company, SPX Technologies (NYSE: SPXC) supplies specialized infrastructure equipment for HVAC systems and detection and measurement applications across industrial, commercial, and utility markets.

SPX Technologies reported revenues of $592.8 million, up 22.6% year on year, outperforming analysts’ expectations by 2.2%. The business had an exceptional quarter with an impressive beat of analysts’ EBITDA estimates and a solid beat of analysts’ adjusted operating income estimates.

The market seems happy with the results as the stock is up 8.9% since reporting. It currently trades at $216.33.

Is now the time to buy SPX Technologies? Access our full analysis of the earnings results here, it’s free.

Weakest Q3: Graco (NYSE: GGG)

Founded in 1926, Graco (NYSE: GGG) is an industrial company specializing in the development and manufacturing of fluid-handling systems and products.

Graco reported revenues of $543.4 million, up 4.7% year on year, falling short of analysts’ expectations by 3%. It was a softer quarter as it posted a significant miss of analysts’ revenue estimates and a miss of analysts’ EBITDA estimates.

Interestingly, the stock is up 7.3% since the results and currently trades at $87.53.

Read our full analysis of Graco’s results here.

Gorman-Rupp (NYSE: GRC)

Powering fluid dynamics since 1934, Gorman-Rupp (NYSE: GRC) has evolved from its Ohio origins into a global manufacturer and seller of pumps and pump systems.

Gorman-Rupp reported revenues of $172.8 million, up 2.8% year on year. This number lagged analysts' expectations by 1%. It was a slower quarter as it also produced a significant miss of analysts’ EPS estimates and a slight miss of analysts’ revenue estimates.

Gorman-Rupp had the slowest revenue growth among its peers. The stock is up 9.7% since reporting and currently trades at $53.85.

Read our full, actionable report on Gorman-Rupp here, it’s free.

IDEX (NYSE: IEX)

Founded in 1988, IDEX (NYSE: IEX) is a global manufacturer specializing in highly engineered products such as pumps, flow meters, and fluidics systems for various industries.

IDEX reported revenues of $878.7 million, up 10.1% year on year. This print topped analysts’ expectations by 2%. Overall, it was a very strong quarter as it also logged a solid beat of analysts’ adjusted operating income estimates and a solid beat of analysts’ organic revenue estimates.

The stock is up 18.5% since reporting and currently trades at $197.82.

Read our full, actionable report on IDEX here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Quality Compounder Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.